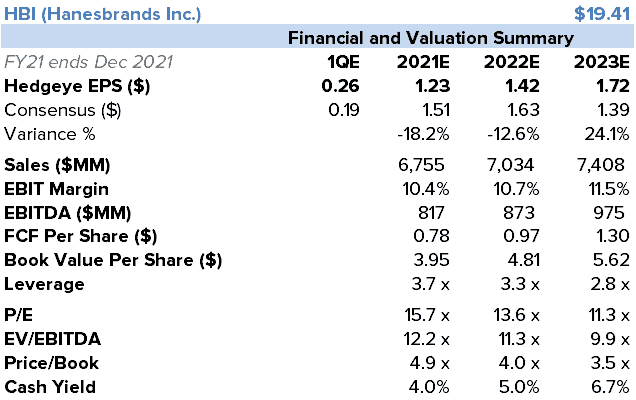

We’re removing HBI from our Best Ideas Short list. It’s an end of an era for this call, as we added as a Best Ideas Short on May 2nd 2016, since then the stock is down ~35%, with the S&P up 90% and the XRT up 80%. We’re wrong on the stock today as we were waiting for a full year guide to rebase margin and earnings, which we still think is coming on the May Analyst Day, but given how the theoretical bull case is shaping up we’re just not sure that event will mean a material enough stock selloff to warrant Best Idea status. A core tenant of our TAIL bear case looks to be reversing, which was secular share loss in core underwear. We’re not talking about recent shelf space changes, we’re talking about the opportunity from reinvestment in the brands that can drive organic growth and improved gross margin. The steps towards SKU rationalization and elevating marketing are notable changes vs the historical strategy and with the narrative changing we think the market is going to give this an elevated multiple vs recent years. As we look at the model today, we see 2021 EPS around $1.20 (the Street is at $1.51) and with the new management plan likely to mean the TAIL bear case has less teeth a fair multiple is likely between the low and mid teens. That’s a stock between $15.75 and $19.50. HBI is going down to our short bias list, that is at least until we see a pullback and/or earnings expectations lowered. Depending what we see/hear on the Analyst Day, this stock could actually go to the long side of our idea list – presuming the company lowers expectations for the year enough in that context.

Business Still Not Good

If the market is getting excited about the 1Q guide, we’d exercise caution. The company wrote down PPE, that they plan to sell in 1Q, alongside a margin guide ahead of expectations. 1Q is the very easy compare with no PPE sales last year, and cotton costs are a tailwind in 1H21 turning headwind as the year goes on. We suspect the full year guide will look nowhere near as good as 1Q in isolation. For 4Q20 results, on the positive side HBI had 2.8% revenue growth with an acceleration in Innerwear from 8.4% to 13.5% plus guided DD growth, and Champion returned to growth at +11%. On the negative side, EPS was down 25% YY even with $28mm in PPE, a 53rd week, and FX tailwinds. Guidance still implies anemic Activewear growth despite the positive commentary around Champion. Regarding the PPE write down, ending PPE as a business for HBI is the right move, but the market seems to be completely shrugging off the wasted capital.

We still think a 2021 guide down is coming. The CEO talked about being able to ‘lap’ PPE, but that seemed to simply imply replacing the sales. We think the model likely sees revenue up slightly, with quality gross margins but SG&A reinvestment driving margins down YY. Also keep in mind the raw materials trends. Cotton/oil in 1H should be a tailwind as lower costs around Spring will be flowing through the P&L, but come 2H and into early ’22 the raw materials costs will weigh on margins. Cotton is up from $0.51 to $0.88 over the past year. There is still some distribution risk from door closures (JCP, M, KSS?) though much has been trimmed in 2020, and there are tough compares in the mass channel (be looking for that detail in the 10-K). Between restructuring charges, PPE puts and takes, and raw materials volatility, it’s going to be messy model year. The revenue rate of change in the core should look good, but the total earnings model likely won’t be one to get excited about.

Bull Narrative Is Taking Shape

We think to buy here you clearly need to be looking beyond 2021, but that Bull Case is starting to look a bit more appealing…

- SKU Rationalization and concentration on the core with brand investment to protect/gain share and drive gross margin improvement.

- Grow Champion, which is coming off an awful year, meaning clear multi quarter/year growth runway.

- Exploring strategic alternatives for Europe Innerwear, would likely means small EBIT dollar pressure but margin upside, and can be a way to raise some cash and pay down debt.

- Further deleverage of the balance sheet from cash generation, margin and earnings growth off of to be reset base.

Management will likely control the message by presenting the business ex. PPE from 2020, representing a much better look at the underlying than the reported P&L, and HBI is also likely to have restructuring charges elevating adjusted earnings. It will be a little messy for a year or so, but the market will likely give the new management team the benefit of a doubt as it puts its new plan in place.