Favorable mix in Macau, higher gaming volumes in Singapore, and better cost controls drove revenue and EBITDA higher than our Street high estimates.

Not much to say other than Steve Wynn must be kicking himself again for not bidding on Singapore. Macau wasn’t too shabby either. Las Vegas was a disappointment but who really cares other than MGM shareholders?

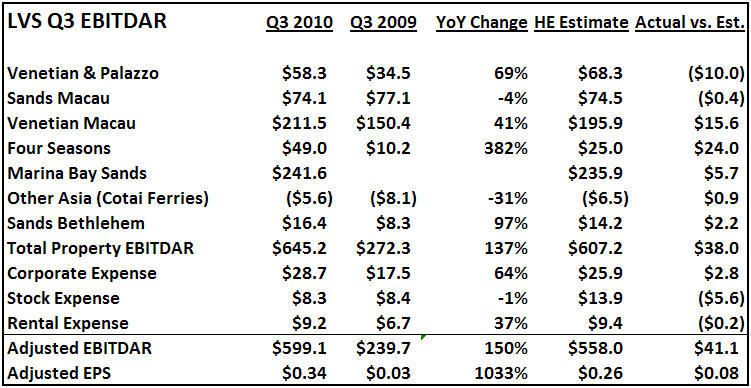

Venetian Macau revenues were $15MM above our estimate and EBITDA was $16MM better

- The revenue beat vs. our numbers came from

- Mass revenues coming in $9MM better

- Retail and other was $5MM better

- F&B was $2MM

- EBITDA was boosted by better fixed cost controls.

- We estimate fixed costs were $91MM down $1MM from 2Q and 11% YoY. We assumed that Venetian has lapped their ability to cut costs and that fixed costs would increase to $95MM.

- $5MM of lower commission payments to junkets due to a higher direct play mix which were completely offset by $6MM in higher taxes on better revenues

- Bottom line variable expenses were in-line with our estimate despite better revenues

- Direct play was 23% vs. our estimate of 21%

- High Mass hold benefited property revenues by $21MM and higher than normal hold benefited VIP gross revenues by $17MM and we estimate that the impact on EBITDA was about $19MM

Not much to add on Sands Macau as revenue and EBITDA were exactly in-line with our estimates

- Direct play was 14%, a few points above our estimate

- High hold on VIP helped revenues and EBITDA by $9MM and $4MM, respectively

- Slightly higher gross gaming revenues were offset by higher rebates which were 1% of RC

- Could be partly due to higher direct play

- Slightly higher non-gaming revenues were offset by higher promotional expenses

- Implied fixed costs increased 2% YoY to $47MM

Four Seasons revenues were $22MM above our estimate and EBITDA was double our estimate

- Why was our revenue number so off?

- Net VIP revenues were $15MM higher than we estimated due to a rebate rate of only 83bps vs. a rebate rate that was 101bps last quarter on hold of 3.07% and a rebate rate of 94bps in 1Q2010 on a hold of only 2.5%. The low rebate rate accounted for $10MM of the revenue difference while VIP gross revenues were also $5MM higher

- Retail & other revenue was $7MM above our estimate; basically doubling QoQ

- Why was EBITDA so off?

- Variable expenses were only $2MM higher than we estimated on a revenue beat of $22MMM since the lower rebate brought down the total commission rate

- Non-gaming margins are very high and non-gaming revenues were $6MM higher

- Fixed expenses were only $20MM vs our estimate of $25MM

- Put another way, last quarter, FS printed a $33MM EBITDA quarter with gross gaming win of $181MM and this quarter on $182MM of gross gaming win, they printed $49MM

- Direct play was only 42% vs. our estimate of 50%, and therefore hold was actually not low as we had estimated but high at 3.08%

- High hold boosted revenues by $11MM and EBITDA by $2MM

- Mass play was $2MM higher than we projected but hold was also off the charts at almost 30%

- High hold helped revenues by $4MM and EBITDA by $2MM

MBS reported revenues were $22MM higher and EBITDA was $6MM better

- Bottom line – handle and drop were stronger than we estimated and beat our numbers despite low hold

- Low hold depressed VIP gross revenues by $15MM and EBITDA by $6MM

- Rebates were 1.34% this quarter or $135MM (basically difference between calculated gross gaming revenues and reported net casino revenues)

- Fixed expenses were $145MM

Las Vegas net revenues were $19MM higher than we estimated but EBITDA was $10MM below our estimate

- Casino revenues were $7MM below our estimate and rooms revenues were $4MM below our estimate, but F&B, retail and other were $30MM better, while promotional was exactly in-line

- Operating expenses increased 20% YoY (Revenues- EBITDA)

- Rebates were 3.6% of gaming revenues and promotional expenses were 31% of gross gaming revenues

- Added over 200 slots sequentially at Venetian