- We are lowering our out year 2017 estimate to $0.28 per share, -30% below consensus on ongoing dramatic outflows from the company's 2 biggest products, the Hedged European Fund (HEDJ) and Hedged Japan (DXJ). While the sequential rate of change has improved slightly from -$5.4 billion in outflow last quarter (the worst quarter in the firm's history) to a running outflow of -$3.9 billion thus far in 2Q16, this time last year, WETF was still gathering assets at a substantial pace so the redemption story is still quite new. We don't think the firm has any chance of comping positively on a year-over-year basis until the first quarter of 2017.

- Most investors that are positive on the story believe that HEDJ and DXJ are just getting swept up in an unpopular International equity category which is not factually accurate in our view. The biggest factor for the substantial about face in positive trends in HEDJ and DXJ is the currency hedge which has nullified +15% annual returns in the Yen this year and a positive +3% return in the Euro. These funds were designed solely to capture QE trends, i.e. weakening currencies and positive equity returns but with risk aversion instead taking place, investors are covering Yen and Euro shorts (causing those currencies to rally) and are pulling out of local equities.

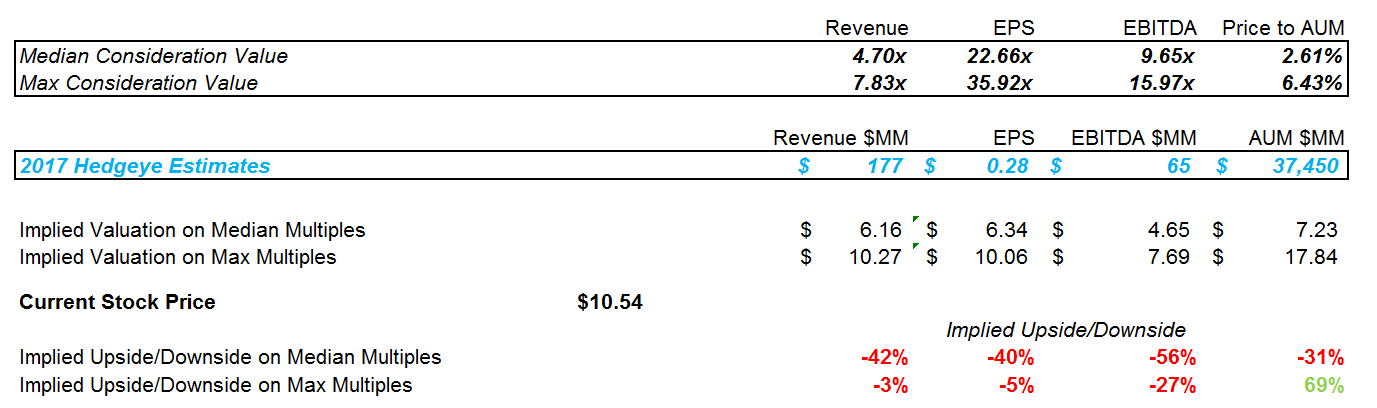

- The resting value for HEDJ and DXJ was roughly ~$1 billion each prior to respective QE programs and thus with the funds still at a combined $19 billion, there is still substantial downside in our view. Our $0.28 estimate assumes total AUM at $35 billion next year but we think a break even scenario is possible at $20 billion in AUM (we haven't forecated that scenario yet but we are watching for this). In our current earnings scenario we see fair value at $5-6 per share (using median valuation multiples on Revenue, Earnings, EBITDA, and AUM). If a breakeven scenario (on earnings) comes about, we forecast an equity value of $2 per share. We do not think shares currently are attractive as a take out candidate considering dour trends and concentration risk in the International Hedged Equity category.

Contrary to investor belief that the firm's biggest funds are "out of favor" because of the International Equity category, the bigger issue is the firm's hedging of foreign currencies within these funds which are now forcing investors out of these products as the hedges are now nullifying currency gains:

The resting value of both DXJ and HEDJ prior to QE programs in Japan and Europe was ~$1 billion each which leaves plenty of downside if risk aversion in both geographies continues:

Although flows have improved from -$5.4 billion last quarter, Q2 is running at -$3.9 billion down -150% from +$6.5 billion in 2Q15:

Fair value at our current projection for 2017 on Revenue, Earnings, EBITDA, and AUM points to downside of up to -50% from here. At a breakeven scenario on earnings at $20 billion in AUM, we see fair value at $2 per share. We do not think shares are attractive as a take out candidate with distressed trends:

WisdomTree (WETF) - It's Different This Time

WisdomTree (WETF) - The Land of the Sinking Sun

WisdomTree (WETF) - The Kuroda Kicker

WisdomTree (WETF) - More Questions Than Answers - We Remain Short

Please let us know of questions,

Jonathan Casteleyn, CFA, CMT