“Everything is changing. People are taking their comedians seriously and the politicians as a joke.”

- Will Rogers

This weekend during his 200,000 plus people “Rally To Restore Sanity And/Or Fear”, Jon Stewart joined the ranks of calling the press out as the Manic Media. “If we amplify everything, we hear nothing,” he said. “The press is our immune system. If it overreacts to everything, we eventually get sicker.”

I don’t think he was precluding the financial media from that statement either. At least in politics there’s a core competency in being raging Republican or Democrat. In the arena of finance, the incompetence of academic dogma and Keynesian policy is pervasive. What sell-side lovers amplify as “news” becomes a contra-indicator that we make money from. Thank God for that.

This week brings us the Super Bowl of market hope:

- Tuesday = Midterm Elections

- Wednesday = Federal Reserve’s Decision to Debauch The Dollar

- Thursday = European Central Bank and Bank of England Fiat Fool statements

Then on Friday, everyone will come back from their mid-term election and Dollar debasement parties in Washington DC to be hung-over by Hedgeye reminding them that neither Republicans or Quantitative Guessing will result in anything more than what we already have in this country, Jobless Stagflation.

Jobless Stagflation? What’s that? Don’t ask Barron’s – they decided to title this weekend’s cover story “Bye-Bye, Bear”…

No, I couldn’t make that up if I tried… and no, I don’t think the probability is very high that Barron’s is a leading indicator on the US stock market’s next major move either.

Let’s start Taking Sanity Seriously and understand what’s occurred since Ben Bernanke exercised his conflicted and compromised right to give the perma-bulls and financial media alike something to cheer on since the Jackson Hole Groupthink Summit on August 27th:

- The SP500 is up +13%

- The CRB Commodities Index is up +14.5%

- The Input Price component of Chinese manufacturing is up +15.5%

Seriously? Yes, this is a very serious level of expedited inflation folks.

But what does it mean? Doesn’t this mean that Burning The Buck at the stake is a credible, everybody-wins, strategy? Or does the Manic Media on the Western side of the world get paid to suspend disbelief and take the Groupthinker’s word for it that this is going to end in jobs?

The Manic Media doesn’t do buy-side equations, but we’ll give them another one to chew on now that our clients have their positions on:

QG = COGS inflation

Seriously. It’s sort of one of those IF/THEN equations that they can build upon using the equation we gave them a few weeks back:

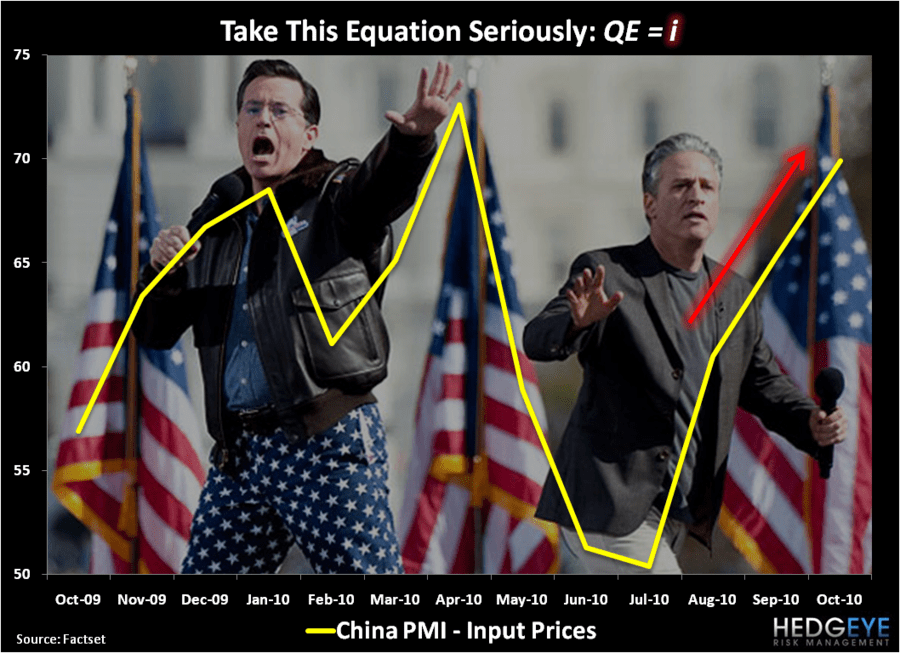

QE = i

Take these equations very seriously.

If, Quantitative Easing (QE) = inflation, and QE = QG (Quantitative Guessing), then QG = COGS (cost of goods) inflation. I know, I know. This is as brilliant a mathematical revelation as Morgan Stanley cutting its US Dollar forecast this morning “As The Federal Reserve Sets To Ease.” That and “Thirty Three Hour Race May Induce ECB Surrender on Weak Dollar” are top Bloomberg headlines this morning, fyi.

Notwithstanding the analytical incompetence of the political media on financial matters, this turns Jon Stewart into a very savvy politician, of sorts. Or is he a politician? Maybe he’s just simplifying the common sense signals that normal human beings have in their heads as Washington attempts to fear-monger you into believing that there is only deflation and, as a result, you should earn 0.17% on your hard earned savings in perpetuity?

Here’s what the Chinese think about this American style Burning of the Buck this morning:

- “US Dollar depreciation exacerbates currency war” –China Trade Ministry

- “China should buy gold, oil, to avoid US Dollar losses” –Chinese Business Reports

- “Yuan deposits rise as Hong Kong currency peg debate heats up” –Bloomberg Asia

Seriously? Yes, the Chinese are seemingly sane folks.

Oh, and they have the real-time price data to support it. There was a creepy little Halloween critter in China’s better than expected PMI reports last night (54.7 OCT vs 53.8 SEP) called COGS (cost of goods) that showed input prices rise to 69.9 in October versus 65.5 and 60.5 in September and August, respectively. At the same time, South Korea released a new high in their inflation report of 4.1% overnight versus 3.6% in September.

If you’re taking the global interconnectedness of markets and prices seriously, you’re seeing inflation rise, globally, as joblessness stagnates locally. This is called Jobless Stagflation. And we don’t think the Manic Media’s stock market cheerleaders will make that go away by the end of this week.

My immediate term support and resistance lines for the SP500 are now 1169 and 1192, respectively. In the Hedgeye Portfolio, I remain short both the US Dollar (UUP) and the SP500 (SPY). I’ll be a seller of all buy-and-hope oriented strength this week.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer