It's going to be all about topline growth from here because it looks like there is little in the way of cost cutting available.

Despite the "less bad" spin:

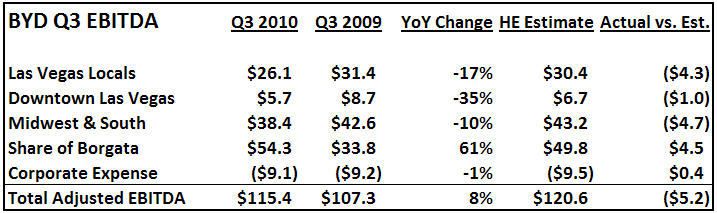

- Las Vegas Locals EBITDA margins suffered their worst decline of the year – dropping 290 bps YoY to just 17.9%.

- For the 1st time in years, costs actually increased, up 0.1%

- In Downtown, EBITDA margins declined 490 bps YoY to just 10.9%

- Expense control was tight – only up 0.1% but again there’s no room left to cut

- Midwest and South had relatively their best quarters

- Margins only declined 1.2% YoY

- However, costs only decreased 0.5%

- 4Q has the first “easy” comp of the year

Borgata:

- Table hold was only 12.1% vs. an average 14.2% over the last 6 quarters. Low hold cost them $9MM in revenues and probably about $3MM of EBITDA.

- Operating expenses decreased 1% YoY

- BYD declined the option to buy the other half of Borgata - smart move in our opinion given the higher than expected multiple. We're not convinced the deal on the table will go through so BYD may get another crack at a lower multiple