The following is a post written by our Hedgeye Financials team, led by Josh Steiner, on the impact of QE2 on consumer spending through 2011. The analysis shows that the modest impact on consumer spending resulting from QE2 may not be worth the significant opportunity cost (for savers) associated with longer term rates.

When $2 Trillion Buys You $3 Billion

We think it's conventional wisdom that when long-term rates are low it drives high volumes of refinancing activity, which puts significant incremental disposable income back into consumers' pockets. While this was true back in 2003, we think investors will be surprised to find out just how little it will add this time around, especially when comparing 2011 to 2010.

Low Long-Term Rates (i.e. Refinancing) Are Not the Elixir the Market Thinks They Are

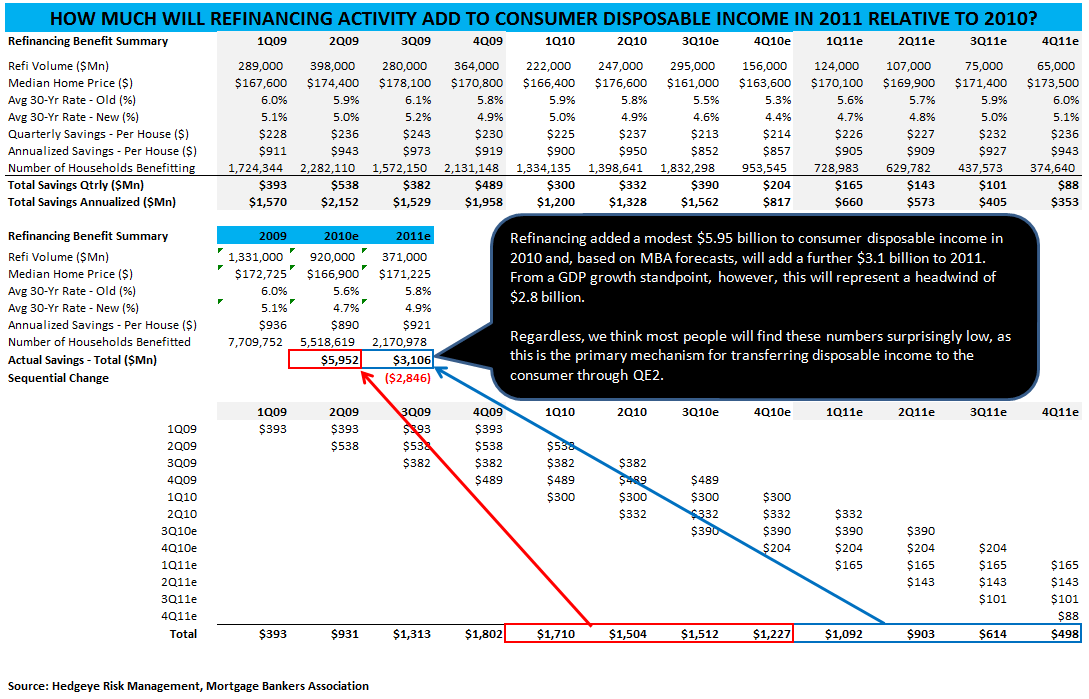

In the table below we've mapped out precisely how much additional money consumers will have from refinancing opportunities. We've used MBA estimates, which, to be fair, have generally overestimated activity in the past. The takeaway is that based on their estimates for refinancing volume over the remainder of this year and throughout next year, we expect a very modest increase in disposable personal income of $5.9 billion in 2010 (roughly 4 bps of GDP) and an even more modest boost of $3.1 billion (2 bps) for 2011.

Considering that QE2's only direct stimulative property for consumers is in boosting the housing market and consumer spending through refinancing activity, we were somewhat surprised to see just how paltry the benefit would be ($3 billion) especially when juxtaposed against the rumored cost of QE2 (~$500 billion to $2 trillion).

For those who think the MBA's rate forecasts and commensurate refi volume assumptions are overly conservative in light of the rumored scale and scope of QE2, consider that in 2010 mortgage rates fell 40 bps and drove only $6 billion in incremental disposable income. If we assume that 2011 sees mortgage rates fall another 40 bps, averaging 4.3% for the whole year, this would drive roughly $6 billion in further disposable income, only $3 billion higher than our $3.1 billion estimate. In other words, we just don't see how QE2 can drive enough incremental spending power to either move the needle on GDP or justify the profound cost.

Our Methodology

We've used MBA forecasts for refi volume and 30-year mortgage rates, and we've even used their home price assumptions (basically flat), which are in sharp contrast to our own (down). Based on this, we show there being 2.2 million mortgages being refinanced in 2011, down from 5.5 million in 2010 leading to a total annual payment reduction of $3.1 billion in 2011, down sequentially from the $5.9 billion boost it gave to 2010. We've assumed, based on Freddie Mac data, that, on average, people save 90 bps on their rate when they refinance. We've also assumed that everyone is in a 30-year fixed rate mortgage and that everyone is refinancing at 80% LTV.

It's worth pointing out that there is a not immaterial opportunity cost associated with lower long-term rates. Namely, the savers in this country are earning lower returns on their deposits. While it's difficult to quantify precisely what this opportunity cost is, we estimate that it is in the billions of dollars and likely exceeds any aggregate savings from refinancing activity.

We recognize that the goals of QE2 are twofold: to inflate asset prices by crowding out whatever asset class the Fed decides to monopolize for the next 6-24 months and to transfer lower borrowing costs to the consumer. The point of this note is to call out how small the actual transfer will be.