The guest commentary below was written by written by Michael Aroesty of DBR & CO. This piece does not necessarily reflect the opinions of Hedgeye.

|

“Failure is not fatal, but failure to change might be.” - John Wooden The only thing worse than being surprised by the unexpected, is for the expected to occur and not having been prepared. During his 27-year reign as the head coach of the UCLA Men’s Basketball team, “The Wizard of Westwood” prepared for nearly everything. More importantly, his ability to evolve in-game strategy to meet the challenges of his opponents, netted him 10 NCAA National Championships in his last 12 seasons. Legend! |

From a rate of change perspective, we are in the midst of one of the most “legendary” accelerations in both growth and inflation of our lifetimes.

Only a year ago, we saw economic growth in the US get pancaked to -9% year-over-year (y/y). While the 2Q2021 data will not be reported until July, our current estimates suggest that US GDP growth will accelerate by nearly 13%. Furthermore, as we look out over the balance of 2021, we expect GDP to remain elevated, at or above 7%. Given consumers fervent demand and bottomed-out 2020 year-over-year comparisons, these absolute levels of growth are unsurprising.

Equity markets responded accordingly to GDP’s epic ramp. In the second quarter alone, we enjoyed 15 separate all-time closing highs in the S&P 500. All-time, as they say, is a long time.

Interestingly though, despite the rapid rebound in economic activity, growth is not investors’ primary focus. Inflation, which has been benign for much of the past decade, has become THE economic story of the year as it continues to outpace estimates and surprise to the upside.

As an example of inflation’s rebound, recall at this time last year, with global travel banned and cars sitting idly in our garages, oil prices actually went negative(!) for the first time in history (for those around in the late 1970s and early 1980s, let that sink in..).

A year later, oil prices exceed $70/barrel for the first time since 2018. Additionally, from the economy’s abrupt March 2020 closure to perhaps even more abrupt June 2021 boom, residential construction input prices have risen 23%, used cars have inflated by nearly 30%, airfares by 24% and auto rentals by over 100% over the past year.

For the time being, the Federal Reserve is holding to their story that these price surges will be “transitory” (i.e., a short-term phenomenon that will be corrected by normal market forces).

We would agree with the Fed that there are certain pockets of the CPI index that likely dissipate in the intermediate term. In commodities historically, for example, the cure for high prices is high prices – as production of oil, metals, lumber, etc. increases to take advantage of those high prices, and supply debottlenecking will correct price imbalances.

Adding to near-term the pricing pressures, the frequently referenced supply shortages are playing out in the data. This is evidenced by the Inventories-to-Sales ratio being at all-time lows. Again, these supply-chain shortages are likely temporary as capacity comes back online. Also notice that a drop in this ratio happens to be a routine part of the business cycle post-recession (see 2009-10) as producers restock to supply rebounding demand.

Further fueling the supply imbalance, though, is that demand has proven to be far more robust at this point in the recovery than anyone predicted. In fact, nearly all measures of retail sales have recovered fully, and then some, to pre-pandemic highs. Even as recent as February 2021, a “full” recovery – not recovery plus – was not expected to occur until at least mid-year 2022.

An important driver of such rapid demand is personal incomes, which are running well above trend. The substantial support from stimulus checks, enhanced unemployment benefits and consumers’ suppressed ability to spend throughout the pandemic has created a ‘balloon under water’ effect of demand.

However, as activity shifts back to normalized levels and pandemic-related benefits begin expiring, which is already occurring in a number of states, we expect this demand-pull effect to moderate over time.

That said, we believe there is longer-term risk that the prices we pay for the basic needs, food, shelter, and services, may likely be stickier than the Fed is willing to acknowledge. And market participants tend to agree. Currently, the market’s 5-year inflation expectations are 2.5%, the highest reading since the Great Recession.

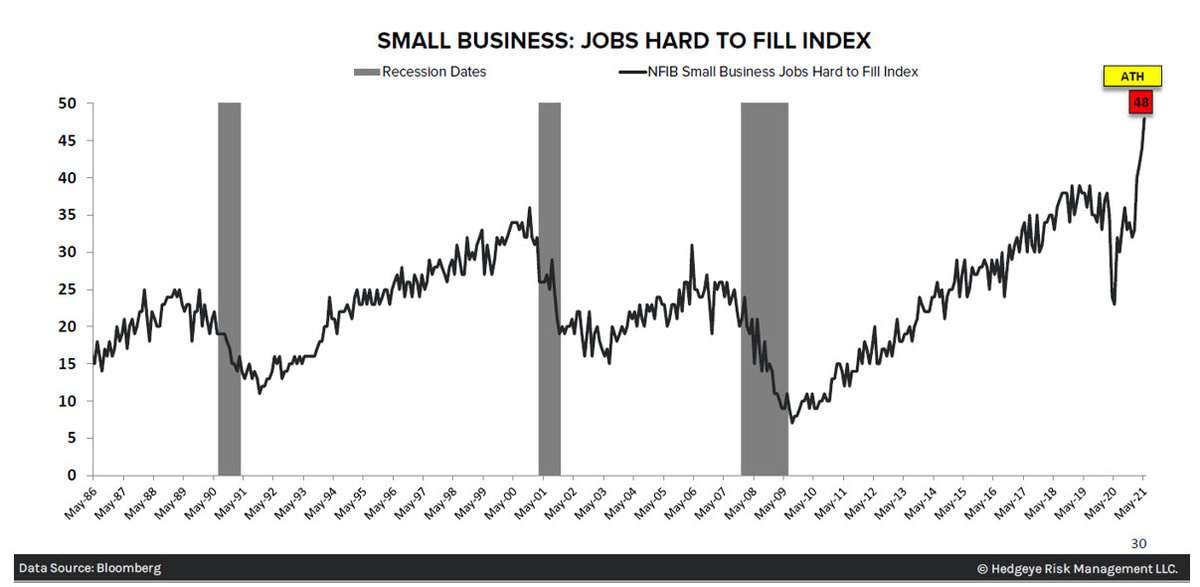

Furthermore, small-businesses’ ability to hire qualified workers has never been so difficult. The NFIB Small Business Jobs Hard to Fill Index touched 48 (out of 50), you guessed it, another All-Time High.

The solution of course is higher wages and passing those costs on to consumers. As the risk of longer-term labor scarcity evolves, it could create a cycle of higher wages, and with it, higher prices. Therein lies the risk of silent theft of our purchasing power.

That said, we are keeping our eye on how this data changes as pandemic-related benefits expire and workers return (or not return) to the workforce. To be determined.

Editor's Note

Michael Aroesty CFP® joined DBR & CO in 2010 and serves as both Investment Committee Chair and Chief Operating Officer. Michael has oversight and responsibility for the communication of the firm’s research and asset allocation decisions. As a Senior Financial Advisor, Michael also works with a select group of high-net worth individuals and institutions, providing wealth management and financial advice to help those individuals meet their goals and objectives. Michael holds a B.S. degree from Williams College, where he was the starting goaltender for the Ice Hockey Team.