This Nike print lived up to the hype. Lots for both sides to chew on. We expected that. But the only way the short side could really work – i.e. one of those horrific -10% days with lousy follow through in subsequent weeks – is if there was a big fundamental erosion in the business and Nike backed off its model. Yes, North America Futures were lousy (+1%) but the global numbers looked healthy, inventories are improving on the margin, underlying gross margins looked good, e-commerce growth (+49%) was off the chart, and the organic EPS number beat by a nickel, or 9%. The punchline is that the company is on track to delivering on ‘the hockey stick’ earnings ramp for FY17 (May), and we’re taking our numbers up by more than the 1Q beat to a level that will likely be about 5% above consensus (we’re 30% above by 2019). Maybe the hedge fund community will bat this name around a bit after the noise surrounding this print. But will a long-only PM punt this name because of what Nike just printed? No. Relative to what was rumored before the call, this print was more than good enough for most people to stay put. It certainly is for us.

All of that said, we give the management team a D minus for this call.

- Parker and Edwards both get an A (rare that we give Trevor Edwards an A). They were poised, thoughtful extremely confident. If there are problems out there, someone forgot to give Nike the memo. Historically, it’s not a profitable move to bet against Nike’s confidence (unless it comes with a strong dose of cocky – and we definitely did not get that sense). Mark has never seen a category or market that he has not been ‘extremely excited’ about growing. In fairness…he’s usually right. Too bad he’s only got about a year left in his seat until he hands the reigns over to Trevor.

- On the flip side, I give Andy Campion a strong F on this one, and the whole investor communication effort something between a C and a D. How they managed guidance was fine. But reclassifying what we think is 100bps of costs from SG&A into COGS AND changing up the process for communicating futures to the Street AGAIN in a quarter where there are so many questions around the sustainability of growth is simply not cool. Nor is the lack of transparency and quantification of these items.

To be clear, this was a lay-up quarter for new CFO Andy Campion to earn his stripes. My view on almost any job is, you rarely want to step into a role where the person before you was the best of the best. That’s what Campion did. Don Blair was about as good as they come. A great CFO is not revealed when business is going great, but rather when a model is going through a state of transition as Nike is today. Blair would have breezed through this with no problem. Campion did poorly. He actually scored the equivalent of an ‘own goal’ in soccer/football (whatever).

The CFO’s miss definitely won’t help the stock tomorrow, but it has zero impact on our call on this name.

- TAIL: GM% headed above 50% as mix moves higher and Nike consolidated 3-4x gross profit dollars without the need to gain share as e-comm goes from 6% of sales to 20% over 3-4 years. Ultimately you’ve got near $5 in EPS. A 20x multiple (lower than what you have today) is a $100 stock.

- TREND: EPS accelerates meaningfully as revenue growth accelerates globally, gross margins trend higher due to DTC and less inventory bloat vs last year and SG&A growth takes a dive due to the Olympic spending hangover. All in that takes EBIT growth in Q1-Q4 from -11% to 9%, 24% and 37% respectively.

- TRADE: The near term factors like Adidas/UA share gain, Olympic Trade, Channel Conflict (this is real), Inventory Issues might matter in part to the US market, but the reality is that Nike is a global company. Maybe we see multiple pressure as US investors are pretty myopic on this issue. But Nike guided to mid-single digit US revenue growth – which is probably conservative, and is more than enough for Nike to achieve/beat its guided financial model.

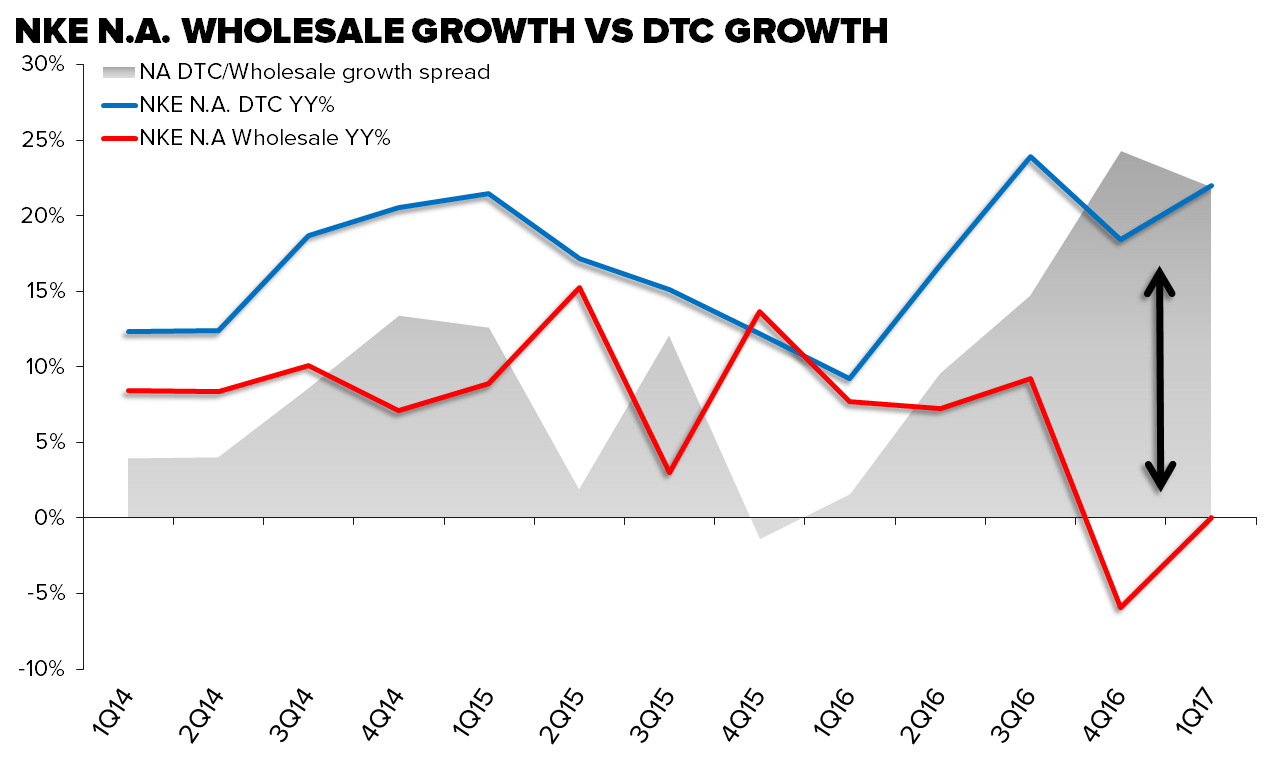

The bears will dwell on the meager 1% growth in futures in North America. Thats what we call ‘pretty much negative’ in Nike-talk. It completely validates the concern about Nike losing share in the US market – sort of. The space is about +4% -- Nike grew 50bps in the quarter (share gain), but then put up an order book of only +1% -- implying share loss. We’d also note that e-comm (which is now included in futures) was up 49% in the quarter, good for 3% of revenue growth and helped fuel 22% DTC growth -- implying that Nike’s wholesale orders were up just 3.4%. This is at the same time that inventories in the channel – FL and FINL are getting better on the margin. This is opposite to what we’ve seen historically -- as the model has been ‘as goes Nike, so goes FL.’ That’s no longer the case. Nike is likely to go down to 70% inside of FL (from 72% last year) and should be closer to 60% within 18 months. This is by design. The datapoints that float around the hedge fund community (Nike losing share) will be extrapolated to the global business – which is simply inaccurate. That’s our biggest concern here – the multiple and certainly NOT the earnings.

Here are some other trends we’d point out as notable.

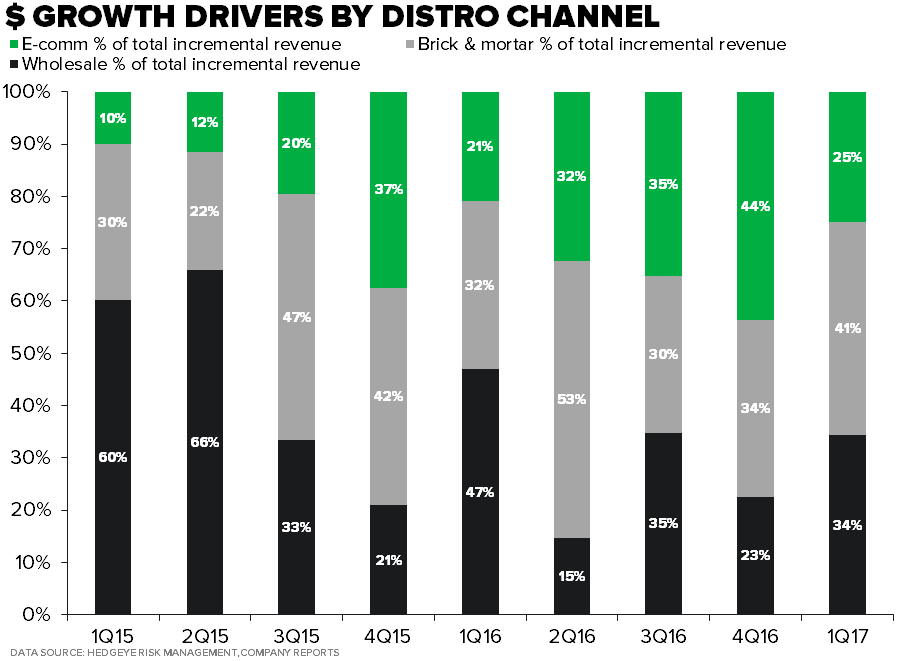

1) Nike’s DTC business grew at a staggering 49% this quarter. By our math, US DTC was up over 20% in the quarter, while wholesale was flat. Though the numbers don’t outwardly show it, that’s a sequential improvement from 4Q when wholesale in the US was down 6%. We’re hard pressed to think that wholesale will consistently grow better than 3% in the US ever again. On a trendline basis (out to the TAIL duration) we think that 90% of incremental profit for Nike in the US will come from its DTC/online business.

Looked at a slightly different way, we’re down to about 1/3 of incremental revenue growth coming from wholesale – 50% lower than just two years ago. The spread is much greater on the gross profit line as DTC carries 3-4x gross profit dollars as wholesale.

2) Futures/Revenue Delta: There’s been a 5-7 point delta between Futures growth and reported revenue growth in the past four quarters. Therefore the trends we saw today are actually not unusual. Campion’s assertion that we should see revenue growth ahead of futures growth throughout 2017 is actually plausible.

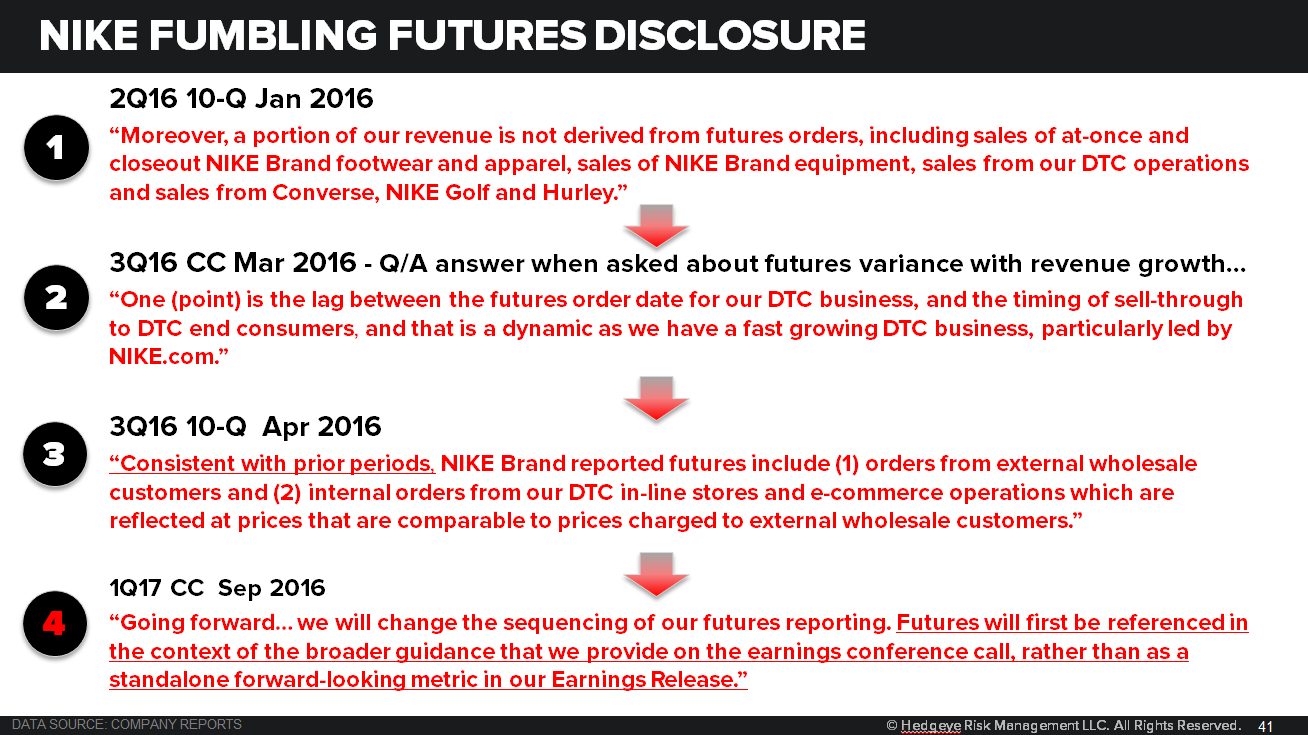

3) But…can anyone explain the moving target that is Nike Futures? The company has tweaked/changed its disclosure in each of the past four quarters. Yeah…we get it that futures are largely unaudited, and should not matter as much as the wholesale model shrinks relative to the whole. But for a World Class company like Nike, we expect World Class disclosure. #fail.

4) GM/Inv/Futures: If there is only one chart we need to see for Nike – after e-comm growth – it is the triangulation in futures, inventory and gross margins. The two former almost always are a great predictor for the latter. This quarter, however there was a big disconnect – not the least of which was the (uncharacteristically opaque) reclass of expenses from SG&A to COGS. By our math, this dinged GM% by about 100bp. On an adjusted basis, we should see GM accelerate throughout this year as mix shifts higher and DTC is increasingly consolidated.

5) SIGMA Improved. This might look gnarly – and it does. But the fact is that inventories corrected – slightly – on the margin. And everything matters on the margin. The next move is likely to be in the upper left, which is multiple-positive.

Below is our previous note from 9/26/16:

NKE | Key Issues – And What To Expect

Not a slam dunk qtr. But the bear case is just too easy to build – so everybody’s doing it. It’s lacking context and in some cases, truth.

Let’s be clear about one thing…we’re definitely nervous about Nike’s 1Q print. This has not been a battleground stock for the better part of three years – but today there is no question that it is. In fact, a short-seller’s narrative around this name has never been easier to construct – at least in this economic (and sneaker) cycle. It sounds something like this…

- Sharply decelerating futures trends in last quarter,

- Simply massive acceleration in the Adidas brand,

- Continued growth out of UnderArmour,

- Shrinking US distribution,

- NKE already tapped out inside FL (72% of FL sales bear a Swoosh),

- The Olympic Hangover,

- Golf Implosion,

- Peaky valuation, and

- Hockey Stick Guidance

But the simple fact, and it is a fact, that it is so easy to construct this bear case leaves us more inclined to think that it has become the consensus. In addition, while many of these ‘fear factors’ are concerning, we think that easily half of them are being blown out of proportion and lacks the context for a behemoth that manufactures 285mm pairs of kicks a year.

Our sense is that given the pessimism around the name, if you think Nike can

a) Nike can hit the quarter (TRADE), and

b) Deliver on the hockey stick (TREND),

And you think that these TAIL factors will come to fruition…

a) Gross margins headed above 50%, and

b) $5.00+ in EPS power just below the surface with sharply accelerating returns and the management team to unleash it.

…then this is probably a stock you want to own.

We vet through all these factors in our 45-page Black Book which we presented earlier today. Here’s the video link.

Replay: Nike: Key Issues Ahead of the Print

We hand-picked some of the slides that garnered the most interest. Here goes…

1. EPS Trajectory. We believe in the ’hockey stock’ EPS trajectory for FY17 (May). Post-Olympic product flow is strong and DTC accelerates on top of lower SG&A. Then e-comm drives the top line and gross margin line for the duration of the model. All in, we get near $5 in EPS in 3-4 years, which is 30% above the consensus.

2. Adidas’ Momentum matters. The ‘Yeezy’ really does not. We only bring up the Kanye shoe bc we are asked about it so often. To put it into context, Jordan is a $6.3bn brand at retail. If Yeezy triples this year, it will be $300mm. At best we’re talking 70bps in share. Not relevant.

3. What does matter is the core Adidas share gain, which is very real. But let’s remember where Adidas is coming from – hint: a very low base. Before the AdiBok merger in 2005, the two brands had 16pts combined share. By 2014 the company evaporated its share to 6%. Reebok has all but gone away. Can Adidas recapture 2-3 points? Yes. Does that mean it comes out of Nike’s coffers? No. Yes this is a zero sum game. But NKE, Adi and UA can all gain a point of share for the forseeable future without stepping on each other’s kicks.

4. Content Winning, Distribution Losing. Adidas’ web traffic is en fuego. But Nike isn’t doing too bad either. We’re seeing steady losses, actually, in traditional Brick&Mortar channels. Beware Foot Locker. This trend will be more sever and will last longer than most people think.

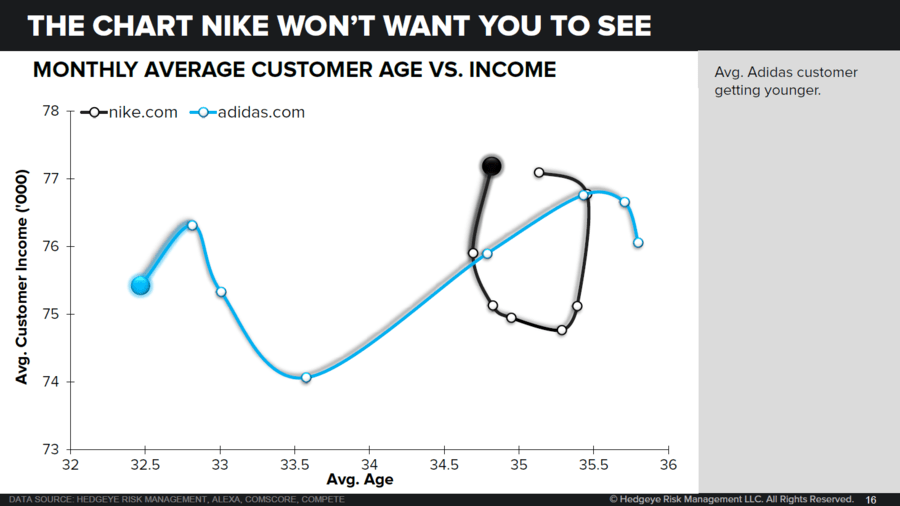

5. Nike hates this. This chart shows age vs income for the Nike and Adidas demo. Simply put, the Nike consumer is getting older, while the Adidas consumer is younger and richer. This fuels that ‘your father’s Buick’ argument for Nike. That said, if there is any one factor Nike is aware of internally, it is this one. The risk is not that the brand gets too old, it is how much money Nike will spend (and it will spend what is necessary) to keep it youthful and awesome.

6. e-comm targets are beatable. We get a lot of pushback on Nike’s $7bn e-comm target by ’19. We think the internal target is $8-9bn. Our estimate is $9-11bn. Two points here. A) Nike hitting its goal only represents a 30% CAGR. There’s nothing outrageous about this – 20% in US and 40-50% int’l. If we see 40% we get to $8.5bn, and 50% = $12.5bn. Nike will hit these not just through product innovation, but by manufacturing/distribution innovation – that’s the factor people are not banking on. This is already in the pipe for Nike – they’re simply not talking about it.

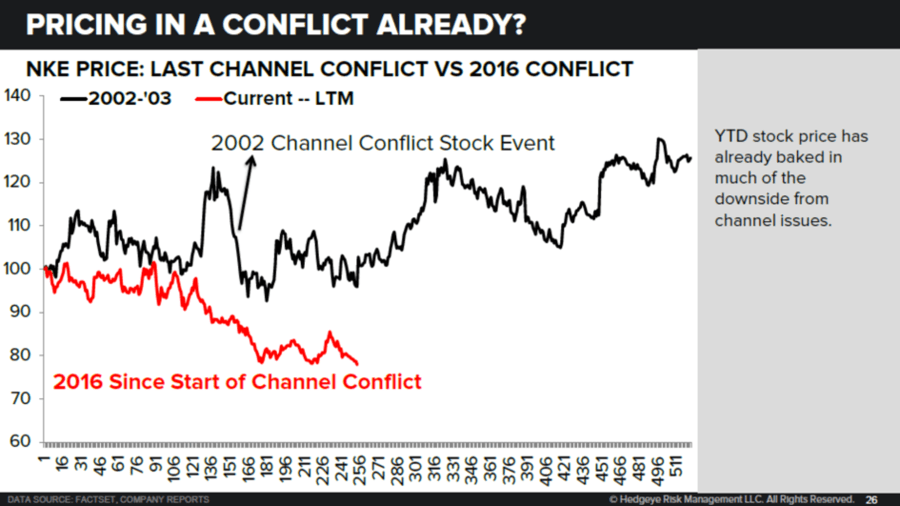

7. With great e-comm growth comes great channel conflict. Remember in 2002/3 when Nike and Foot Locker tried to figure out whether content or distribution was more relevant. Hint, Nike won. But during that time, Nike’s stock was off by 22% relative to the market. We’re about 9 months into the start of a channel conflict 14 years later, and year-to-date NKE is down – yes you guessed it – 22% relative to the market. We’re not calling this a template, but are simply making the point that there’s a lot of bad news in this stock.

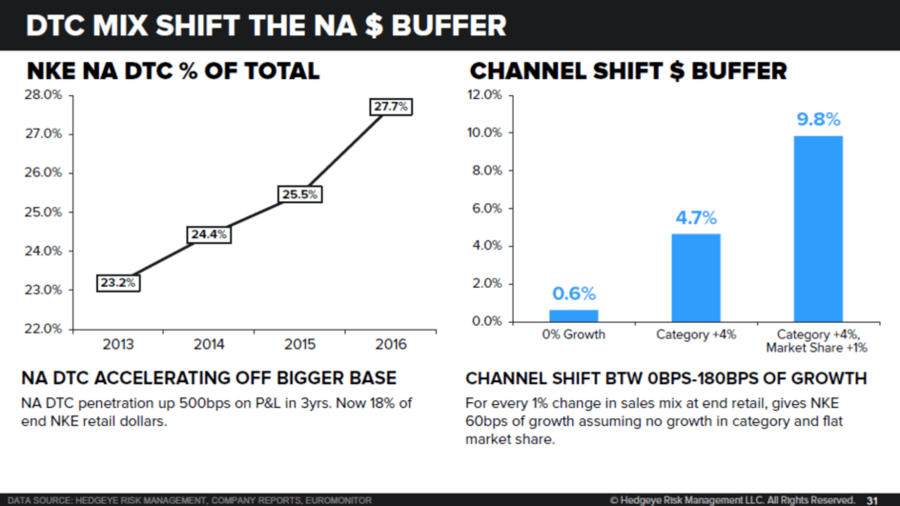

8. THE KEY SLIDE NO ONE TALKS ABOUT. With Nike consolidating incremental units in a vertical model (i.e. in its own DTC business) there is a natural revenue lift that’s underappreciated. In other words, with no change in end market share, Nike goes from consolidating $65 for a $140 shoe that sells through wholesale to booking all of a $175 shoe online. This is about a 2,000bp margin lift, and more importantly accounts for 3-4x the gross profit dollars. Looking at the right half of the slide below…

a. Assuming the market does NOT grow one bit, and Nike’s share is unchanged, we’ll see 60bps revenue growth simply from the consolidated accounting. In this scenario, our numbers are too high. Unlikely.

b. In the second scenario, where the market grows at 4% and Nike share change is ZERO, we’ll see 4.7% growth in consolidated revenue – halfway to the company’s hsd goal. This should be easy.

c. With the market growing by 4% and Nike gaining 1 point of share, we get to 9.8% top line growth – which more than puts Nike over its long term goal. In other words, hitting its long term goals are easier than Nike has experienced in recent years.

9. Inventories are still questionable. Nike’s SIGMA is in a rough place – Quad 3 is never good. We’re also seeing unusual discounting in Nike’s in-line stores, where the company is going in with heavy price points, but is offering up 20% off cards when you walk in the store. Our sense is that the SIGMA will turn up this quarter – something that has to happen for the stock to work.

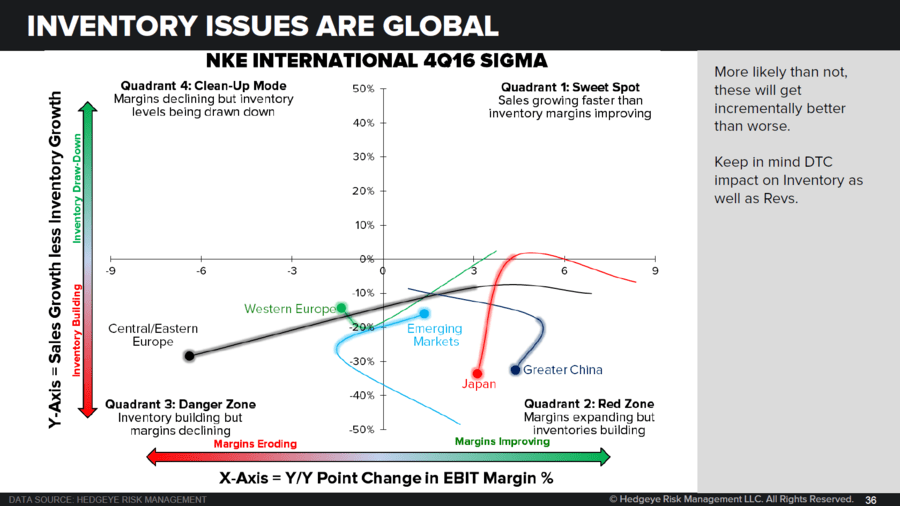

10. GLOBAL SIGMAs. This is more of an fyi…but we have enough disclosure to calculate SIGMAs in every region. They all pretty much look bad – except Emerging Markets. The US, at a minimum, should improve, as noted above.

11. Another Key Chart. If I could look at only chart every quarter, this would be it. It triangulates futures, inventories and gross margins. When Futures are trending up, inventories are trending down, it invariably leads to extremely bullish gross margins. Today, we have decelerating futures and bloated inventories. That should be bad. BUT, we think we’ll see solid GM trends out of Nike – which is not to say that core margins are good. But simply that the e-comm benefit is more than offsetting weakness in merchandise margins. That’s a secular trend, and a bullish on eat that. Even more so when inventories are completely clean.

12. Olympic Trade Does Not Exist. People always talk about the ‘Olympic Trade’ with the understanding that you should own Nike 3-6 months into the Olympics. Never has this proven to be the case. Back to 1992 when we separated the Summer and Winter games into 2-year increments, there has been only one out of seven Olympic Games where this trade worked. In fact, the stock more often works after the games. Why? The channel gets cleaned out just ahead of the Games, revenue is strong due to the product launched around the event, and lastly, SG&A rolls over resulting in a fat hockey stick in EPS (usually more than people think).

13. Futures Transparency. Here’s a nit pick – but a valid one at that. Nike has slowly evolved its verbiage around Futures over the past year. First it said, as it always did, that Futures excluded DTC. Then in 3Q16 Nike started getting vague about how futures are accounted. Then in 4Q Nike said “consistent with prior periods, futures include [DTC including e-comm]. This actually matches up with economic reality, so we can’t really fault Nike. But this is hardy the stand-up disclosure we’ve grown to expect from this company.