Solid week for both footwear and apparel sales. Nike continues to crush it while regional performance out West is starting to outperform. In looking forward to November, comps are extremely favorable across the athletic industry. It’s important to note, however, that at the same time apparel comps get increasingly more favorable over the next 4-weeks, footwear comps are getting less so on the margin. Below are this week’s key callouts:

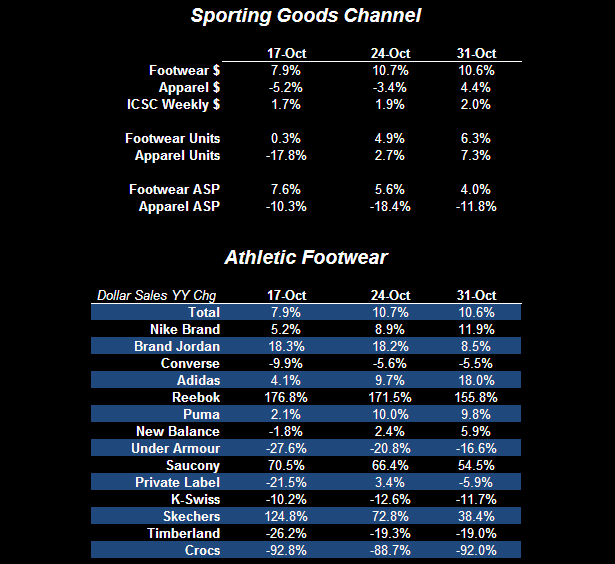

Sports Apparel:

- After facing the toughest comps of the next 12-months, driven by UA’s launch of fitted product and an unseasonably cold October (-2%-3% below average), Sports Apparel sales now faces its most favorable through the first week of December.

- Sport Retailers continue to outperform both Family Retailers and Mass/Discount channels with underlying trends up mid-to-high single digits – good for DKS, HIBB, FL, FINL, etc.

- As we look towards November, temps were 3%-4% higher than average throughout the month last year. Based on our limited sample here in New England, we can attest to a rapid turn in temps with the season’s first frost coming on the 1st of the month.

- We may be starting to see a modest pickup in discounting in the Athletic Specialty channel – though still early make a bigger callout. The ~1% decline in ASP is consistent with pricing throughout October, however, the increase in weekly unit sales suggests promotional activity may be underway particularly with prices firming in other channels.

- Sales improved across all regions with relative outperformance in the Pacific region over the last 2-weeks a key callout. This comes on the heels of positive commentary out of BGFV on traffic and comp trends throughout Q3 and in the first weeks of Q4.

Athletic Footwear:

- With comps starting to get progressively less favorable, new product will be the key to sustaining positive momentum.

- Over the last two weeks, Nike (Air Max LeBron 8), Under Armour (Micro G Inception) and Adidas (TS Beast & adiZero) have blitzed the market with key launches. Given that basketball accounts for ~25% of the athletic footwear sales, we expect sales to reflect the acceleration of new product into the channel.

- Not only is Nike continuing to post robust sales at both Nike Brand and Brand Jordan, but Converse is also starting to improve on the margin over the past month as well.

Casey Flavin

Director