As we charge out of summer into fall, and into the ECB’s next interest rate meeting (on Thursday, September 8th), below we revisit our Eurozone regional economic and political outlooks within the context of our Q3 2016 Macro Theme of #EuropeImploding.

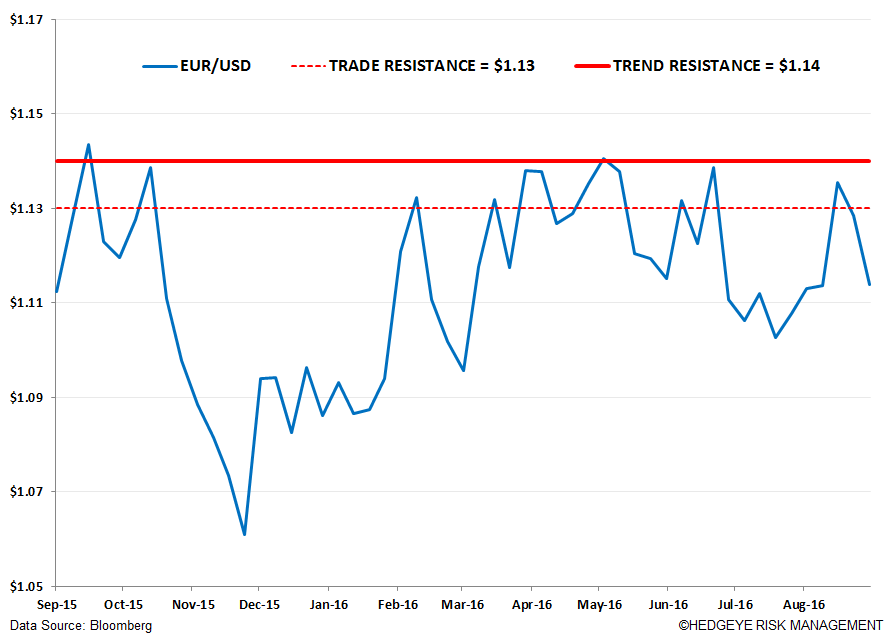

The quant continues to signal that the EUR/USD is broken across its intermediate term TREND duration and immediate term TRADE duration with a current trading risk range of $1.11 – $1.13.

Growth Outlook: Slowing Persists

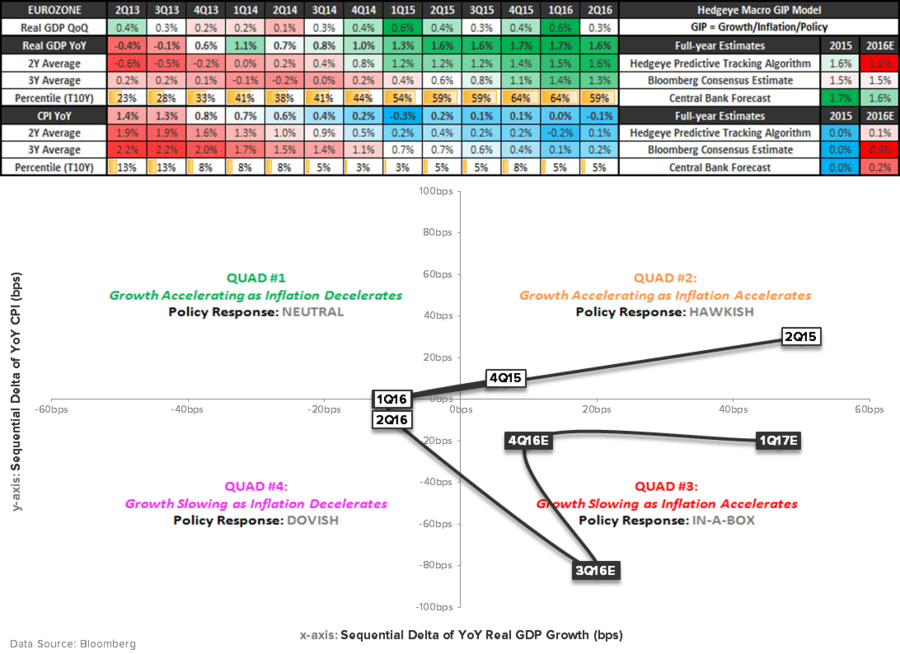

The Eurozone as a whole (alongside most individual countries that make up the 18 member bloc) is stuck in Quad 3 of our proprietary GIP (growth, inflation, policy) model - growth slowing as inflation accelerates - for the remainder of 2H 2016 and into early 2017.

Reported Q2 European GDP from Eurostat (released back on August 12th) confirmed what we had long been beating the boards about: #EuropeSlowing (a Q3 2015 Macro Theme!).

Eurozone Q2 GDP fell to 0.3% Q/Q vs 0.6% in the prior quarter and fell to 1.6% Y/Y vs 1.7% in the prior quarter.

While the market was shocked by the lower Q2 print, we weren’t, and as you can see from the table below, Hedgeye’s 2016 FY estimate for Eurozone GDP (+1.2%) is notably lower than Bloomberg Consensus (+1.5%) and Central Bank (+1.6%) estimates. So there’s more room for downward surprises from here!

In addition, numerous international forecasting agencies have lowered country level growth and output estimates across Eurozone countries over recent weeks:

- The Bundesbank in its biannual economic outlook cut Germany’s growth forecast for 2016 to 1.7% (from 1.8%) and for 2017 to 1.4% (from 1.7%).

- The German Institute for Economic Research (DIW) showed German GDP forecast to fall by 0.4% in the first eight months post-Brexit, and said Eurozone GDP could fall by 0.2%.

- Germany's BGA Trade Association cut its 2016 forecast for German export growth to between 1.8% and 2.0% this year (vs its previous forecast of 4.5% in April) due to risks from Brexit and increasing global uncertainty.

- Bank of France reiterated its 1.4% growth target for 2016 (Hedgeye is at 1.0%) and cut the 2017 estimate by 10bps to 1.5%.

- Fitch Ratings agency downwardly revised Italy’s growth estimate to 0.8% vs 1.0% in 2016 and to 1.0% in 2017 and 2018 (down from 1.3% and 1.1%, respectively).

Olympic-Style Data Dive:

We’ll let the data speak for itself in the charts below. In any case, it’s been crystal clear to market participants that Eurozone data is broadly slowing, not improving, on the margin. Again, the QE central-banker wand is not working!

This week, the release of Inflation (CPI) for August printed +0.2% Y/Y, unchanged from the prior month and below the 0.30% forecast. Is CPI anywhere near the ECB’s medium term 2.0% target? Nope!

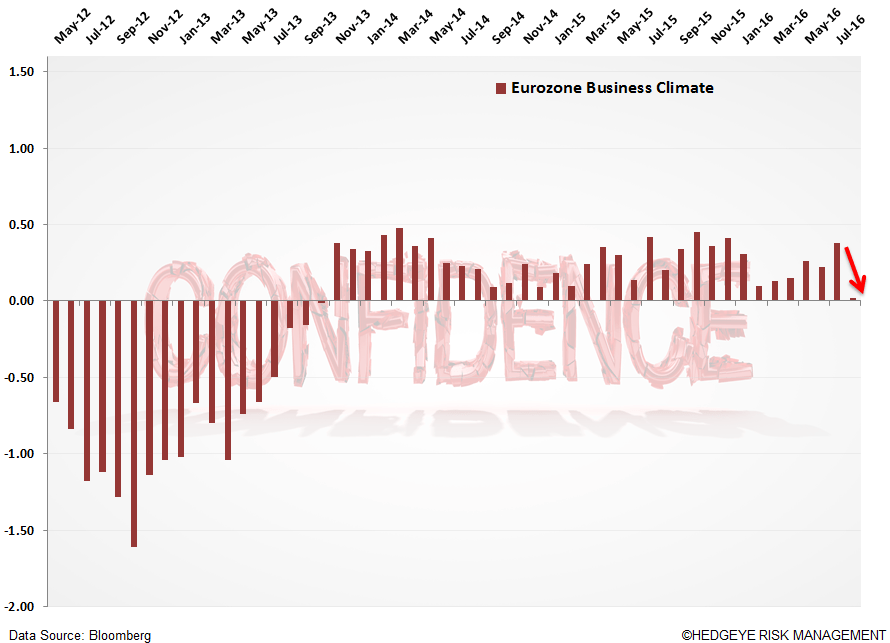

Eurozone Confidence figures for the month of August fell across four categories (Economic, Business, Industrial, and Services), while Consumer confidence remained unchanged on the month.

Manufacturing PMI data for August was also anemic, with a M/M decline for the Eurozone in aggregate, with most countries showing monthly declines or levels around/below the 50 line indicating contraction.

Finally, Germany’s IFO Business Sentiment Survey did a swan dive in the August print, with Expectations (6 months out) falling for a second straight month.

ECB Policy: Super Mario to the Rescue?

Assessment: Draghi has run out of bullets in an attempt to manage growth and inflation expectations

If we had a dollar for every time we mentioned that neither Mario Draghi, nor any other central banker for the matter, can will growth and inflation higher through quantitative easing, well, frankly, we’d be rich!

This time around is therefore no different – the ECB’s newest “tool”, to buy selective corporate debt alongside its sovereign Eurozone debt buying, will remain a failed policy as a “transmission mechanisms” to the real economy.

As we’ve noted in other works, the Fed’s Janet Yellen has now made 5 policy pivots (from Dovish to Hawkish) in the last seven months. Her credibility, along with Draghi’s and Kuroda’s, is one and the same: lost!

Most recently at Jackson Hole the ECB's Benoit Coeure said that “if other actors do not take the necessary action then it [the ECB] may need to dive deeper into its operational framework and strategy.” #HelicopterMoney?

We expect that September’s meeting next Thursday will yield no new “programs” or “tools”, yet we expect any language attached to an economic and inflationary outlook to be marginally more bearish to reflect updated economic data releases.

Political Risk Rising!

Spain - the poster child for political risk, as acting PM Mario Rajoy is into his 9th month without a government. The latest update is Rajoy lost a confidence vote yesterday 180 votes to 170.

Is there a path for a government going forward? We expect that Rajoy is unlikely to form a majority government (176 votes needed of 350-seat parliament), given his inability to attain enough votes through a coalition with the liberal Ciudadanos party, as a strong block opposition in the Socialists (PSOE) and anti-establishment group Podemos seek to block his candidacy. We suspect we’ll be looking at a third election before year’s end.

Italy - Calling a Referendum David Cameron Style? How about this scenario… by the end of the year Italy’s PM Matteo Renzi is replaced?

It could happen. In early August Italy’s high court approved a constitutional referendum set out by PM Renzi to do away with a parliamentary system in which the upper and lower houses have equal powers, effectively abolishing the Senate as an elected chamber and sharply reducing its ability to veto legislation.

While this referendum’s original intention had nothing to do with Italy leaving the Eurozone or not, media messaging was twisted, and whether a mistake or not, Renzi personalize the result of the referendum, saying that he would resign if the vote was not a ‘yes’. An ode to David Cameron!

Over recent weeks Renzi retracted his statement, saying: “This is not my referendum…I’ve made a mistake in personalizing it too much. But now we simply need to tell the truth about the substance of the reform…The question is not, ‘Do you think Renzi is a nice guy?’ It is, ‘Do you want to cut down the number of parliamentarians and scrap perfect bicameralism?’ If [the reform] passes, it will cut the cost of politics by €500m a year.”

Recent polls show "Yes" and "No" camps almost neck-and-neck, and many voters are still undecided ahead of the referendum, which in theory could take place on any Sunday between October 2 – December 11. Recent whispers suggest a November 27th date.

However, the referendum does share parallels with the UK Brexit referendum because like Cameron, Renzi has linked the referendum vote with his candidacy. Having open up this box, he’s squarely allowed Italians to vote him out of office, regardless of their opinion on the referendum. Not only has Renzi’s popularity been fading in recent months to anti-Eurozone/European parties, including the euroskeptic Five-Star Movement and Northern League, the referendum gives this opposition new marketing fodder to vote him off the island.