This note was originally published at 8am this morning, November 03, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

"We must all strive to find common ground to support the middle class, create jobs, reduce the deficit and move our nation forward."

-Nancy Pelosi, November 2nd, 2010

While it will take many days for the final tallies to come in, it looks like our prediction will hold and that massive Republican turnout has driven a net gain in House seats of 65+ for Republicans. According to Nate Silver over at the FiveThirtyEight blog (one of the more accurate electoral statisticians we follow):

“Our current projection is that Republicans will finish with a total of 243 house seats: this would reflect a net gain of 65 from Democrats. The range of plausible outcomes is fairly small: our model thinks there is roughly a 90 percent chance that the G.O.P.’s total will eventually be somewhere between 64 seats and 66.”

As it relates to our prediction in the Senate, we were off slightly as a number of major Democratic candidates did marginally better than expected, in particular Harry Reid in Nevada. Currently, Alaska, Colorado, and Washington are still too close to call, but even if these States all go Republican the Democrats will still retain at least 51 seats in the Senate. Nonetheless, the Democrats should lose a net 7 seats.

Since it seemed statistically unlikely that the Republicans could take the Senate, the story of the night is really the massive seat losses in the House. To put it in historical context, this will likely be the largest seat loss in a midterm election for any party since 1938 under President Roosevelt, when the Democrats lost 72 House seats and 7 seats in the Senate. Clearly, the electoral results today are indicative of a strong statement being made by the American people.

The obvious conclusion from these results is that this is a repudiation of the Obama agenda. While we would be naïve to not agree at least partially with that, more broadly this looks to be a referendum on politicians themselves. To wit, given a historical incumbency advantage of almost 90%, the last three congressional elections of 2006, 2008 and 2010 have shown accelerated volatility of incumbent losses. Specifically, in 2006 the Democrats gained 30 seats in the House, in 2008 the Democrats gained 22 seats, and in 2010 the Republicans will likely gain back 65 seats. In a span of four years, we have seen massive volatility between the parties and the relative support from the electorate.

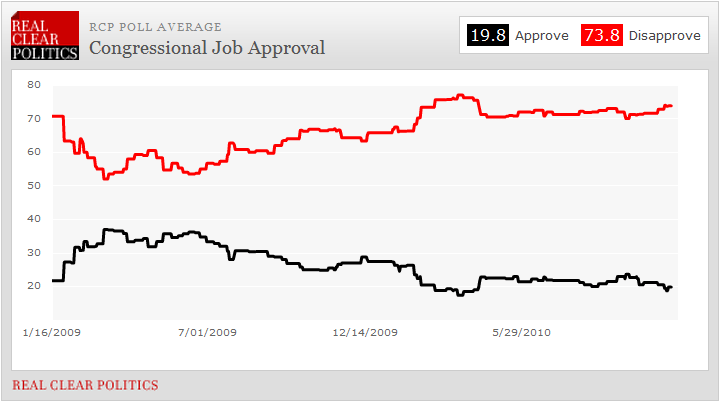

The chart of the day, which is posted below, underscores the key reason why this occurring. This chart highlights broad congressional approval. Currently, 73.8% of voters disapprove of Congress! If you were a professional politician yesterday and didn’t understand the implications of that yesterday, today you do in spades.

We’ve used a quote from Nancy Pelosi at the top of the note today to further emphasize our point regarding the popularity of professional politicians. While Pelosi retained her seat, her approval rating across the country as Speaker of the House was 29% heading into yesterday’s election. Her brief statement last night, assuming it is not just rhetoric, is actually what politicians collectively need to work towards for this nation. More broadly, the message this morning is clear from Americans, they are tired of rhetoric.

While the Republicans will take a few victory laps over the next few days, the gauntlet is now thrown to them. They have been given at least a nominal agenda and the next two years will be a test as to whether they can work with the President to move the country forward. The questions we would ask are: what is next for monetary policy, what can be done about the burgeoning budget deficit, and how can we address the escalating sovereign debt situation of the federal government? As Paul Rand stated in his victory speech last night:

“When I arrive in Washington, I will ask them, respectfully, to deliberate upon this. We are in the midst of a debt crisis and the people want to know why we have to balance our budget - and they don't.”

To take a deeper dive on some of these questions and to test the mettle of the rhetoric we will be hearing over the coming weeks, Keith and I will be hosting a call next Wednesday November 10th at 1PM with Peter Orszag, former Director of the Office of the Management and Budget. This call will be a similar format to the one we held with our friend Karl Rove in September. Peter will present for 20 – 25 minutes and he will then take questions for the duration of the call.

If there is anyone in the nation who understands what can and cannot be done to reduce the budget deficit, it is Peter Orszag. If you would like to join this call and are an institutional subscriber, or would like to trial our institutional service for the call, please email Jen Kane at sales@hedgeye.com. The budget deficit is one of the most pressing economic issues facing the United States; therefore we think this call will be a valuable use of your time.

To Rand’s point in his victory speech last night, the people of America are asking a lot of questions. The next two years will be a test as to whether the professional politicians are finally ready to answer the people with more than rhetoric. Needless to say, our Hedgeyes will be watching.

Yours in risk management,

Daryl G. Jones

Managing Director