Our Risk Tracker gauges key risk measures across the various banking systems around the world.

Note, we plan to publish the Risk Tracker on a dynamic basis, contingent with evolving conditions in markets, i.e. more frequently during periods of acute stress and less frequently in periods of relative calm.

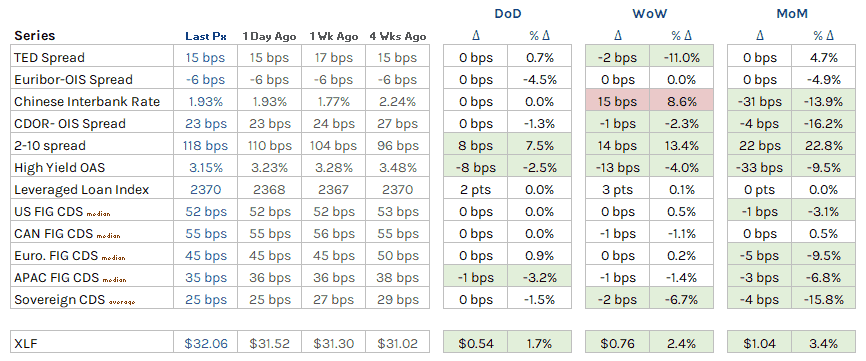

HEDGEYE FINANCIALS RISK TRACKER

Key Takeaways:

- The Ted Spread held flat d/d at 15 bps as of 02/16, also holding flat from four weeks ago

- The Euribor-OIS Spread remains in negative territory since the beginning of August 20'

- The CDOR-OIS Spread held flat d/d at 23 bps as of 02/16, down -4 bps (-16%) from four weeks ago

- The 2-10 Spread increased +8 bp d/d to 118 bps as of 02/16, up +22 bps (+23%) from four weeks ago

- High Yield spreads decreased -8 bps d/d to 3.15% as of 02/16, down -33 bps (-10%) from four weeks ago

Much of our risk tracker focuses on overnight interbank lending spreads. The reason for this is those spreads reflect systemic risk perceptions and reality. When those spreads are low (tight) the perceived risk is low and when they're high (wide) risk is rising. The normal state for these spreads is to be low (tight) and that's the case >99% of the time. Aside from the interbank market, we also consider stress gauges in the high yield and leveraged loan markets, important gauges of risk in the corporate credit market. Individual name CDS signals issuer-specific risk and can also be viewed in the context of the broader group, i.e. U.S. Financial issuers. Sovereign CDS reflects the perceived default risk of the respective countries.

Since the beginning of the pandemic, central banks have flooded the system with liquidity and have, so far, successfully put a dampener on most conventional risk gauges such as previously ballooning interbank credit spreads and global financial CDS spreads, while also propping up the leveraged loan market and applying downward pressure to high yield credit spreads.

Summary

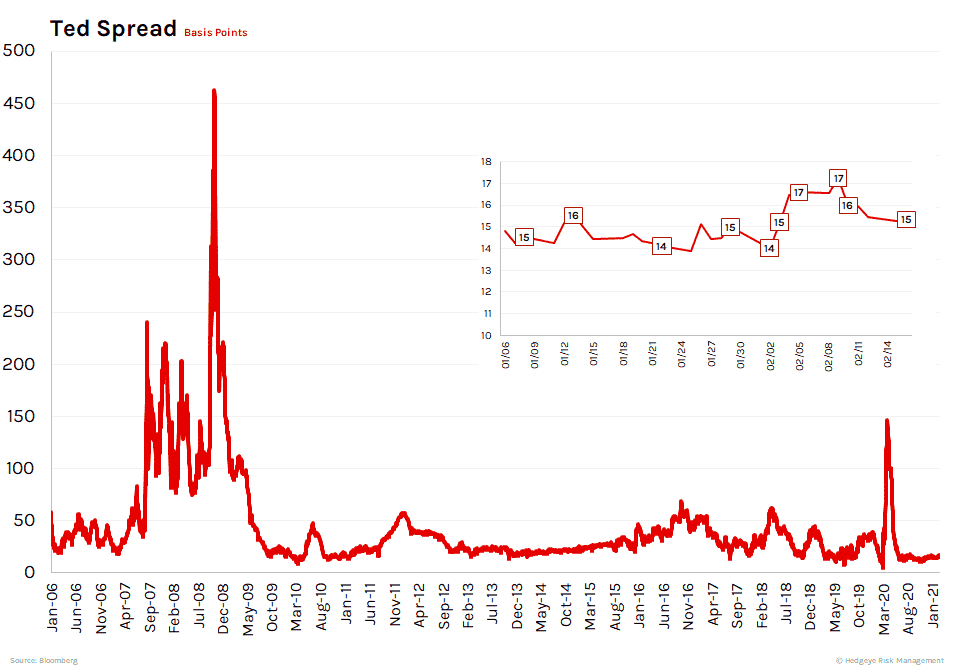

1. TED Spread – The TED spread held flat d/d at 15 bps as of 02/16, flat from four weeks ago as well.

2. Euribor-OIS Spread – The Euribor-OIS spread held flat d/d at -6 bps as of 02/16, flat from four weeks ago as well.

The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

3. Chinese Interbank Rate (Shifon Index) – The Chinese Interbank Rate held flat d/d at 1.93% bps as of 02/16, -31 bps (-13.9%) lower from four weeks ago.

The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

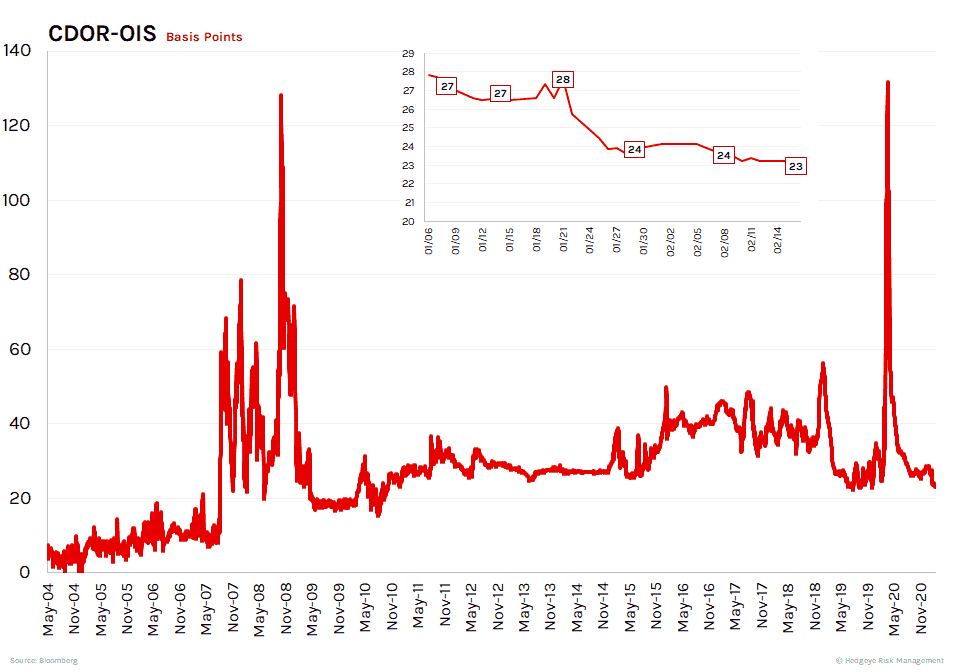

4. CDOR-OIS Spread – The CDOR-OIS spread held flat d/d at 23 bps as of 02/16, -4 bps (-16.2%) lower from four weeks ago.

The CDOR-OIS spread is the Canadian equivalent of the Euribor-OIS spread. It is the difference between the Canadian interbank lending rate and overnight indexed swaps, and it measures bank counterparty risk in Canada.

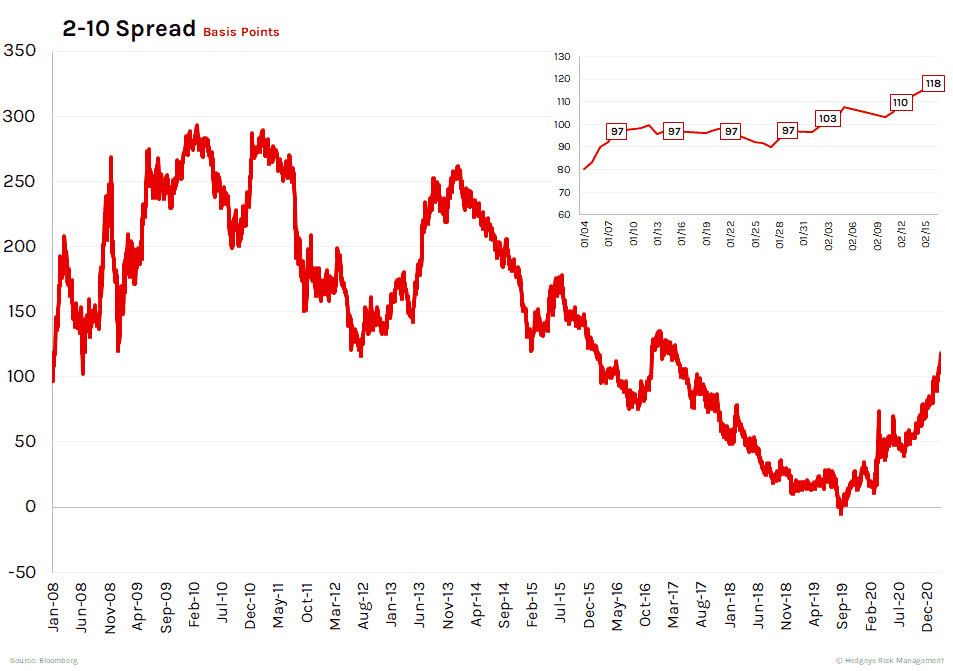

5. 2-10 Spread – The 2-10 spread moved +8 bps (+7.5%) d/d to 118 bps as of 02/16, +22 bps (+22.8%) higher from four weeks ago.

We track the 2-10 spread as an indicator of bank margin pressure.

6. High Yield (OAS) – Option-adjusted High-Yield spreads moved -8 bps (-2.5%) d/d to 3.15% as of 02/16, -33 bps (-9.5%) lower from four weeks ago.

7. Leveraged Loan Index – The Leveraged Loan Index moved +2 pts (+0.0%) d/d to 2370 pts as of 02/16, flat from four weeks ago.

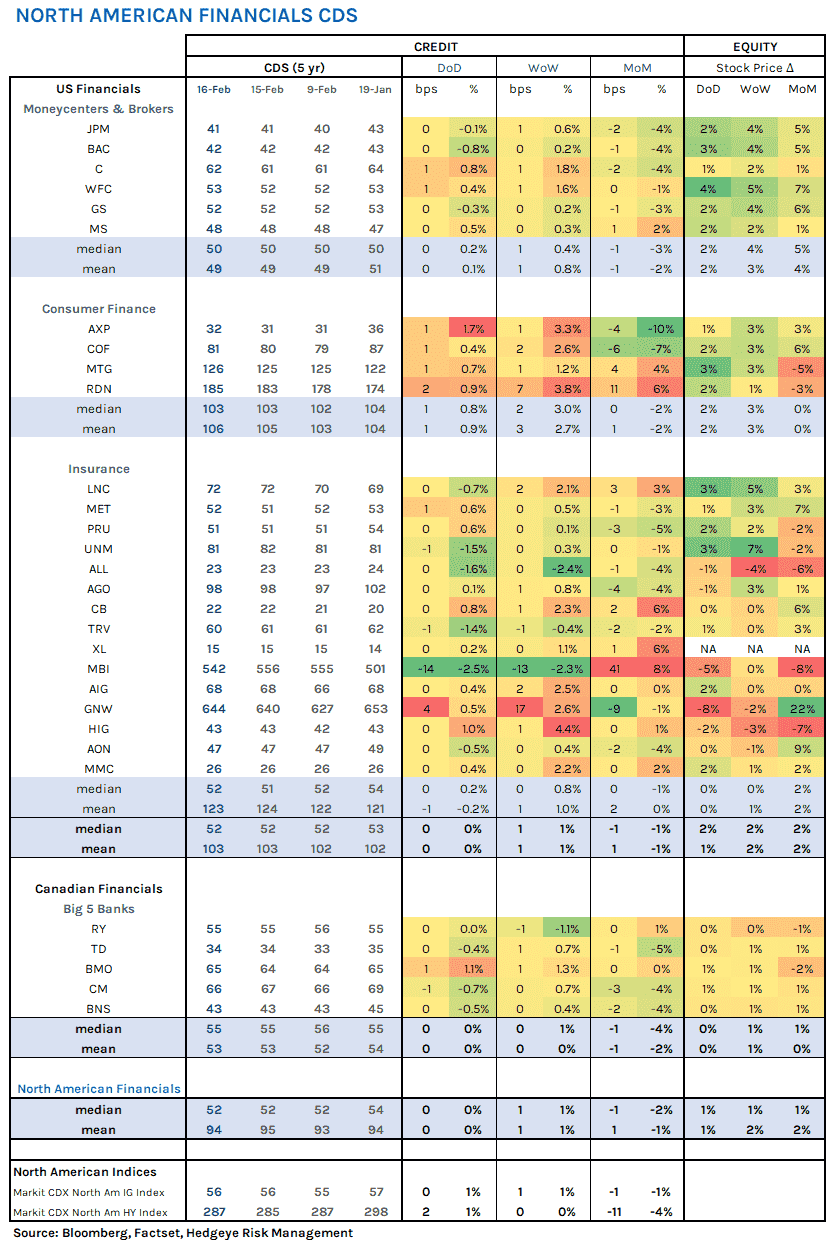

8. North American Financial CDS – The median North American financials swap held flat d/d at 52 bps as of 02/16, -2 bps (-2.9%) lower from four weeks ago.

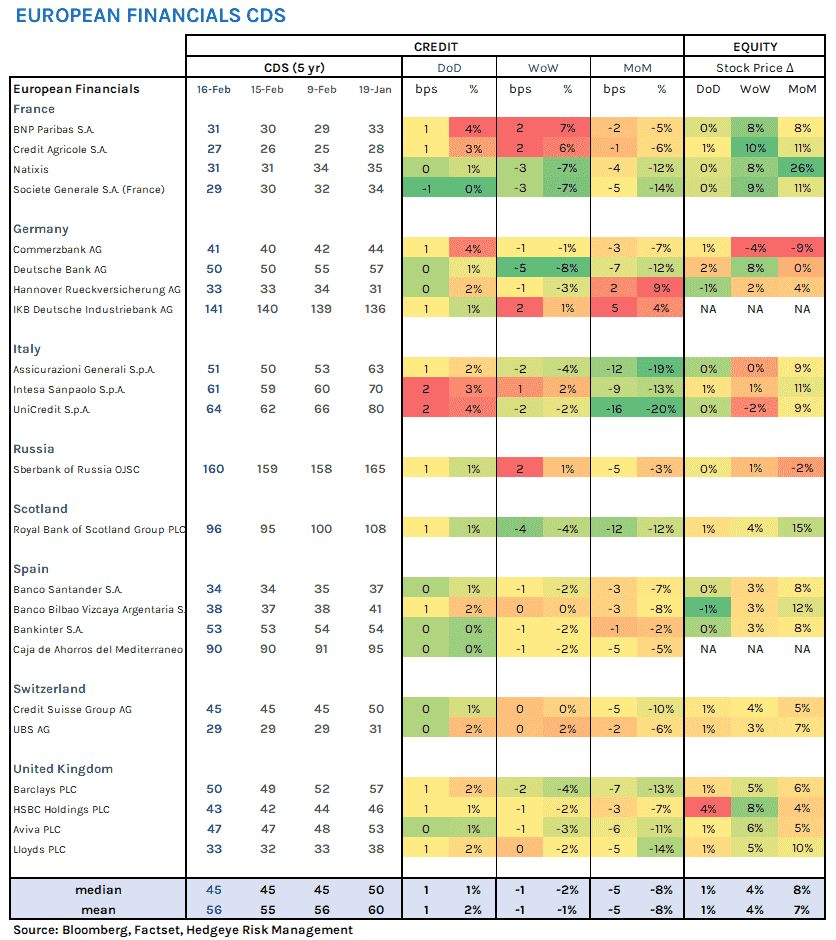

9. European Financial CDS – The median European financials swap held flat d/d at 45 bps as of 02/16, -5 bps (-9.5%) lower from four weeks ago.

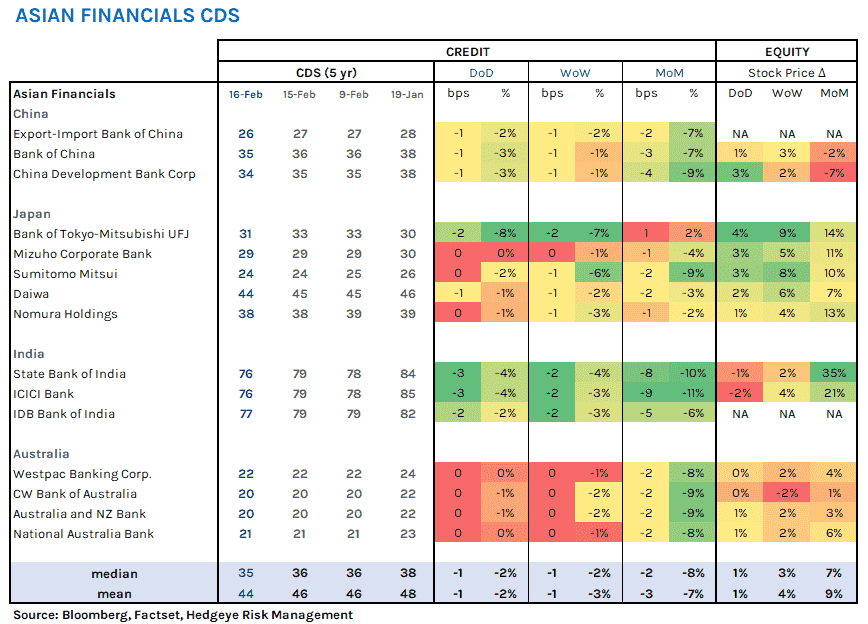

10. Asian Financial CDS – The median Asian financials swap moved -1 bps (-3.2%) d/d to 35 bps as of 02/16, -3 bps (-6.8%) lower from four weeks ago.

11. Sovereign CDS – Australian swaps increased most d/d, moving 0 bps (+1.8%) to 14 bps as of 02/16. Japanese swaps increased most m/m, moving 0 bps (+1.1%) to 15 bps as of 02/16.

12. Emerging Market Sovereign CDS – Russian swaps increased most d/d, moving +2 bps (+2.6%) to 85 bps as of 02/16. Chinese swaps improved least m/m, moving -2 bps (-6.4%) to 29 bps as of 02/16.