INTRODUCTION

The prevailing bull-case story has been about NFLX redefining video consumption, if not replacing linear TV altogether. That story has evolved from NFLX emerging as a rising domestic content distributor to potentially becoming a global distributor, producer, and network all in one. That story had being gaining steam over the past couple years, however the YTD volatility in the stock suggests sentiment has been wavering, which should provide more opportunities to get involved in the stock. Further, NFLX’s simultaneous launch into 130 countries in 1Q essentially accelerates the test case into 2016 for how the longer-term global expansion story will play out.

Below is the first of what will be a series of notes that we will be publishing on NFLX. The longer term story really hinges on NFLX’s ability to grow into its content obligations, which we suspect is a loosely understood topic. While we are bearish on NFLX in this respect, there is no immediate way to play that part of the story yet. That said, we’re staying on the sidelines until we can get some edge on its sub growth metrics, which may be the only thing that matters for the stock at this point. In the interim, we will continue publishing additional analysis, which we hope will assist you in your process.

KEY POINTS

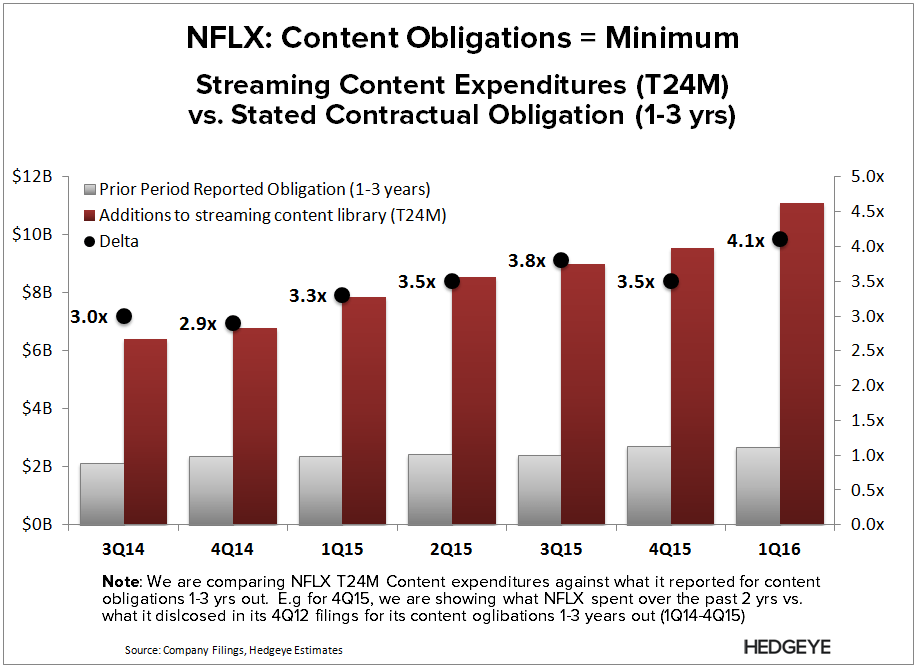

- CONTENT OBLIGATIONS ≈ BARE MINIMUM: What NFLX reports as its streaming content obligations are the minimum legally-binding amounts that it can currently identify. Many of these contracts have unspecified commitments based on future title releases, which is also why NFLX’s reported obligations are front-end loaded. Historically, NFLX spends multiples more than what it had previously identified as its contractual obligations, so the ~$11B due over the next 3 years could wind up being considerably higher if history repeats itself.

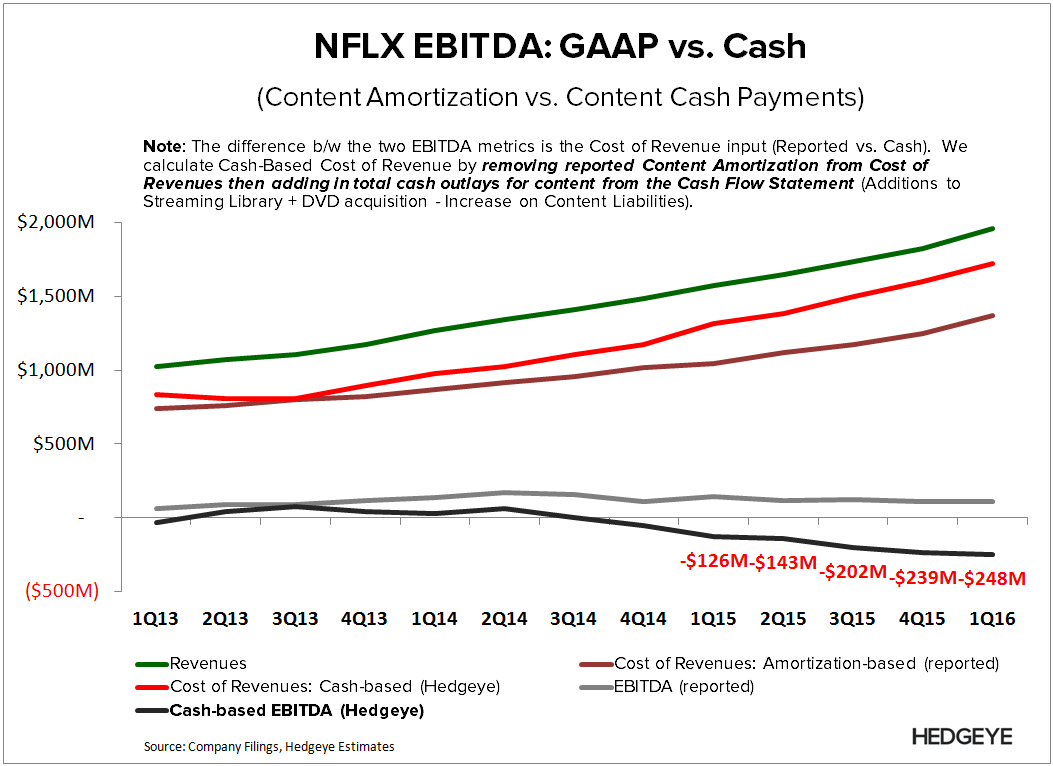

- CONTENT IS MORE EXPENSE THAN ASSET: NFLX is primarily paying for access not ownership; its content assets are largely comprised of contracts that allow NFLX to stream its suppliers' content. NFLX historically amortizes the majority of its content assets within a year, which suggests that its content outlays are more expense than they are asset. That said, the better way to contextualize NFLX’s model is from a cash perspective (vs. GAAP) since the former better captures the actual operating costs necessary to keep the business running.

- WHAT DOES THIS MEAN? NFLX’s stated content obligations are really more of a look at the minimum ongoing cost of running its business rather than a distant set of milestone that it will have to meet someday. This naturally calls into question NFLX’s ongoing ability to cover its content costs or whether NFLX will be able to sustain the breadth of its content offering down the road. That will largely depend on its ability to realize its subscriber TAM, and what it has to pay in subscriber acquisition costs to do so (note to follow).

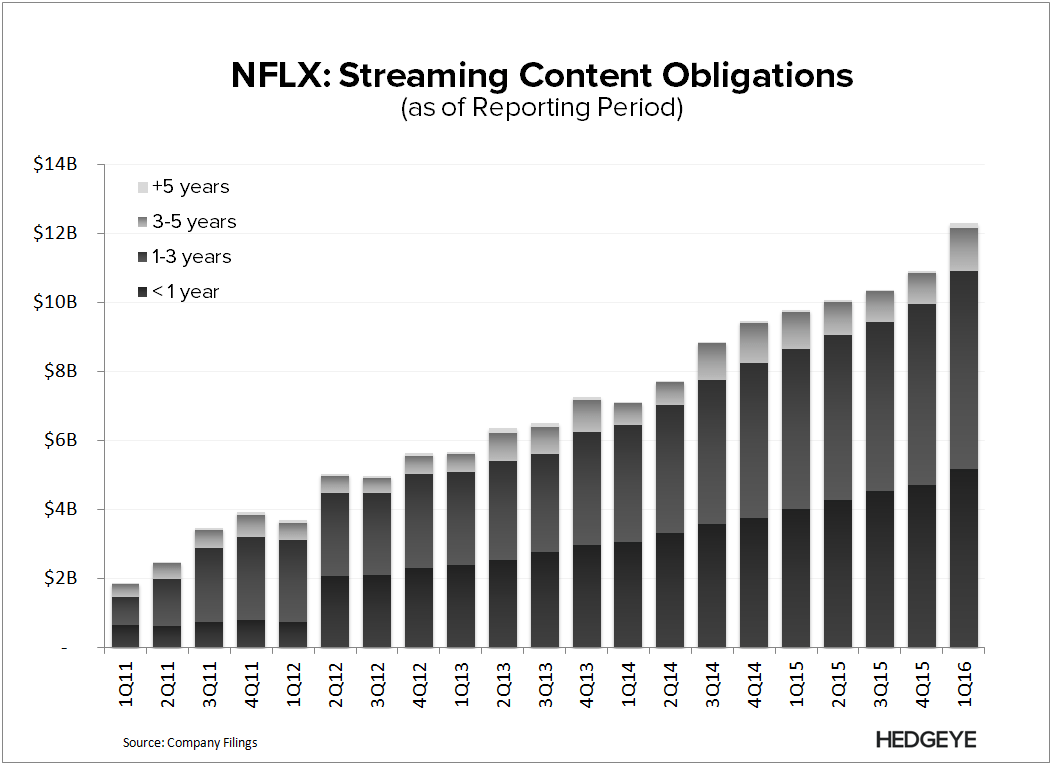

CONTENT OBLIGATIONS ≈ BARE MINIMUM

What NFLX reports as its streaming content obligations are the minimum legally binding amounts that it can currently identify. Many of these contracts have unspecified commitments for future titles in which the number of titles and associated fees are unknown. This is why nearly 90% of its reported streaming content obligations are historically concentrated in the upcoming 3-yr period (almost half in current year).

NFLX currently estimates that its streaming content obligations over the next 3 years could wind up being $3B-$5B higher than the ~$11B it is has most recently estimated for that period. But historically speaking, NFLX generally usually spends multiples more than what it previously estimated for its streaming content obligations. Granted some of that may be related to original content and opportunistic spending, but the delta is considerable regardless.

We’re not suggesting that NFLX is holding anything back. We're just pointing out that mgmt doesn't fully know much it will be required to spend under these contracts, and that its reported streaming obligations aren’t really a reflection of what NFLX will actually spend. That said, we shouldn’t be putting too much stock into those numbers since they are an artificially low hurdle.

CONTENT IS MORE EXPENSE THAN ASSET

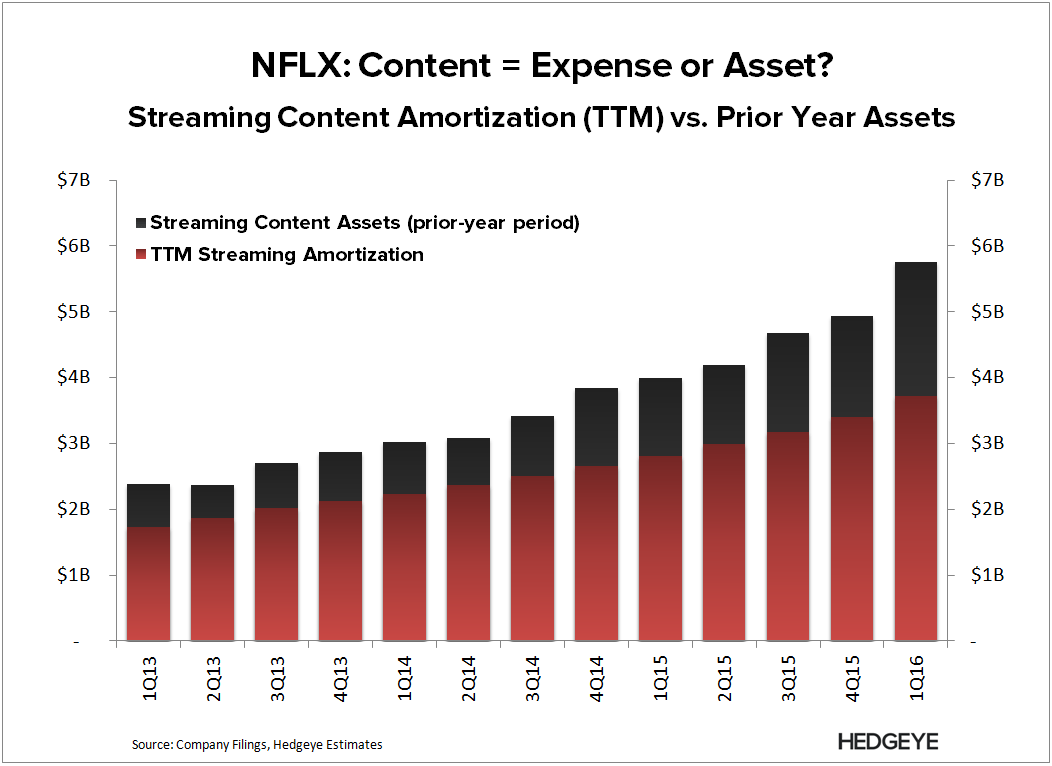

NFLX is primarily paying for access not ownership. NFLX’s content assets are largely comprised of contracts that allow NFLX to stream its suppliers' content. NFLX's amortization history suggests most of these contract are either short-term or the underlying content has a relatively short useful life. NFLX suggests that its amortization period ranges from 6 months to 5 years, but it historically amortizes its entire library within two years, with the bulk of that amortization occurring in the initial year.

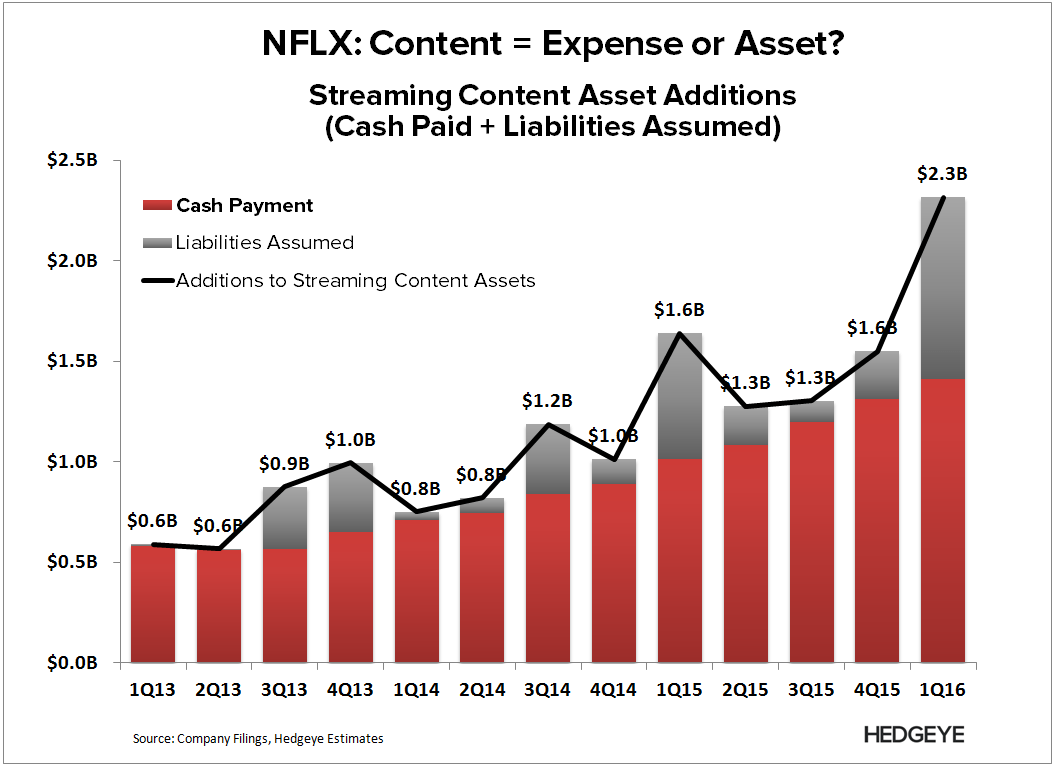

NFLX’s historically quick amortization schedule combined with its recurrent cash outlays for content suggests that its content is more of an expense than an asset. We’re not suggesting that NFLX’s GAAP amortization methodology is inappropriate, but believe evaluating the model on cash basis is the better way to contextualize its operating performance. Put another way, NFLX’s current cash outlays for content better captures the actual operational costs necessary to run its business.

In the charts below, we’re calculating Cash EBITDA and Contribution Margin by swapping out reported Content Amortization from reported Cost of Revenues, then swapping in NFLX’s cash outlays for content acquisition from the Cash Flow Statement. We understand some of you may take issue with calculating EBITDA in this fashion, but our calculation aligns better with NFLX’s reported Operating Cash Flow than its reported EBITDA metrics, which makes sense since almost all of NFLX’s content outlays are recorded in Operating Activities (vs. Investing).

WHAT DOES THIS MEAN?

In short, NFLX’s contractual obligations are essentially understated recurring expenses, which means that those obligations are really more of a look into the minimum ongoing cost of running its business rather than a distant set of milestones that it will have to meet someday.

This naturally calls into question NFLX’s ongoing ability to cover its content costs or whether NFLX will be able to sustain the breadth of its content offering down the road. There only so times that NFLX will be able to take price or borrow long-term debt to finance what are essentially recurring short-term liabilities. That said, NFLX’s ability to sustain/build its content portfolio will likely hinge on its ability to realize its subscriber TAM, and what it has to pay in subscriber acquisition costs to do so.

We will be publishing another note shortly to discuss the dynamics of NFLX’s subscriber TAM. In the interim, let us know if you have any questions or would like to discuss further.