The guest commentary below was written by Jeff Snider of Alhambra Investments on 6/7/21. This piece does not necessarily reflect the opinions of Hedgeye.

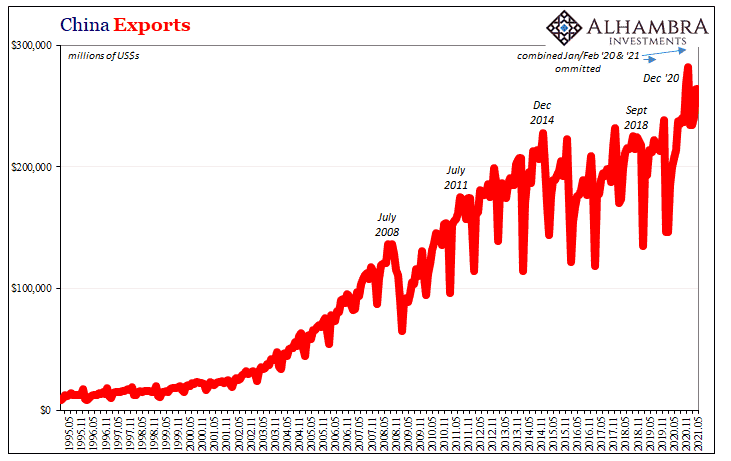

For the month of May 2021, China’s General Administration of Customs believes the total US$ value of exports exiting that country was an impressive-sounding $263.9 billion.

Compared to the US$ value of exports sent abroad in May 2020, this was a 27.9% increase.

But base effects; exports in May 2020 had been a little more than 3% below those in May 2019. The 2-year change, therefore, a less inspired 11.1% compounded.

This suggests China’s vast export sector has been bumped up no more than it had been a few years ago during the insufficient top of Reflation #3.

And that’s with everything being thrown into this global goods rebound largely emanating from the US; from rare earths to PPE stuff, a lot of one-offs have been included just to get to that $263.9 billion.

Furthermore, those same had stacked up much higher all the way back in December 2020. The GAC doesn’t seasonally adjust its figures, yet there’s still a recognizable seasonal pattern in them.

The jump in last December’s export levels still represents the most recent peak. In other words, five months into 2021 the latest data continues to indicate how that may have been the best it gets for the rebound.

What if it really is downhill from here?

Before thinking about that, there’s still China’s import side to consider. Over here, the annual number is even more impressive, nearly twice the growth shown in exports.

Rising 51.1% year-over-year last month, like all the rest of Chinese estimates (ex exports) these are huge numbers which otherwise appear to indicate a robust, intentionally government-fueled economic recovery consistent with what’s said to be behind 1970s-style inflation numbers at least in the United States.

The 2-year change in imports, though, this was only 12.4% (compounded) which doesn’t even come up to the better levels of Reflation #3.

Even all that’s supposedly going right in and around China via global trade and the mainstream view of its internal policy contributions, the best they’ve managed (so far) from the inside is importantly less than what wasn’t nearly enough for the global economy heading toward 2019’s more synchronized global downturn (and eventual recession).

Why isn’t it going so much better, so much less ambiguously?

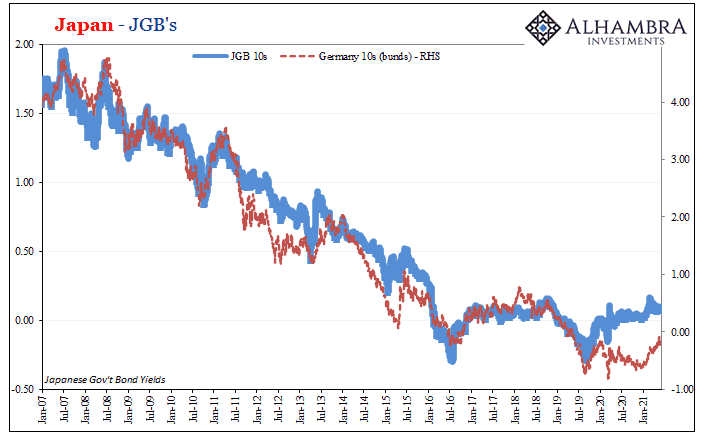

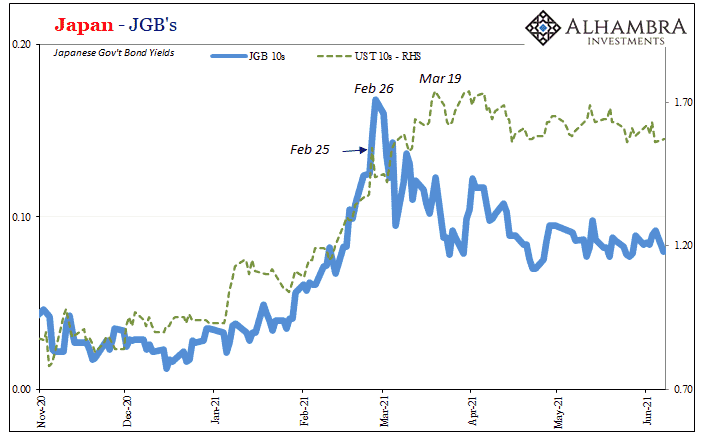

Two questions that combine to give us a data-side view of the post-Feb 24-25-26 anti-reflationary marketplace; a widespread global anti-reflationary marketplace (the only reflation trading in bond markets has been Europe).

While the media in the United States can’t get enough inflation talk, bonds around the rest of the world have actually pulled in those from the US lining up more negative answers to those two enquiries.

If December 2020, or thereabouts, does present the possible top of the 2020 recession rebound, it also would mean peaking well short of anything like a full and complete recovery.

Reflation that in comparison to past reflationary periods (considering the huge downside/contraction from which it began) comes up even less than those would account for bond yields behaving as they have in equal part short- as well as longer run considerations.

It’s not just Chinese trade terms nor limited to global trade across regions.

China’s economy as a whole continues to exhibit the same signs in both these dimensions, only starting with its near-term top somewhere around the end of last year and the beginning of this year (despite when reflation yields really picked up).

The other perhaps more important element being just how little that possible peak may have reached.

These possibilities are captured only-too-well by these various 2-year comparisons – including overall nominal GDP in RMB (IOW, it’s not just US$ trade terms which indicate shrinking possibilities as well as growth).

This measure, unlike estimates of real GDP, is less susceptible to artificial (read: political) influences or even targets.

The correlation between nominal China GDP and marginal export changes has been a very strong one, as anyone would suspect given how the Chinese system remains wedded to its export sector (realizing how in reality rebalancing is a hope or wish rather than rational analysis or design).

Nominal GDP had leapt 21.2% in Q1 2021 when compared to the recession-stricken quarter of Q1 2020.

Already you see their problem – in the first quarter of 2011, by comparison, after more than a year of what had been “recovery” from the world’s Great “Recession” that for China, anyway, wasn’t nearly as rough as it had been last year, the 2-year change was 18.8% compounded annual.

In Q1 2021, by contrast, the 21.2% one-year change followed what had been a nearly 7% decline last year for a two-year total of barely 7%.

Nominal. Bigger decline, actual decline, half the recovery speed? And half for an entire year now.

Nominal 2-year expansion has pretty much stuck around this number for each of the four quarters since the contraction (only the smallest, most suspicious of acceleration: from 5.4% 2-year in Q2 2020 to 6.3% then 7.0% and now 7.1%).

It’s hardly the roaring comeback otherwise pictured when peering through the highly colored lens of US goods or the equally distortive filter of 1-year base effects.

This is substantially less, significantly slower from China than even 2018 and 2019 when the “world” had been shocked to see such stubborn negativity posted by this crucial economic nexus.

As always, depending upon the Chinese for marginal growth has – since 2011 – been a difficult and ultimately losing proposition.

This does not appear to have changed in the aftermath of 2021; if it has, to this point it has only been a change in the sense of yet another longer-term downshift in results therefore very likely potential (a possibility only strengthened all the more by words and behavior of Chinese officials).

There has been this ongoing perception, the very one underneath all the inflationary hysteria, that the frenzy in the US goods economy is representative of conditions first in the rest of the American domestic economy as well as for the entire worldwide system.

In truth, as we see time and again in foreign figures – China most of all, a huge marginal chunk of any growth/anti-growth period – the US goods economy isn’t just an outlier, it is an extreme one.

The vast majority constituting the rest is really struggling.

The view instead from China, consistent with that vast majority, is a very lackluster return from the depths and one that may just have reached its fullest if disappointing speeds already some time ago.

This, along with money/liquidity risks epitomized by Feb 24’s Fedwire disruption and its Feb 25 impact on UST liquidity, would more than begin to explain the changing bond viewpoint.

Dealing in probabilities, it would then make perfect sense why global yields which had previously sprung suddenly into reflationary trading almost as suddenly jumped right out of them.

Or, more specifically, balance of probabilities that had been more favorable after last November, risks tilting toward a limited reflationary upside, tilted right back down again and remain steadfastly lower the longer it goes and the more China (and the rest of the world) fails to converge with US goods – despite having been artificially buoyed by that frenzy in US goods.

And if the US goods economy converges with everything else, as we keep asking, then what?

Whatever these increasing downside possibilities, which doesn’t necessarily mean more contraction or outright negatives ahead, the one thing they don’t contain is actual inflation either for the rest of the world let alone the United States.

None of this, however, will do much to sway the sure-to-be even more colorful interpretations of this week’s May US CPI figures.

EDITOR'S NOTE

Jeff Snider is Head of Global Investment Research for Alhambra Investments. Jeff spearheads the investment research efforts while providing close contact to Alhambra’s client base. This piece does not necessarily reflect the opinions of Hedgeye.