Overview

We have not previously added short UAL Equity to our firm’s Best Ideas list, despite numerous issues with UAL’s “adjusted” financial reporting and the broader airline renaissance thesis. We have had the CDS on the list, which were very tight in mid-2014 and we believed offered an attractive asymmetric return potential. However, with employment at or very near a peak for this cycle, we expect demand growth to slow and potentially turn negative in 2016. At the same time, lower fuel prices have allowed the industry to rapidly grow capacity. Weaker demand and rapid capacity growth are likely to prove a toxic combination...particularly for UAL.

This isn’t a call on UAL’s report tomorrow, which should be roughly in line with the Investor Update. UAL’s outlook may well be just as rosy as DAL’s, even though we have observed some modest pressure on UAL’s fares in recent readings. The equity market could also bounce, taking shares of UAL higher. However, this is a longer-term view, informed by capacity growth amid changing fleet dynamics, an expected softening of demand, and our firm’s Macro process. Ping us for our prior Black Books and EQM/data sets for additional background.

Highlights

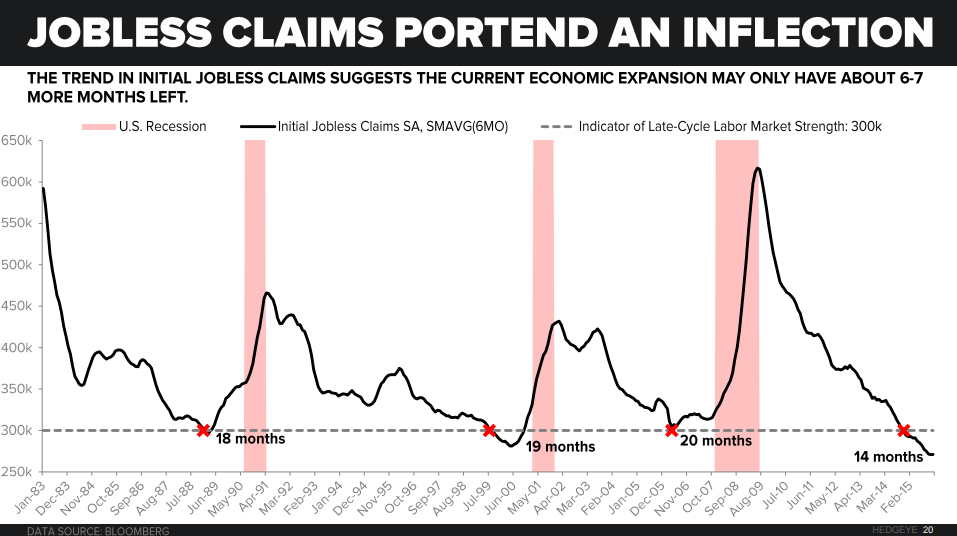

Fade Ideal Environment: Following a 70%+ drop in the price of oil and a halving of the unemployment rate, it would be hard for the airline environment to be better. Our firm’s Macro team makes a strong argument for a recession, or at least a recessionary environment, in 2016. The data are compelling. For example, credit losses are coming from resource-related industries from coal mining to oil & gas to metals. Credit losses typically bring broadly tighter credit. For airlines, as we show below, the economy need not experience a downturn on the scale of the Financial Crisis for the shares to sell off sharply. Airlines typically perform horribly on both an absolute and relative basis in periods of economic slowing. Even the 2H 2012 slowdown took a third off shares of UAL from a much lower level. In a recession, even “high-quality industrials” would continue to sell-off sharply.

h/t Hedgeye Macro

Airlines Still Beloved: Amazingly, 100% of analysts rate Delta Airlines a Buy. Perhaps more amazingly, 88% rate UAL a Buy. Yet, if the recession/significant slowdown call is correct, airline shares face a disproportionately large downside. Higher cost airlines often fail in recessions; there is little historical precedent to expect airline shares to perform defensively through a downturn.

UAL As Tide Goes Out: We have detailed what we view as series of accounting gimmicks that have served to boost UAL’s adjusted numbers. We won’t rehash all of them, but here are a few:

- Writing-up frequent flier deferred revenue on emergence and in CAL purchase accounting allocations, only to drain it through later changes to FFP assumptions at ~100% margin (we estimate this at well over $1 billion)

- Categorizing cash paid to employees as a one-time expense; GAAP allows it, but doesn’t require exclusion from adjusted results

- Special charges for uniforms, aircraft painting which seem fairly operating to us

In recent years, UAL has only generated free cash flow on the firm’s own metric with employment trends peaking and jet fuel prices cratering. We see the mismatch between cash and adjusted profits as noteworthy.

It is not as though capacity additions have been driving the cash drain. Domestic capacity has generally contracted and UAL has steadily dribbled away market share.

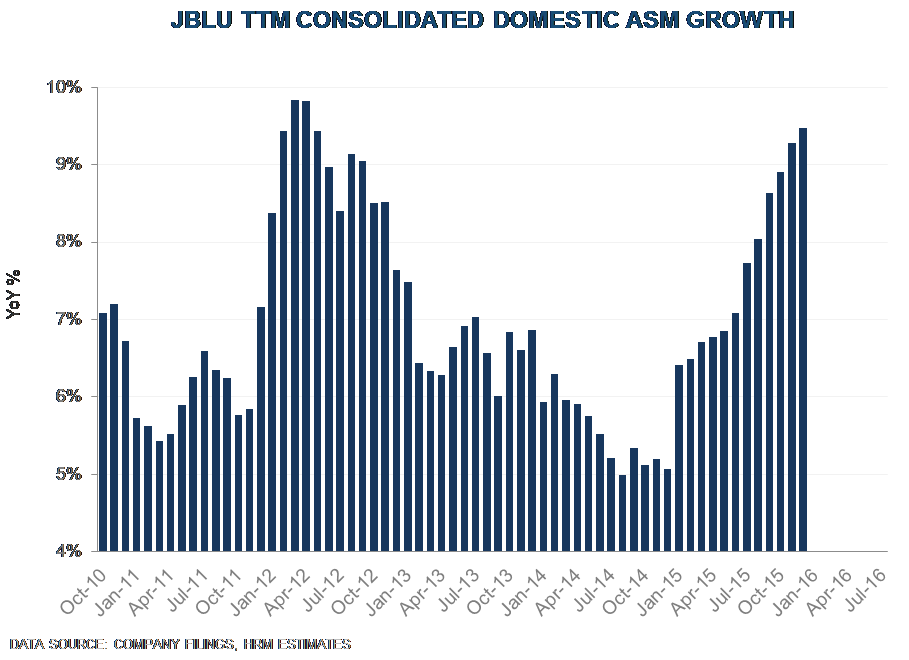

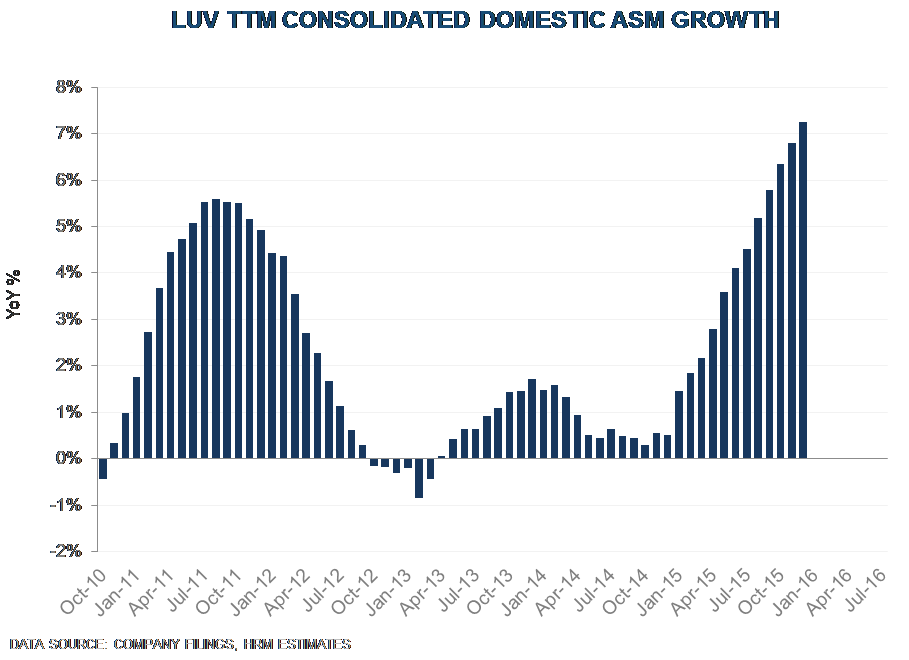

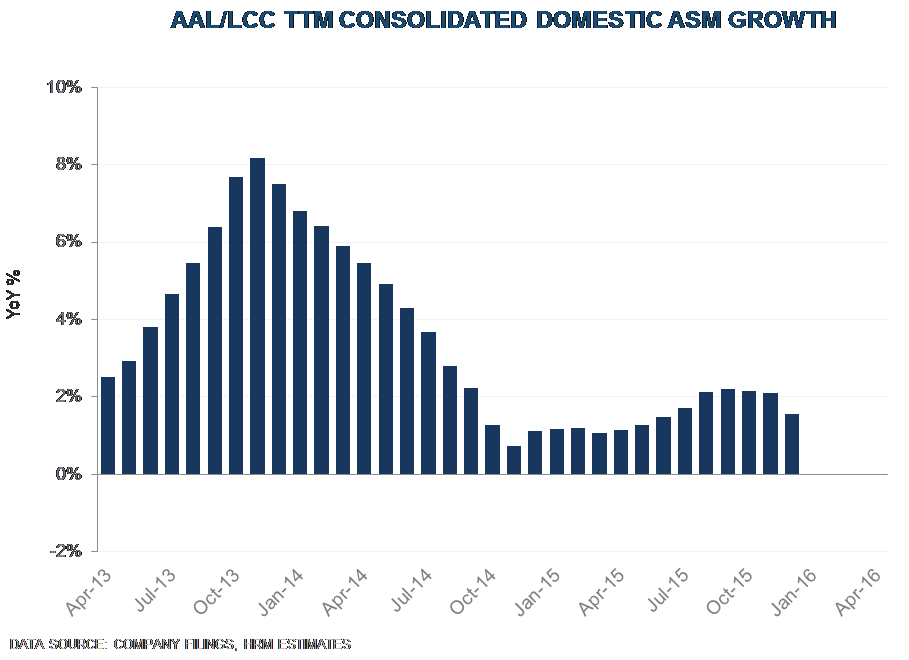

Domestic Capacity No Longer Disciplined: Domestic airline capacity growth is outpacing its typical relationship to economic growth amid lower fuel costs. This is shown below as a residual from the regression of Industrial Production to ASM growth.

Which tends to be explained by fuel prices….

So far, demand has kept pace as lower airfares and higher employment generated adequate traffic. In a recessionary environment, however, we expect capacity trends to prove troublesome. Capex is up, and capacity is coming on rapidly into a deteriorating macroeconomic environment. We have generally explained accelerated capacity growth as resulting from flattening of the incremental capacity cost curve in a lower fuel price environment (e.g. economics of older planes work better at lower fuel prices).

AAL is still roughly playing the game, but this is partly company specific.

And capital spending has ramped higher.

UAL Cost Challenges: For a company which has twice promised billions in cost reductions (Project Quality & Merger Synergies), UAL’s cost efforts may have limited how quickly costs have grown, although it is hard to tell if that is the case. At a November conference appearance, UAL claimed to have cut “$800 million” in 2015 non-fuel operating expenses in November, which is odd since non-fuel expenses are generally higher vs. 2014.

Liquidity & Net Debt: In the best airline operating environment in a generation, UAL did not make much progress on net debt or liquidity. The relatively small buyback activity (net of converted debt, that is) may be viewed as an error in a recessionary environment.

Senior Management Uncertainty: We very much hope that UAL’s CEO Oscar Munoz makes a speedy recovery. As unfortunate as it is, senior management has been lacking at the firm since Jeff Smisek was pushed out following the Port Authority scandal. That may prove an additional challenge.

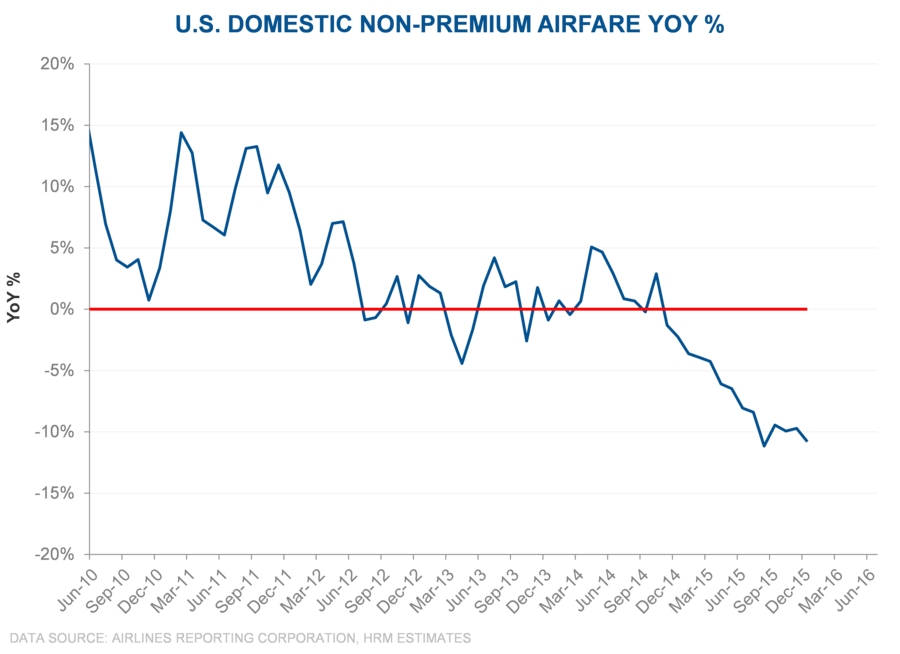

2015 Fuel Profits: UAL has benefited enormously from the decline in fuel prices. We expect airfares to compete away lower fuel on a lag. Since airfares are readily tracked daily, investors may need to move well ahead of actual changes.

Upshot: We see UAL as a high cost airline with dubious financial reporting, a combination that seems a straightforward short in a recessionary environment. Airlines are historically among the most cyclical groups, but UAL is still very much “up” and investor sentiment remains very positive despite signs of an inflection in economic activity. We expect the shares to trade lower before airfares fully reflect the changed environment. While this does not represent a view on UAL’s soon-to-be reported quarter, the tide appears to be moving out amid a loss of capacity discipline.