With Q2 earnings season underway, headlines centering on “earnings beats” as a bull catalyst are at a new cycle high. The “beat” catalyst from the bulge brackets is a bit ironic considering financials in the S&P 500 have beat bottom line estimates by double digits on average in the current cycle (taking out the post-recession beats, the 5-yr avg. beat is +5.9% from the Financials), outpacing every other sector.

In fact, every sector beats estimates, just about every quarter. This reporting season has started no differently. Earnings have come in at -5.7% Y/Y in aggregate so far with earnings exceeding expectations by nearly 4.2%:

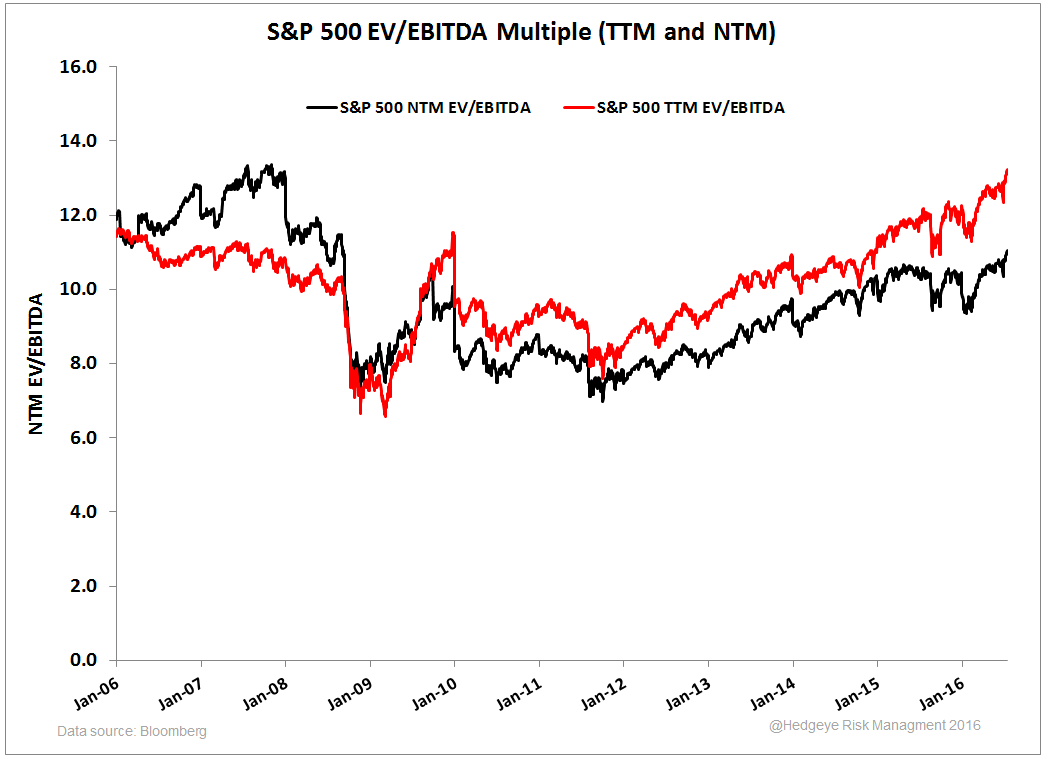

Looking at more highs, the current forward multiple is at a new cycle peak on earnings expectations that assume positive S&P earnings growth by Q3 2016, 9% in Q4 2016, and +16% and +14% by Q1 and Q2 2017 respectively. Starting in Q4 of this year, positive earnings growth expectations are baked in for every sector for three quarters through Q2 of 2017. So we’re looking at a market that has been taken to an all-time high on cycle-high buyback activity with a new cycle high forward multiple with optimistic earnings expectations in the denominator as seen in the chart immediately below.

So the earnings management cycle goes on...

Lofty earnings expectations --> Negative guidance communicated --> estimates taken lower --> company beats estimates

That’s seemingly a marginal positive for now. According to factset:

- S&P 500 earnings expectations for Q2 started the quarter at -2.1% Y/Y and were revised to -5.5% Y/Y by June 30th

- 81 companies issued negative guidance for Q2 vs. 32 that issued positive guidance

In Q2 of 2015 only two S&P 500 sectors comped down, energy and industrials, and energy’s -56.5% Y/Y comp was in reality a very large contributor to a -1.2% S&P earnings comp in Q2 of last year. And looking at energy in isolation, spot energy commodity prices were meaningfully lower Y/Y on average in Q2 of 2016. All in all, Q2 is not an easy comp across the board which has been largely baked into in expectations in real-time:

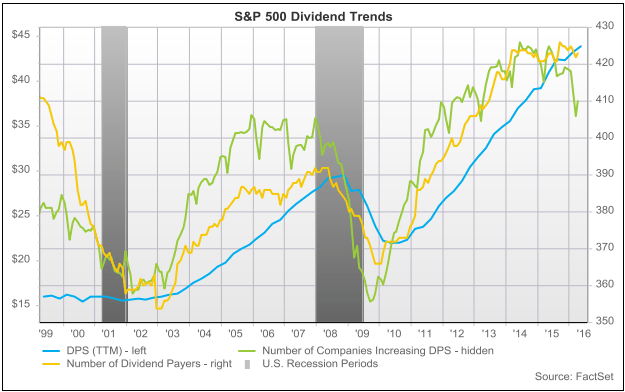

With lofty expectations, companies remain objectively laser focused on exceeding expectations, and the corporate gamery has increasingly picked up steam since margins and corporate profits peaked in 2H 2014 – buyback activity continues to make-up an increasing share of daily volume while return of capital via dividends is only showing early signs of deceleration:

As we've written, our expectation for Y/Y GDP for Q2 has been revised higher to +2.3%, implying the Q/Q SAAR number on which most of global macro is focused, could easily have a “4%” in front of it. The strength of last Friday’s retail sales report was a notable contributor to our revision with goods consumption contributing ~1/3 to PCE and ~1/4 to GDP – the trend in this series is meaningful. However, to re-iterate two important points with respect to the market’s potential reaction to a positive print:

- Can good news from an economic perspective now be good for the market just as deteriorating trending data was good for the creation of a policy tailwind?

- Is the risk of marginally hawkish policy with the data supported backdrop overpowered by good news?

Those are two questions worth asking, but a key takeaway with regard to our positive revisions for Q2 is the data supported overlay that employment and consumption is past peak with revolving credit showing mixed signs of slowing at a cycle low in delinquencies (credit growth has provided a consumption growth cushion since the consumer peaked in 1H 2015). Credit growth remains very robust, but taken as a whole, there is little room for an extension in the current consumer credit cycle and some metrics have already rolled over:

With the current “E” expectation empirically in question, we chose the title “high, high, high” instead of “peak, peak, peak” because we are constantly asked to weigh in on on the direction of the broader equity market in real-time (understandably as beta is the measuring stick for most) instead of focusing on what have been our better than bad tactical exposures within equities for most of 2016 (Long Utilities, short Financials).

So can market levels, multiples, and buyback activity reach new highs? Sure, but as we wrote in this morning's early look:

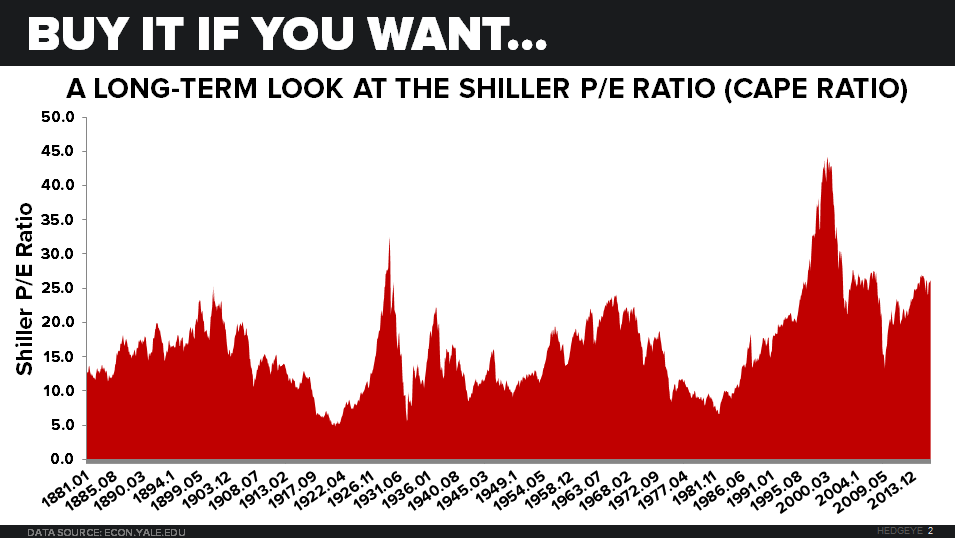

“At this price (i.e. the all-time closing high of 2166), even if you believe the “E” (Earnings) embedded in the SP500’s multiple, this is a Top 3 most expensive stock market in US history.”

And to add another behavioral overlay, fund flow data indicates the cyclical gravitation to beta is at a new cycle high with fund flows out of actively managed funds averaging -$2.8Bn weekly in 2016 according to ICI and headline stories this week of actively managed outflows Financial Times.

Please ping us back with comments or questions. We’re happy to look into anything mentioned above in more detail.

Ben Ryan

Analyst