R3: REQUIRED RETAIL READING

November 1, 2010

RESEARCH ANECDOTES

- According to the Gallup-Healthways Well-Bing Index, “very religious” Americans have the highest levels of wellbeing (healthiness). 44% of Americans fall into the “very religious” category, attending church/synagogue/mosque at least once per week.

- Add Prada to the list of footwear brands that allows its customers to create their own customized shoes. The shoes are available in 16 colors and four different materials.

- According to a study by Equation Research, nearly 75% of CEO’s are looking outside the industry for retails’ next generation of leaders as retailers face increasing pressure to think outside their own four-walls to stay competitive. One of the key challenges will be attracting top talent, which 90% of those surveyed are saying the industry is failing to accomplish due to more attractive and lucrative options elsewhere.

OUR TAKE ON OVERNIGHT NEWS

Adidas HQ For Sale - Adidas America Inc. has put its North Portland headquarters up for sale, according to a report in the Portland Business Journal. The company is looking to lease back the facility a money-saving move and a spokesperson said the brand remains committed to the Portland region. According to a flyer announcing the property's availability, Adidas is looking for a buyer that will lease the eight-year-old, 320,000-square-foot campus back to the company for 10 years. "There are several business and financial reasons we are considering a sale-leaseback transaction, the most important being that it would free up funds which we can reinvest in our brand, employees and community in which we operate," said spokeswoman Lauren Lamkin, in an e-mail to the Portland Business Journal. "Adidas remains committed to continuing our strong local presence in Portland. According to the flyer, Adidas would pay $15 per square foot in rent, including 2%annual escalators, providing the eventual buyer with first-year operating income of $4.8 million. Adidas bought the site of the former Beth Kaiser hospital at 5055 N. Greeley Ave. in 1999. The $90 million development opened in 2002, allowing the company to consolidate its offices in Northeast Portland and Beaverton. <SportsOneSource>

Hedgeye Retail’s Take: Tough to argue with increasing one’s liquidity, particularly if you prescribe to further downside risk in real estate assets as outlined in our Hedgeye’s Housing Headwinds call.

Genesco Stock Repurchase Authorization - Genesco Inc. announced that its board of directors has authorized it to repurchase up to $35 million of the company's common stock. The authorization replaces the remaining balance of a previous $35 million repurchase program authorized in Feb. 2010, pursuant to which the company has repurchased approximately 844,000 shares at a total cost of approximately $24.2 million, including approximately 435,000 shares repurchased during the company's third quarter ending Oct. 30, 2010 at a total cost of approximately $13.0 million. <SportsOneSource>

Hedgeye Retail’s Take: Replacing an authorization updated earlier this year, this could be either a case of poor planning at the board level, or a bullish sign of internal expectations with shares near multi-year highs – either way, we view it as a positive.

PSS Launches ATR - Collective Licensing International last week relaunched the Above the Rim brand at an event held at the Hudson Hotel on W 58th St. in New York City. Former NBA players Daryl Dawkins, Anthony Mason and Bo Kimble attended the event along with several ambassadors as part of a new community-based grant program. The 21-year-old Above The Rim brand was purchased from Reebok in January. ATR will launch with a limited basketball footwear collection available now at Payless ShoeSource, which is also part of Collective Brands. The initial collection will include three key styles, the Pivot, Crosscourt and Rise. In addition, ATR will launch a full scale, premium basketball footwear and apparel collection geared toward specialty retail, department store and better sporting goods channel for Spring 2011 and backed by NBA star endorsements. The Spring footwear collection will be highlighted by the first signature ATR style created for Martell Webster of the Minnesota Timberwolves. Available in four colorways, his Elevate MW5 shoe will debut in Spring 2011 and will be featured in the return of ATR's advertising efforts. <SportsOneSource>

Hedgeye Retail’s Take: One of Collective Licensing’s many brands in the portfolio, we like the opportunity ahead for ATR to capture share in a category dominated by a single player – Nike. Coming off such a small base, even modest share gains would drive meaningful growth. With the brand left for dead by Reebok, Collective has done a solid job lining up known endorsements that should drive interest at a considerably lower price point than industry average.

Cherokee Goes China - California-based Cherokee Inc. has officially launched its namesake brand in China through a distribution deal with RT-Mart, the country’s largest supermarket chain by sales volume. “This is one of the biggest launches we have ever had in a huge country and with a very aggressive company,” Cherokee chief executive Henry Stupp said at a recent launch event, which featured a runway show of the fall-winter collection. “We felt right from the beginning that RT-Mart had a long-term vision for where they wanted to take this brand, and they respected the culture, the history and the legacy of Cherokee.” Cherokee inked the exclusive, multi-year international licensing deal last November with RT-Mart, a division of Ruentex Industries Ltd., a Taiwan-based textile company. French retailer Groupe Auchan SA also owns a stake in the hypermarket chain, which first opened in China in 1997 and now has 134 stores on the mainland. <WWD>

Hedgeye Retail’s Take: Smart move for a company and brand that is essentially an exclusive at Target. With growth 100% tied to TGT and it’s license, China makes a ton of sense.

Loehmann’s Running Out of Options - The Melville, N.Y.-based off-price chain has defaulted on its credit agreement and is exploring reorganization options, including a possible bankruptcy or prenegotiated restructuring. The discounter said Friday it was unable to complete a swap of old notes due next year for new ones due in 2014, falling shy of the 97 percent of required votes by 4.6 percent. Without completing the swap, the off-pricer was unable to make its October interest payment to bondholders, as it had planned to do today. Loehmann’s last month was able to get a 30-day extension on its October interest payment in order to execute the swap. Istithmar, the investment arm of Dubai World, which owns Loehmann’s and Barneys New York, was expected to provide additional funding for the beleaguered retailer had the transaction been completed. Loehmann’s said Friday it was in discussions with certain bondholders and Crystal Financial LLC, its revolving credit lender, regarding its options. “While this dialogue has been generally constructive to date, there can be no assurance that these negotiations will be successful,” the company said. Jerald Politzer, chairman and chief executive officer of Loehmann’s, could not be reached for comment Friday. Earlier last month, the retailer said it had the approval of a requisite number of bondholders to close up to 15 stores over the next year. It currently operates 60 stores in 16 states. <WWD>

Hedgeye Retail’s Take: With the competitive landscape becoming more consolidated (Syms/Filene’s Basement) and the rich getting richer (ROST/TJX) it’s not surprising that Loehmann’s struggle for survival may ultimately be nearing an end.

Patagonia Driving Green Awareness - Later this month, Patagonia catalogue shoppers will be among the first to find out about the company’s Common Threads Initiative. Instead of just hailing the benefits of recycling and reusing clothing, the program is also meant to encourage consumers to think twice before they buy something new. “Don’t buy this jacket unless you really need it” will be one of the cautionary messages used on hangtags, posters and other in-store signage. Self-defeating as that might sound, founder Yvon Chouinard said this unconventional approach will “increase my business like crazy,” namely because the brand will cut into competitors’ sales. Over the past few years, the recession has made people more conservative about spending, more interested in long-lasting and better-quality items, he said. “We want people to imagine our lives consuming less and living simpler lives based on what we need as opposed to what we want,” said Chouinard, whose company has donated 1 percent of its annual sales — $40 million to date — to environmental organizations for years. The brand’s four Rs — reduce, repair, reuse and recycle — will be fleshed out in the holiday catalogue, which ships to about 1.2 million shoppers Nov. 15. To reduce, Patagonia is recommitting to making durable, multifunctional clothes that stay reasonably in fashion. Repair guarantees that if a zipper fails before a garment does, the company will fix it for free. As part of its reuse effort, the brand will help provide a way for shoppers to sell, trade or donate garments they no longer want. <WWD>

Hedgeye Retail’s Take: Check out Patagonia’s blog for another interesting initiative which tracks the manufacturing of its garments by country and by component. If you’ve ever wondered how complex it is to make a piece of outerwear (and in a social responsible way) then this is worth a look.

Holiday Spending Forecasted to Rise Per Deloitte Survey - Consumer spending during this year's holiday season is expected to be slightly higher than in 2009, despite worries about the general state of the economy, according to Deloitte's 25th Annual Holiday Survey. The survey found that 62% of those questioned plan to spend more or the same on the holidays, up 11% from Deloitte's 2009 holiday survey and the highest level since 2006. The average total holiday spend per consumer is expected to grow to $1,160 this year, up from $1,145 in 2009. Consumers plan to spend a total of $466 on gifts, the first increase since 2004. However, the average number of gifts fell for the third consecutive year, to 16.8. Consumers hold a conservative outlook on the U.S. economy, with nearly four out of 10 (39%) of those surveyed expecting the economy to improve next year, down from more than half (54%) who anticipated an improvement at this time last year. Two-thirds (66%) of consumers surveyed indicate their household financial situation is the same or better than last year at this time, a 10 percentage point rise from 2009. <SportsOneSource>

Hedgeye Retail’s Take: While the holiday is likely to end up being better than last year, we won’t know it until it’s pretty much over. Last minute shopping and post holiday deal scavenging will be bigger than ever.

November Key Month for e-Commerce - Forget Black Friday, the deal-crazy day after Thanksgiving when turkey-fattened holiday shoppers scour the web and race into stores in search of the most outrageous deals. For online retailer Newegg Inc., the holiday effort really kicks off Monday with a month of deals the e-retailer is calling Black November. “We plan a pretty strong assault beginning Nov. 1,” says Bernard Luthi, vice president of Internet and product marketing at Newegg, which sells computer and electronics equipment. “We’re looking to offer strong bargains, category-wide promotions and specific hot deals. We’re sending the message that this is an opportunity to land some bargains before the crazy, mad rush begins the day after Thanksgiving.” He expects other retailers also will begin a big push this week. “Everyone’s looking to get a head start,” Luthi says. <internetretailer>

Hedgeye Retail’s Take: Despite the hype over November e-com sales, the largest online shopping day is expected to be Dec 14th aka Green Tuesday.

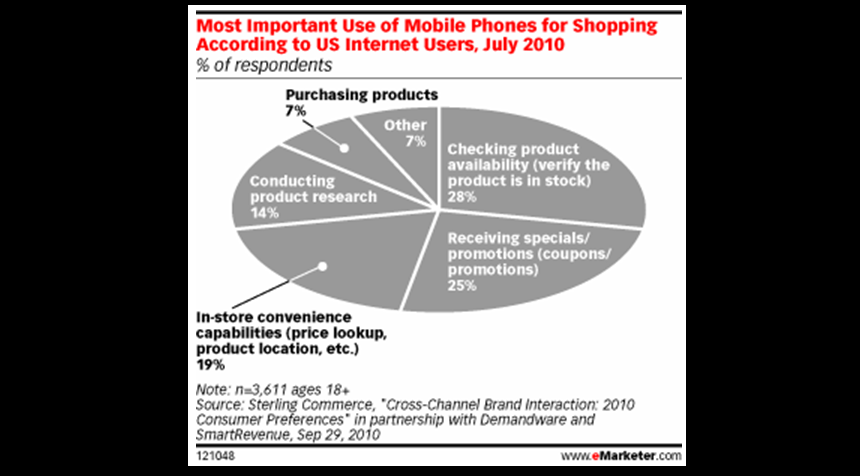

Mobile Functionality a Challenge for Retailers - US internet users place great demands on multichannel retailers. A majority expect to be able to track, modify, complete and order from any channel, according to a July 2010 survey from Sterling Commerce. Shoppers expect to use a variety of routes from research to purchase, especially during the holiday shopping season. And as smartphones continue to proliferate and more consumers use their phone as yet another shopping channel, retailers must be ready to offer capabilities through the mobile web or an app, or both. While many retailers focus on the price-comparison ability of smartphones, which allows in-store shoppers to check competitors’ prices, web users surveyed by Sterling Commerce said the single most important shopping function of a mobile phone was the ability to check whether a product was in stock. <eMarketer>

Hedgeye Retail’s Take: This should come as no surprise to any retailer who is in touch with their customers. Instant satisfaction and accurate information are now prerequisites for consumers. After all, a mobile platform should be viewed as merely an extension of desktop shopping.

Cambodian Strikes Likely - A local workers’ union in Cambodia plans to restart workers’ strike in front of clothing outlets and shops if the cases of the suspended workers are not solved. The secretary general of the Coalition of Cambodian Apparel Workers Democratic Union (CCAWDU) has been urging the government as well as garment industry representatives in an offer to help the union workers who had been suspended before the court’s verdict on the validity of the unions’ strikes came. The Ministry of Social Affairs had told CCAWDU to give them some time in order to solve the problem before restarting strikes and requested workers to respect the company rules and the Labor law of the country. According to the CCAWDU, ninety-four union representatives had been suspended from their jobs as they were related to the strikes that took place last month. The Secretary General of the Garment Manufacturers Association in Cambodia requested workers to remain away from the strikes which will do more harm than good to the industry. <FashionNetAsia>

Hedgeye Retail’s Take: Further labor unrest can only lead to one thing over time. Inflation.

China Footwear Brand Upgrades Image by Moving to Beijing - China’s footwear brand Kangnai has recently opened its first national flagship store in Beijing as a way to build itself a more high-end image. President of the group Zheng Xiukang said the opening of the Beijing store marks the beginning of the company’s transformation from a shoe maker to a high-end brand. The new “Kangnai Family” leather shoe collection will be sold at the newly opened store with prices ranging from CNY1200 to CNY1800. Currently, Kangnai has 2,900 retail stores worldwide and five hundred stores will be selling the new Kangnai Family products. The company is also planning to open more flagship stores nationwide. As the first Chinese footwear company opening stores overseas, Kangnai has 270 retail stores in the EU and the US, and 2,600 domestic franchise stores in China. <FashionNewAsia>

Hedgeye Retail’s Take: Yet another example of a Chinese company looking to tap into its domestic consumer rather than just being a “manufacturer.”