Conclusion: We are short CMG in the Hedgeye Virtual Portfolio.

CMG is now the sixth largest publically traded restaurant company having just come public in 2006. It has the captivation of the growth crowd, as there are few other alternatives in which to invest as part of a growth-oriented strategy. For the past three quarters, the company has crushed it, beyond my expectations. I don’t like to “chase” stocks so I have missed the doubling in the stock this year.

With just two short months left in the calendar year, if you own CMG you probably want to hang on for the balance of the year in order to show everybody how you have done and so as to not incur the significant tax liability that comes with selling it.

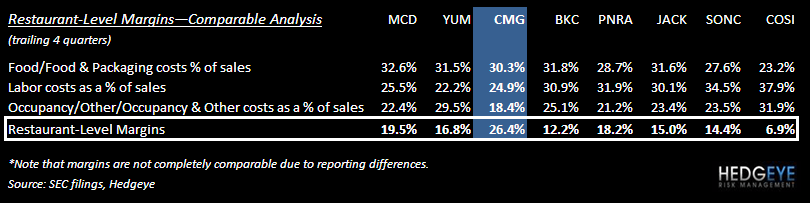

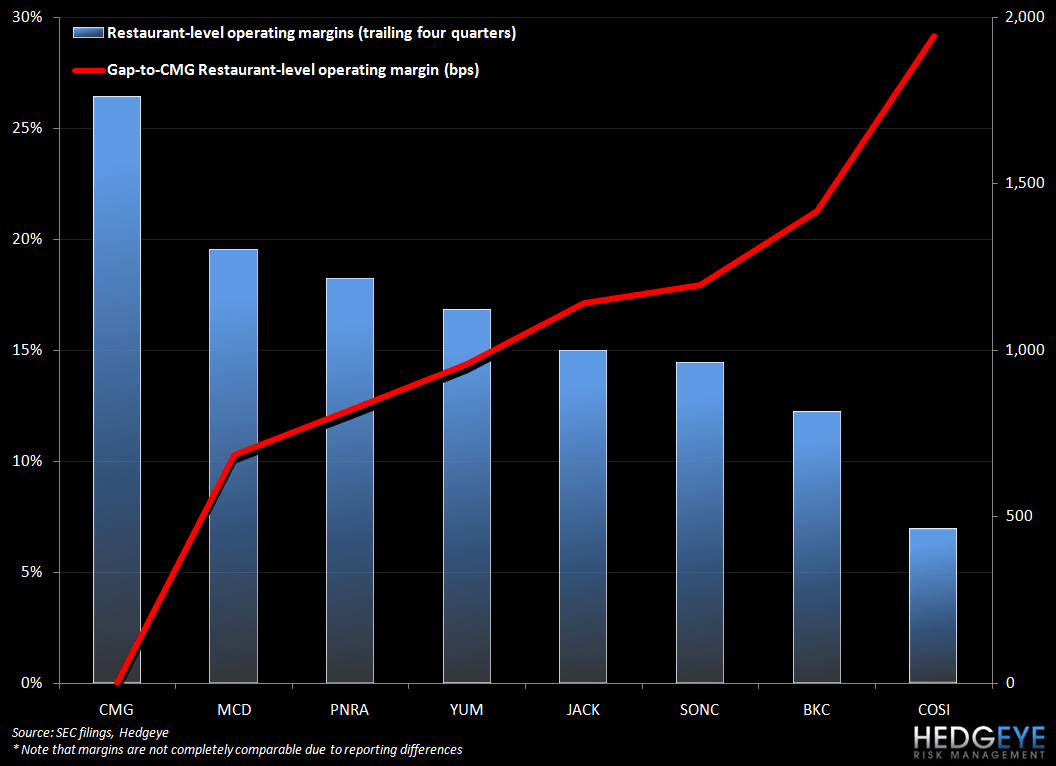

Certainly the financial performance has been nothing short of amazing in FY10 with restaurant-level margins that are about 1200 bps above comparable companies on average (please refer to the charts below for more details). The company’s new A-model sites are pushing the envelope on growth, allowing growth investors to become even more captivated by the company’s potential. Ah yes, and there is the potential to take over the world…I get it - comps, margins and the unit growth potential are mesmerizing.

We all know nothing happens in a straight line, but CMG’s current market capitalization values each store at nearly $7 million.

How can we forget Howard Schultz telling the investment community that SBUX was going to have 40,000 stores when that stock was trading at $40 and 40x EPS? Or the potential for PFCB’s Bistro when the stock was at $65 and trading at 40x EPS. We can’t forget CAKE and its smaller unit, which was going to accelerate the potential number of units (not to mention the potential for Grand Lux) when that stock was at $39 and 35x EPS. As the following chart shows, however, the multiples of SBUX, CAKE and PFCB have all come down over time.

Yes, history is repeating itself and the “food with integrity” mantra produced an unprecedented 27.7% restaurant-level margin last quarter.

So what is the market discounting? Perhaps, perfection for the next five years. In 2016, based on my preliminary estimates, I have the company operating 1,916 stores and generating about $615 million in EBITDA or a 17% EBITDA margin; down slightly from my 19.4% EBITDA margin estimate for 2010.

While the growth in stores and EBITDA could possibly be some of the best in the industry, what you can’t fight is the ultimate multiple assigned to a more mature business in 2016. If we assume the stock trades at 10x our 2016 EBITDA estimate (which is a strong multiple given the potential issues outlined below), we get a market capitalization that is down about 7.5% from where we are today.

All of this assumes the company can maintain the same “integrity” across a nearly 2000-unit store base as it has with a 1000-unit store base. Below is a list of issues that the company will likely face over the next 5 years:

(1) Increased competition

(2) Increased labor

(3) Increased food costs

(4) A challenging consumer environment

(5) An aging store base

(6) A compromised site selection strategy

(7) Slowing same-store sales

(8) Declining margins

Lastly, the biggest issue CMG will likely face relates to the company’s announcement after the close today that it is working on an Asian restaurant concept that will follow the Chipotle model. The company plans to open one Asian inspired restaurant in 2011. Unfortunately, I have seen this movie before and it does not typically end well as the company will begin to throw shareholder capital at a concept that will earn less of a return than CMG’s current business model.

Howard Penney

Managing Director