Below is a complimentary Demography Unplugged research note written by Hedgeye Demography analyst Neil Howe. Click here to learn more and subscribe.

|

American and Chinese megafirms have left corporate Europe in the dust. Europe used to boast several of the world’s largest multinationals, but now European firms barely appear in the top 20--and hardly ever in the top 10. (The Economist) |

NH: The Economist starts out this essay with a marvelous anecdote about 29-year-old Steve Jobs visiting Europe in 1985. In a media interview, he offered some advice to his hosts.

He opined that government bureaucrats make lousy investors and that European capitalists would do well to offer budding entrepreneurs more second chances. The Europeans smiled indulgently, wondering what this abrasive new-age yuppie could possibly know that they didn't.

Thirty-five years later, Apple (APPL) is worth more than all 30 firms in the German blue-chip DAX index. It's worth almost as much as all 40 firms in France's CAC. The story raises an interesting question.

Americans once feared that European corporate giants were destined to become fearsome competitors. Whatever happened to them?

The basic economic backstory of the last several decades can be simply told.

It's the speedy rise of China, along with several other Asian-Pacific EMs, which now rival the size of the slower-growing high-income incumbents, mainly consisting of North America and Europe.

So if we had been looking ahead from 1980 or 1990 knowing this future, our baseline expectation would have been that the universe of largest firms would see more from China and its neighbors, and proportionally fewer from every other region.

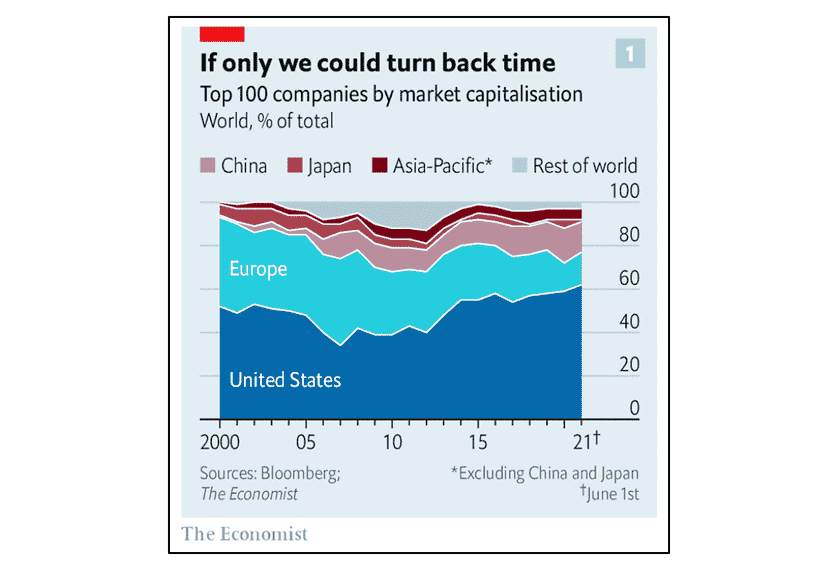

But that's not what happened. Take a look at this tabulation (by Bloomberg) of the top 100 global public companies by market cap.

Yes, China is claiming a larger share of the top global firms. So, to a lesser extent, is South Korea and Taiwan. Together, since 2000, the Asian-Pacific EMs have risen from almost nothing to roughly 20% of the top-100 market cap. And yes, incumbents like Japan are proportionally and gracefully declining.

But otherwise the picture among incumbents is a study in contrasts. Europe, on the one hand, has seen a dramatic drop from about 20% in 2000 to barely 8% today.

America, on the other hand, has actually gained on the rest. It started off the 21st century at around 57%, briefly lost ground before and after the GFC (mostly due to USD weakness), and has since come roaring back to about 60% today.

In truth, when you look only at the very biggest firms, the picture looks even bleaker for Europe than this chart suggests. Among the top ten global firms, Europe used to have at least one, and sometimes two or three players, every year.

Until 2014, when energy prices collapsed, Royal Dutch Shell (Neth/UK) was almost always among the top ten. Swiss powerhouses like Nestlé, Novartis, and Roche made frequent appearances.

And what happened to all those pre-GFC names that sometimes made the top ten? Like HSBC (UK), BP (UK), Vodafone (UK), and Deutsche Telekom (Germ).

For a trip down memory lane, let's not forget 1999, when four European names made the top ten: British Telecom (UK) and Nokia (Finn) as well as BP and Deutsche Telekom.

Now comes this arresting fact: Since Q3 of 2015, not a single European firm has entered the global top ten in any quarter. Nearly all the other top ten have been US firms, now regularly joined by Tencent and Alibaba (China) and the hot new star of 2021, TSMC (Taiwan).

Broadening our list to the top twenty doesn't really change the picture. Once upon a time, Europe regularly placed four to five companies in the top twenty. Today, Europe has exactly one: the French fashion giant LVMH, hanging on at #19.

So what's going on? Why have Europe and America gone in such different directions in their ability to grow world-class corporate giants?

We can point to differences in economic performance, but these probably aren't decisive.

To be sure, Europe is facing stronger demographic headwinds--that is, slower demographic growth--than the US. Since 2000, the working-age population (age 15 to 64) in Europe has shrunk by -2.4% while in the US it has grown by +7.5%. Advantage: US.

Yet Europe has experienced special tailwinds of its own since 2000, in particular the adoption of a single currency and the steady expansion of the EU common market to include new members. (Until Brexit, to be sure.)

If productivity gains among its richest members didn't always match US gains (which have not been impressive in recent years), this deficiency was more than compensated by faster catch-up growth among new central and eastern European economies. Advantage: Europe.

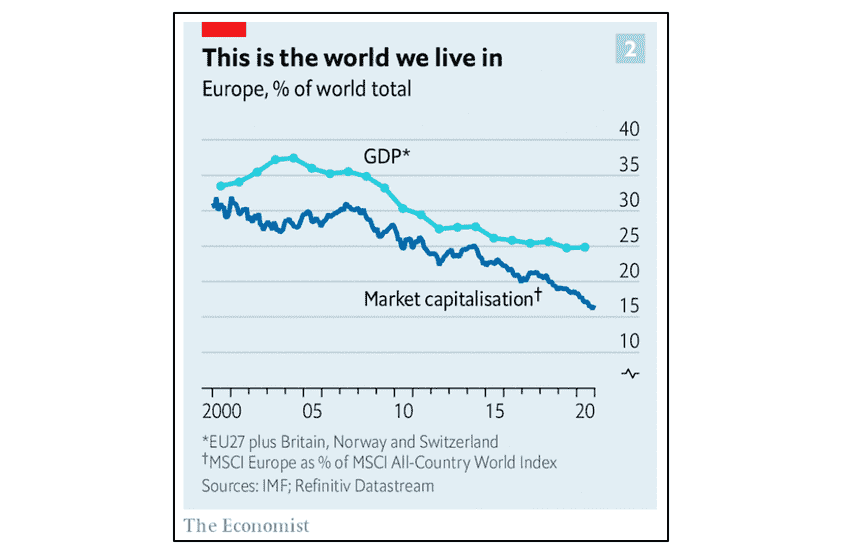

Overall, in constant dollars, US and EU GDP growth over the past two decades has been about the same. But only in Europe has top corporate market cap fallen far behind GDP growth.

To find better explanations, it helps to shift our attention to the top global firms themselves. By just focusing on the US winners at the very top (APPL, MSFT, AMZN, GOOG, and FB), we can't help but notice that America maintained its lead by dominating the most revolutionary economic shift of our era, into digital tech. Meanwhile, Europe merely looked on.

What does Europe have in the top 100 that competes in this space? Not much.

There's SAP (#76), Germany's enterprise software giant, a solid but hardly cutting-edge player. There's Prosus (#81), a little-known Dutch consumer-internet conglomerate. And, if you count hardware, there's ASML (#29) another Dutch firm that builds photolithography systems for the semiconductor industry.

That's pretty much it.

Many European CEOs accept this judgment, hoping that it may have been a single instance of bad luck from which Europe will in time recover. But that's probably a cop out.

The Economist argues, rightly IMO, that Europe's failure to develop competitors in this vast new sector is not a mere accident of timing. Its roots lie a lot deeper, in Europe's pervasive commitment to capitalism without risk.

One sign of risk aversion is a reluctance to fund or encourage new ideas. (Back to Steve Jobs, again!) So let's look first at the dearth of start ups in Europe. According to Pitchbook, VCs worldwide have backed 661 companies over the last decade that later went on to exceed $1B in market cap.

Guess how many of these companies are European? Only 78, worth only 8% of the later aggregate market cap of all these unicorn winners.

Once launched, a European newcomer is later less likely to dethrone the old guard. Consider: Of the world's 142 listed firms now worth over $100B, 43 were started in the past half-century. 27 were in America, and 10 were in China.

Yet only one was in Europe: SAP (founded in 1972, just barely within our 50-year window). Here's another fun fact pointing in the same direction: 5 of Europe’s richest 10 billionaires inherited fortunes. In America, 9 of the top 10 are wealthy solely due to the firms they founded.

Maybe it's no accident that so many of Europe's top-100 winners prosper in yesterday's industries, with little hope of seeing a brighter tomorrow. All four of France's top-100 are venerable fashion brands, from Louis Vuitton to L'Oréal to Hermès to Dior.

Belgium's national champion, AB Inbev, epitomizes the sort of big-brand beverage that young people are no longer drinking. Nestlé is a wonderful company, a Swiss treasure near to the top of the European list. It is not, however, the next big thing of the 2020s.

Even when Europeans seem perfectly situated to dominate a new trend, they swing and miss--or, more often, just stand there on a called strike. This suggests that risk aversion may be intrinsic to the European managerial style.

Italian brands like Lavazza and Illy have always been legendary in the Latin world of coffee enthusiasts. So why was it Starbucks, a firm out of chilly Seattle, that figured out how to turn this enthusiasm into fat global cash flows?

Europeans have always been crazier about electric cars than Americans, so why is Tesla now worth more than 4X VW? Going down the list, why does Unilever continue to struggle against P&G, Adidas against Nike, or Carrefour against Walmart or (even) Costco?

European CEOs often complain about the unwillingness of workers to work hard and take risks due to excessive state regulations and safety nets. But they ought to ask harder questions about their own culture.

How many of them are willing to stake their livelihood on an imagined future before the rest of the world already sees it happening? Why are European banks, who now sit on tons of cash, unable to find worthy borrowers?

As for the advantage Europe was expected to enjoy from its single currency and the expanded reach of its common market, well, this turned out to be mostly hype and ballyhoo.

Post-Maastricht, Europe remains an aggregation of separate national languages and cultures, with nothing like the same degree of integration as America or China or Japan.

That's why so many European firms, after dominating their own country, go outside Europe to seek further sales.

Multinationals in western Europe now derive half of their income from outside Europe, up from one quarter in 1997. American multinationals still derive 70% of their income at home.

The vaunted EU "scale advantage" has thus been slow to materialize. Oddly enough, it's Switzerland, a tiny landlocked nation having no connection to the rest of Europe, that has become the most extraordinary per-capita creator of global titans. Brussels may be loathed to admit it, but without the Swiss and the Brits, Europe would be left scrambling for a fig leaf.

So does all the evidence weigh in against the competitiveness of corporate Europe? Are there any facts we might mention that would qualify this adverse judgment? Yes, I think there are two. The Economist does not mention them, but I will.

One fact in Europe's favor is this.

Historically, Europe's version of capitalism has never rested on public equity to the same degree as America's. Europe has always leaned more toward private equity with financing from big banks. In recent years, private equity has grown more popular both in America and Europe.

This doesn't explain away the low turnover of Europe's biggest winners. But it does suggest that private firms (like Germany's famous family-owned Mittelstände) play a larger role in Europe's economy than they do in America's.

And that may lead us to misread some of the public-company comparisons. Among public companies, for example, it's hard to find European competitors to Walmart and Costco.

But such a comparison would overlook the family-owned Schwartz Group, the fourth-largest retailer in the world by revenue and the owner of Kaufman and Lidl. It would also overlook privately held Aldi Sud and Aldi Nord (aka Trader Joe's in the US). US retailers take these German competitors very seriously indeed.

The other fact is that the mushrooming market cap of the American superstars may, in part, be generated by rising market concentration and pricing power.

To this extent, the soaring valuations of such giants as Apple, Amazon, Alphabet represent future income transfers from consumers to owners--not consumer surplus generated by economic efficiency. They represent dysfunction, not function.

Most Europeans certainly believe this to be the case, which is why their regulators are working overtime to rein these US firms in. Personally, I think they make a pretty good case. And I have written about it. (See "The Inexorable Triumph of Bigness," "Antitrust Threats Against Apple Heating Up," "Declining Business Dynamism: A Visual Guide."

Yet whatever hubris has overcome the Silicon Valley CEOs at the top of the global hierarchy--and I can easily imagine many non-Americans find them insufferable--Europeans need to face up to the new reality. America is not the root of their problem.

The US and China aren't overtaking them merely due to antitrust violations. And well-run family firms won't retip the global balance of power in trade negotiations with Washington or Beijing.

If current trends continue, Europeans may wake to find themselves no longer able to change course--and the rest of the world no longer caring much about their collective economic interests.

| To view and search all NewsWires, reports, videos, and podcasts, visit Demography World. For help making full use of our archives, see this short tutorial. |

* * *

ABOUT NEIL HOWE

Neil Howe is a renowned authority on generations and social change in America. An acclaimed bestselling author and speaker, he is the nation's leading thinker on today's generations—who they are, what motivates them, and how they will shape America's future.

A historian, economist, and demographer, Howe is also a recognized authority on global aging, long-term fiscal policy, and migration. He is a senior associate to the Center for Strategic and International Studies (CSIS) in Washington, D.C., where he helps direct the CSIS Global Aging Initiative.

Howe has written over a dozen books on generations, demographic change, and fiscal policy, many of them with William Strauss. Howe and Strauss' first book, Generations is a history of America told as a sequence of generational biographies. Vice President Al Gore called it "the most stimulating book on American history that I have ever read" and sent a copy to every member of Congress. Newt Gingrich called it "an intellectual tour de force." Of their book, The Fourth Turning, The Boston Globe wrote, "If Howe and Strauss are right, they will take their place among the great American prophets."

Howe and Strauss originally coined the term "Millennial Generation" in 1991, and wrote the pioneering book on this generation, Millennials Rising. His work has been featured frequently in the media, including USA Today, CNN, the New York Times, and CBS' 60 Minutes.

Previously, with Peter G. Peterson, Howe co-authored On Borrowed Time, a pioneering call for budgetary reform and The Graying of the Great Powers with Richard Jackson.

Howe received his B.A. at U.C. Berkeley and later earned graduate degrees in economics and history from Yale University.