We remain short headed into tomorrow’s print. No, this isn’t a call on the quarter, as expectations look to be in check at a -2% comp flowing through to -4% earnings growth – but a broader statement on where we think we are in the progression of the KSS short thesis. If the company throws the bulls a bone – as it does from time to time – then we’d get heavier on it. This is as much of a ‘core short’ as we can find in this market.

The progression of the thesis is in three stages, as follows…

1) Stage 1: Weak sales results as a result of the fact that KSS sells less and less of what consumers want to buy. Sounds overly simple – but it’s reality. That flows through to the gross margin line as online sales cannibalize brick and mortar, and come at a gross margin 1000bps below the company average. True SG&A growth becomes apparent as credit income stops going up as newly emphasized non-credit/loyalty shoppers become a bigger mix of the pie due to launch of Yes2You rewards program. This is where we are today and gets us to an earnings number in the mid-$3s. At a HSD multiple, that’s a low-30’s stock which = 20% downside from current levels.

2) Stage 2: Here’s where credit income (currently about 1/3rd of EBIT and 60%+ of sales) erodes WITHOUT a rollover in the broader credit cycle. The company’s much-touted (but ultimately fatally flawed) Yes2You rewards plan cannibalizes credit income as shoppers can move to a loyalty program that offers similar rewards to the branded credit card but gives the consumers the opportunity to get 2x the points. Once at KSS and once on a National Credit card. That takes SG&A growth, which has been artificially suppressed as credit sales grew from 50% to 60%+ of total sales over a 5 year time period, from a run rate of 1% to 3%-4%. For a company that comps 1% in a good quarter, this is incredibly meaningful.

3) Stage 3: This is the doomsday scenario, and within the realm of possibility as the credit cycle rolls. On top of the self-inflicted pain we see in Stage 2, we see consumer spending dry up (sales weaken – down 5-10%), gross profit margins are down 2-3 points due to excess inventory, SG&A grows in the high single digits due to credit income (which is booked as an offset to SG&A) eroding, and EPS falls to $2.00-$2.50. Look at any data stream on the credit cycle and you will see that delinquencies and charge-offs are creeping off post-recession lows with some bearish commentary mixed in from the likes of Synchrony Financial and Capital One. Translate that to KSS, and it means that the credit portfolio is currently at its most profitable rate. Because the company shares in the risk/reward with its partner COF, any weakening in the consumer credit cycle exacerbates the problems brought on by Yes2You cannibalization and puts 30% of EBIT and half of the current FCF at risk. The result, cash flow dries up and by our math, cuts its dividend within 12-months.

Other Key Considerations Into The Quarter:

Comp Compares – Remain Tough

Despite the low expectations embedded in this name today, we think it’s important to point out that compares on the top line don’t get any easier as we pass through the balance of the year, which happens to be the tail end of the longest positive comp trend (5 quarters) that the company has posted since 2010-11. That was facilitated by an upward lift from traffic – somewhat due to the Y2Y introduction and some pricing power due to the shift away from private label towards national brands. The latter will still be a benefit, but we expect the traffic element to still be under considerable pressure from here. That’s important for a company like KSS who needs a 2% comp to leverage expenses across an already lean organization that is facing ‘significant wage pressure’ thanks to WMT.

Government Data Not Getting Better

We won’t complete the 2Q trifecta, as the government reports July retail sales the day after KSS reports 2Q numbers – but based on the government data, department store trends didn’t pick up in the first two months of the quarter down 5.8% in May and -3.7% in June. Softer than we saw in total for 1Q16, and about on par with 1Q on a 2yr run rate in the ballpark of -3% to -4%. Looking at the most recent data points, we saw every retailer who still reports monthly sales numbers post negative July comps (with the exception of LB). That was capped off by a -4% GPS print on Monday. Anyone looking for a hint of relief for the category isn’t going to find it here.

UA Not Protecting This House

Perhaps the biggest selling point the company will talk to on tomorrow’s call is the introduction of UA in Spring 2017. It’s certainly a win for the company in that it gives KSS some good marketing material when talking with investors, but the way we are doing the math it’s worth no more than a 0.5% lift to comp. Here’s a quick summary on the math – the UA opportunity in year one is $142mm, that will be displacing about $53mm in product which we assume has a productivity rate 75% of the company average, for a net total of $89mm benefit to KSS. For full details, see our note: UA/KSS | The Best + The Worst = Not The Best.

No Turn Down In Credit… Yet

Perhaps the most vexing component of our KSS short call is the relative strength of the company’s credit portfolio growth since the introduction of the Y2Y rewards program at the tail end of 2014. Our logic after the introduction of the Y2Y, which essentially decoupled the rewards program from the credit card (in the past you needed a KSS charge card to get the promotional benefits), was that we’d at the very least see the growth of the portfolio stop, with a very high likelihood that the Y2Y would cannibalize the credit card business because consumers could use any form of currency to capitalize on the myriad number of Rewards promotional events.

To date, the credit income has continued to chug along, and has provided an offset to the underlying SG&A growth between 0-1% every quarter since the Y2Y was introduced in 3Q14. Though we have seen a few cracks in the metrics and the rate at which the portfolio has grown as a percentage of sales has tailed off, credit continues to be a net benefit to the company when recognized as an offset to SG&A. Each of the bars below represents the spread between SG&A ex. credit (i.e. if credit was flat YY) and the reported SG&A growth rate – any reading on the positive side = a net credit benefit. Put another way, SG&A grew -0.8% in 1Q16. Ex the $8mm credit benefit, SG&A dollars would have been flat YY.

We still think that the credit portfolio is stretched, as a) the company has tapped 75% of its total addressable market, and b) the company skimmed the bottom of the credit worthiness barrel when it switched to Capital One and took credit as a % of sales from 50% to 60% over a 5yr time period. Any softening in the contribution from the credit business would put considerable pressure on the expense line with a double whammy if we continue to see weakening in the consumer credit metrics (more on that below).

Credit Considerations

This would characterize step 3 in our KSS short call (described above), and in summary, we’ve started to see a noticeable weakness in the credit quality on the margin. That’s import for KSS, who has 60%+ of its sales tied to its private label credit card and 1/3rd of its EBIT. The two most salient data points relevant to this discussion are…

1) Capital One, saw its net charge off rate accelerate in June, continuing the uptrend seen since September 2014. And let's not forget the denominator effect – the key there being that the charge-off calculation is basically bad debt expense divided by the total loan portfolio, so both numerator and denominator have an impact. Cap One (KSS credit partner) grew its loan portfolio 12% in 2Q at the same time charge-offs accelerated. So not only is default risk increasing, but the rate of change is being skewed positively by the rapid loan growth. The bottom line is the charge-off rate can accelerate much more rapidly than one might expect as the cycle rolls over. KSS shares in the bad debt risk with COF, so a change in the rate means less dollars to share in the partnership, which will minimize the SG&A offset that KSS has benefited from over the entirety of this cycle.

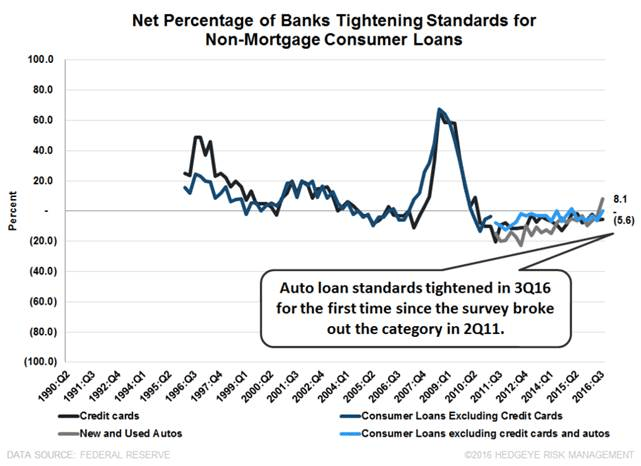

2) First consumer credit category turns to net tightening: After 2Q earnings season for consumer lenders brought about multiple warnings of building bad debt reserves and accelerating delinquencies, last week's Fed Senior Loan Officer Survey brought yet another warning sign. Bank lending standards on auto loans inflected to net tightening now in 3Q16. This follows C&I lending, which turned to net tightening in 4Q15, and CRE lending that turned in 1Q16. This is clearly a consequence of the cycle, and the credit cycle is like a Battleship: once it starts turning, it doesn’t want to stop. It’s likely we see the rest of consumer land turn to net tightening within a quarter or two.

Props to Hedgeye Financials