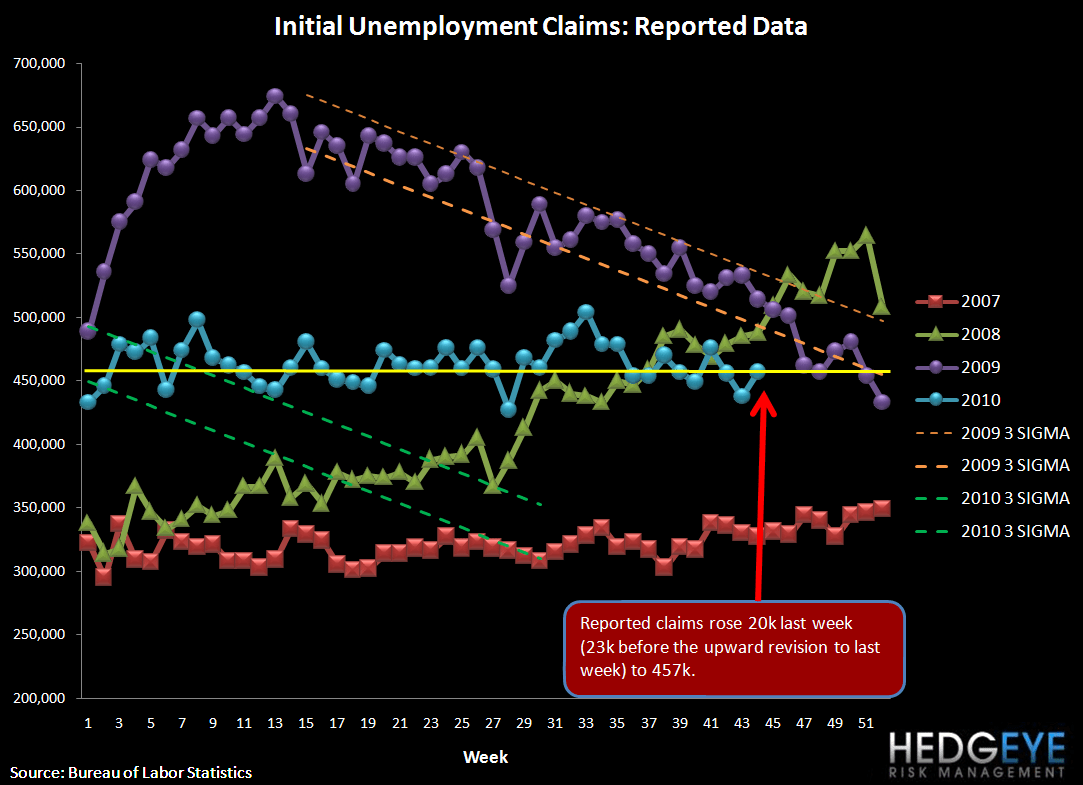

Initial Claims Rise 23k, Offsetting Last Week's 21k Improvement

The headline initial claims number rose 20k last week to 457k (23k net of revisions). Rolling claims came in at 456k, an increase of 2k over the previous week. This wiped out last week’s improvement, and claims still remain in the same band they’ve occupied for the year. We're still a solid 50-75k above where we would need to be in order to see unemployment fall.

QE2 Not Showing Any Signs of Taking Down Claims So Far

Interestingly, in the last round of Quantitative Easing (QE1), we saw almost all of the decline in mortgage rates occur between the time when the program was announced in late 2008 and when the buying commenced in early 2009. We think this time is similar in that mortgage rates have already come in substantially, to all time lows. What's interesting to observe is that mortgage rates have been exceedingly low now for a few months, but we've seen no real improvement in jobless claims. Maybe this is too short a window against which to measure success, but it is interesting to note that so far there appears to have been no transmission of QE2 into lower claims. We would not expect to see long rates drop much further from here, consistent with QE1.

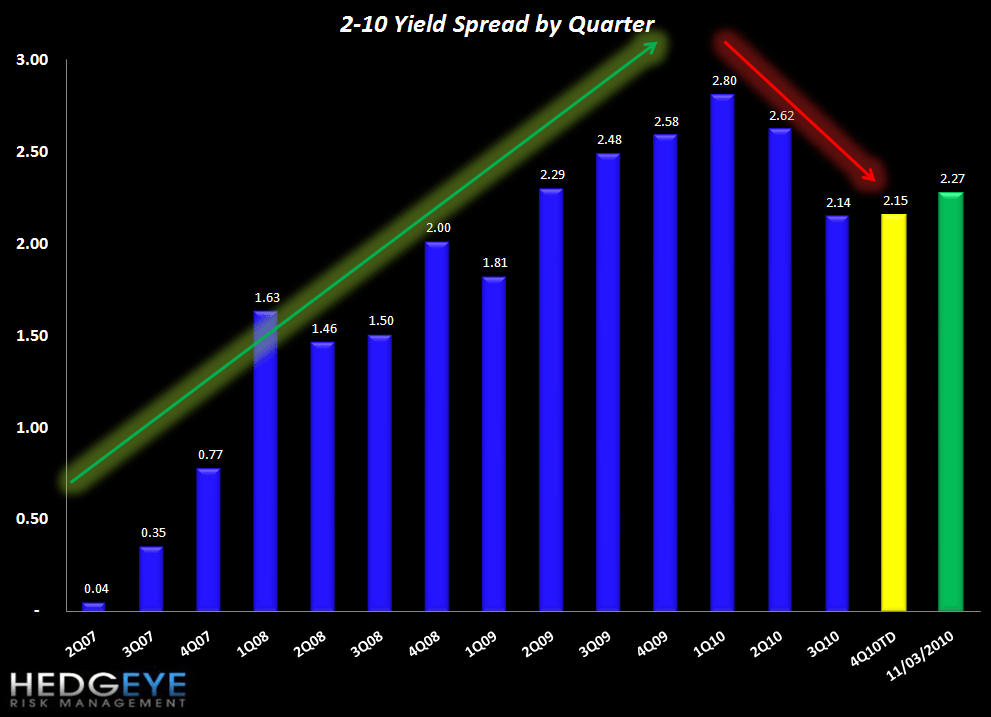

Yield Curve

The following chart shows 2-10 spread by quarter while the chart below that shows the sequential change. The 2-10 spread (a proxy for NIM) has recently stabilized with the backup in the 10-year treasury. Yesterday’s closing value of 224 bps is down from 231 bps last week.

The table below shows the stock performance of each Financial subsector over four durations.

Our Macro Team's Howard Penney and Rory Green published the following chart yesterday showing that the AAII Bulls-Bears survey has not been more bullish since February of 2007, suggesting downside risk has grown considerably. For reference, peak bearishness occurred on March 5th, 2009, a day before the market bottom.

Joshua Steiner, CFA

Allison Kaptur