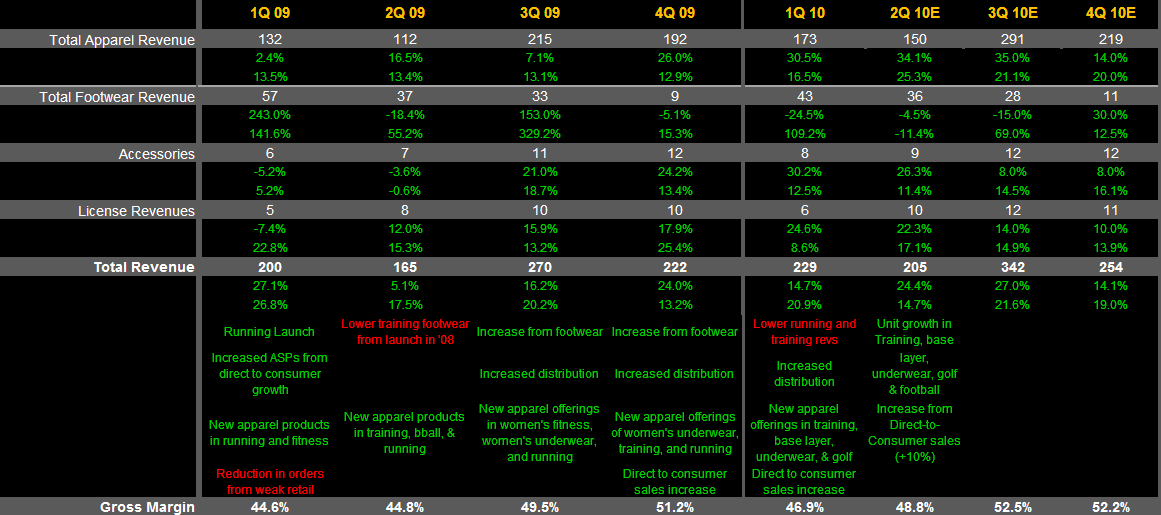

The quarter looks really good – we’re at $0.68 vs. $0.60E driven by the top-line with upside in gross margin. We’ve been a big fan of the story as evidenced by our $1.70 estimate for next year when the Street was at $1.10 and the stock was trading around $35 – since then, consensus has come up to $1.40. In addition, while product in the marketplace has strong momentum, the reality is that UA’s top-line comparisons get materially harder over the next 4-quarters and our estimate is ~20% below the Street next quarter.

Nit-picking the growth on a company that’s putting up such stellar numbers could be the equivalent of complaining about the trunk space in a new Ferrari, but the reality is that we’re going to be seeing a decelerating rate of growth in sales – given that shares are trading at a ~35x 2011 EPS, this flat out matters. This is not a short into the quarter – repeat, this is not a short into the quarter, but as any bears out there get squeezed, we’re more inclined to get involved on the short-side post the event.