R3: REQUIRED RETAIL READING

October 26, 2010

As the policies in India allowing direct foreign investment begin to relax, expect to hear a whole lot more about expansion into the world’s second most populous nation. However, we note that the floodgates are not likely to open immediately or without restrictions. This will be a long, complicated process as Western companies attempt to accustom the Indian consumer to more modern means of distribution.

RESEARCH ANECDOTES

- “Green” products continue to be one of the largest growth categories in retailing. There are approximately 73% more green products on retail shelves this year vs. last, according to a TerraChoice study. Additionally, the same study notes that 95% of these products commit at least one of the seven sins of “greenwashing” (essentially making false claims about the greenness of the product”.

- Tommy Hilfiger is jealous of Ralph. In a conversation with Jimmy Fallon for Interview magazine he was quoted as saying, “"Every time I pass a Ralph Lauren store, I think, I know he's been in business for more than 40 years and I've only been in business for 25, but, boy, do I ever want what he's got,".

- Expect to see and hear about Nike’s latest 90 second commercial aiming to rehab Lebron’s image as the NBA season kicks off tonight. Like it or not, the controversy is already brewing. See the latest from Nike here: http://www.youtube.com/watch?v=cdtejCR413c&feature=player_embedded

OUR TAKE ON OVERNIGHT NEWS

Wal-Mart `Optimistic' India Will Allow Foreign Retail - Wal-Mart Stores Inc. Chief Executive Officer Michael Duke said he is “optimistic” that overseas companies will be allowed to invest in India’s retail industry. Wal-Mart and rivals including Carrefour SA and Tesco Plc are pushing India’s government to allow foreign investment after the trade ministry invited views from the industry on removing the restriction. The government’s discussion paper said in July that allowing foreign investment in retail will lower prices and benefit farmers. “The opening of dialogue the ministry has initiated is very productive, and I view that as progress,” Duke said at a press conference in New Delhi yesterday. Easing the rules on foreign investment in retail will help curb inflation and may lead to the creation of 3 mm jobs in India, he said today. India is the third most attractive retail market for global retailers among the thirty largest emerging markets. <bloomberg.com>

Hedgeye Retail’s Take: Despite the sheer number of “consumers” in India, we believe the effort to allow foreign direct investment will be one that evolves over time. We do not expect the floodgates to open overnight. Furthermore, given the underdeveloped infrastructure across much of the country, we believe it will take substantial time for WMT to build any critical mass in the world’s second most populous country.

Amazon.com Gets a Texas-Sized Tax Bill - Amazon is liable for $269 million in uncollected sales tax from December 2005 to December 2009, Texas says. Amazon disputes the bill in the latest skirmish in the battle over whether online purchases should be taxed. <internetretailer.com>

Hedgeye Retail’s Take: We continue to believe AMZN and other online only retailers are close to losing their tax free status. See our work on e-commerce for specifics on recent efforts to finally even the playing field between brick and mortar retailers and their online only peers.

Puma to Acquire Control of Chinese Operations - Puma said it would acquire full control of its China operations as it reported a 14.2% rise in third-quarter profits. In China, Puma said it would take full control of its joint venture with Swire Resources Ltd., in which it holds a 51% stake, effective Jan. 1. Financial terms were not disclosed. The activewear firm also raised its full-year 2010 sales forecast to a mid-to-high single digit increase, citing an improvement in the overall outlook for the fourth quarter. Revenues in the third quarter rose 16.5% with footwear up 6% cc, apparel up 1.3% cc and accessories up 25% cc. <wwd.com/business-news>

Hedgeye Retail’s Take: Add Puma to list of Western brands taking back full control over their Chinese operations in an effort to maximize the market’s potential.

Dick's SG Lays Out State-by-State Expansion Plan - In a filing with the Securities & Exchange Commission, Dick's Sporting Goods outlined a state-by-state plan for where it sees its potential to double its store count in the years ahead. Not surprisingly, its biggest expansion potential was seen in the West but sizeable growth was also forecast in Texas, New York, Maryland, Oklahoma, Arizona, New Jersey, Wisconsin, Louisiana, Iowa, Michigan and Illinois. More mature states were seen as Pennsylvania, Maine, Tennessee, Alabama, and Indiana. <sportsonesource.com>

Hedgeye Retail’s Take: With Dick’s plan looking for a doubling of the store base we wonder just how aggressive TSA will be with its IPO growth story. Overstoring the country with sporting goods boxes is something that always ends badly.

Under Armour Close to Deal for MLB Footwear License - Under Armour Inc. is close to completing a deal that would gain it the rights to manufacture performance footwear with Major League Baseball logos and the ability to use its stable of baseball players in advertising wearing MLB uniforms, according to the Baltimore Business Journal. <sportsonesource.com>

Hedgeye Retail’s Take: It appears that the “free” advertising done by players choosing to wear UA footwear may be running out of juice. The more formal arrangement would certainly give UA a boost in its effort to market the category more effectively and inline with other similar league partnerships, although keep in mind the cleated business is and will continue to be of secondary importance to the key footwear growth categories – running and basketball.

Walmart Expands E-book Offerings to Include the Nook and the Kobo - Walmart is expanding its ebook reader offerings in stores. This week, Barnes & Noble's Nook and Borders' Kobo hit shelves. The retailer began selling Apple's iPad earlier this month. Two versions of Barnes & Noble's Nook (the 3G and Wi-Fi) are being stocked at 2,500 Walmart stores, as well as online at Walmart.com. The retailer is also launching a Nook-branded ereading area in stores. The Nook Wi-Fi debuted in June. <licensemag.com>

Hedgeye Retail’s Take: With e-readers making their way into the mainstream via WMT, it’s only a matter of time before we see pricing of the actual books start to erode. Mass adoption will only occur at a price point that makes the content a compelling purchase for not just higher-end consumers.

Athletic Propulsion Lab's Concept 1 Sneaker Benefits From NBA Ban - With the NBA officially banning players from wearing Athletic Propulsion Labs’ Concept 1 sneakers last week, business has only gotten better. APL debuted in 2009, with the Concept 1, which is targeted to basketball players and has a patent-pending “propulsion device,” a spring technology under the ball of the foot that its makers claim increases vertical leap. The NBA has stated that the shoes give players an unfair competitive advantage. The decision by the NBA has created a considerable market opportunity putting the brand out there in the public consciousness. The company sold more shoes on the day the shoe was banned than the entire previous month. The day the ban was announced, “Athletic Propulsion Labs” and “Concept 1 shoes” were the fourth and fifth most searched terms on Google. The APL website was also unable to deal with the increased traffic and the site shut down for several hours. Expansion is in the works and only a question of strategy. <wwd.com/footwear-news>

Hedgeye Retail’s Take: Nothing like a negative turning into a major positive. A visit to the company’s website reveals the slogan “Banned by the NBA”.

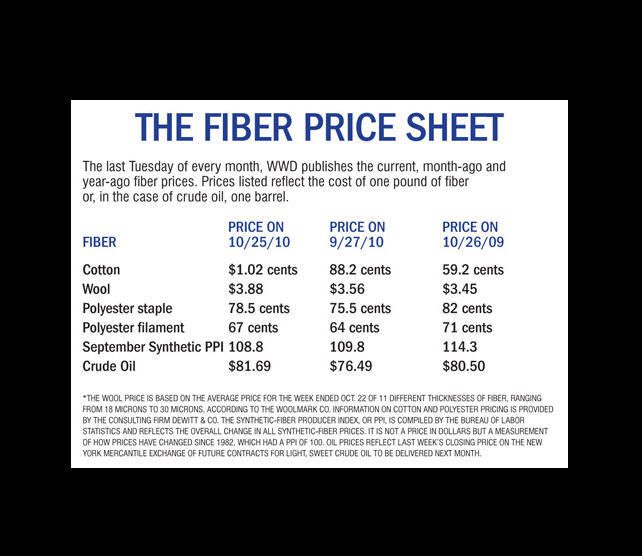

Cotton Soars to New High on China Cold - The fiber on Monday hit $1.2471 per pound, rising by 4.2pc, or 5 cents, which is the maximum allowed by the ICE exchange in New York. Chinese weather forecasts are saying that the current cold snap will last for at least another day. Prices rose 9pc last week, adding to the record 140-year high hit on October 15, after hail storms hit in the southern US. There are mixed views as to whether the current price spike will remain. Supplies have not been this tight since 1995 and prices are already up by 58pc in New York this year. There are six key reasons why the cotton price is so high: tightening US fundamentals, the battle for arable land, a deteriorating Chinese crop, the weak dollar, the Indian export ban and floods in Pakistan. <telegraph.co.uk>

Hedgeye Retail’s Take: Nothing new here except the record highs. We continue to focus on companies whose process may not have properly and proactively accounted for such a dramatic increase in this core textile commodity.

EU To Launch New Labeling Law - The European Union is considering launching new labeling laws during the first half of 2011. According to reports, EU representatives voted 525-49 last week in favor of a country of origin labeling law in order to ensure that it is clear where imported goods such as leather, furniture and shoes are made when they are being sold in Europe. Countries in southern Europe such as Italy and Spain have been pushing for this legislation for some time in a bid to protect the European market from cheap imports, particularly from Asia. However, nations such as the UK and Sweden have campaigned against the measure, which they believe is protectionist and threatens competitiveness. <fashionnetasia.com>

Hedgeye Retail’s Take: Despite improved labeling, it will now be even more clear to see how many goods are coming from Asia. Labeling alone won’t help the Europeans protect their manufacturing base so long as cost advantages remain in place driving production away from their borders.