Upshot: We continue to think that NSC offers relative upside, and would look to initiate a position in the mid-70s to low 80s as presented in our Best Ideas Black Book call above. The rejection of CP’s low bid should come as little surprise, but the reply incorporated a list of hurdles that would need to be overcome in a new and higher bid. NSC’s rapidly improving performance metrics create the potential for a favorable cost surprise along the lines of the 3Q 2015 beat.

NSC/Rail Black Book (9/16/2015):

- REPLAY: CLICK HERE

- VIDEO: CLICK HERE

- SLIDES: CLICK HERE

NSC Is Worth Far More Than Discarded Bid: Holders of NSC have been in a tough spot, we think, with risks to an improbable deal in the way of a longer-term performance opportunity. The CP offer premium was always too low, especially given the regulatory risks and process duration. Pursuing a merger would attract regulatory attention, the last thing an industry making use of a strong pricing leverage needs. The offer was too low, awkwardly presented, and incompletely planned – NSC is just making that clear with its thoughtful and well-presented rejection. For a modestly patient investor we think there is a good deal more upside for NSC. For deal optimists (not us) the potential for a higher bid remains.

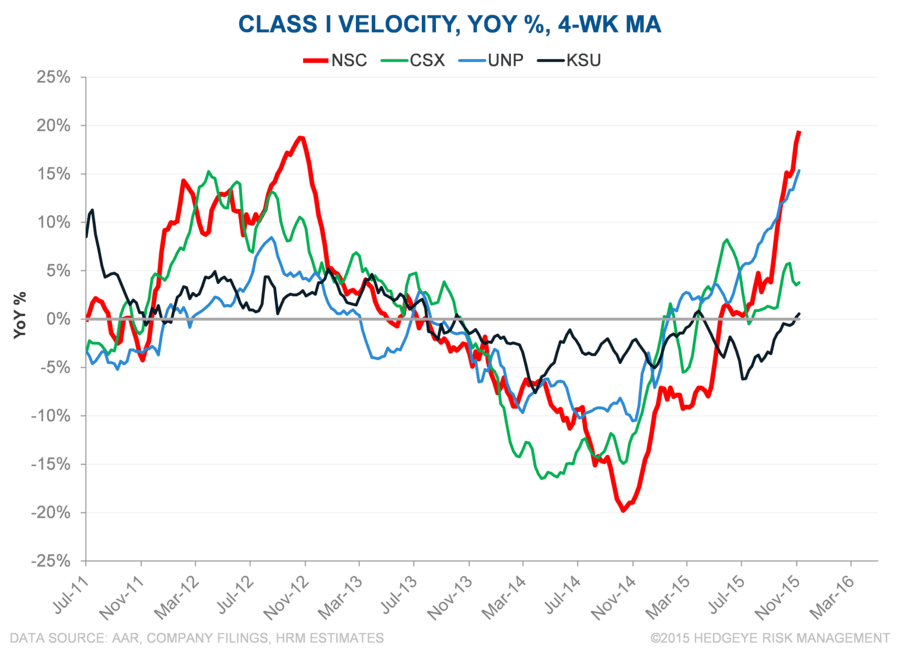

Management Is Confident For A Reason: The longer-term outlook put forth by NSC’s newish management team was favorable and ahead the multiyear consensus estimates by our calculations. NSC’s cost and capital improvements are in process, and performance metrics are improving markedly. That matters. Higher speeds and lower dwell should push cost out of the network, a key factor in NSC’s beat last quarter. As long at NSC’s results continue to track with our long thesis (linked above), we expect to stick with the shares until at least the triple digits, all else equal. In a weak equity market, we would expect shares of NSC to be defensive, sector relative outperformer.

For Deal Optimists: NSC provided a transparent, thoughtful, and detailed response to the CP bid. Management took the low bid seriously, respecting shareholder interests. NSC’s Board also gave CP a clear roadmap of the objections that would need to be overcome to strike an agreement. CP can now work on constructing a higher bid (perhaps >$140, stock heavy) overcoming NSC’s straightforward concerns….if CP’s management is serious about completing the transaction.

Sentiment & Weather: 4Q weather in the Northeastern U.S. has been unusually warm, hurting coal volumes for NSC and other rails. Weather varies, and is not of the same relevance as MATS regulations and sustained lower natural gas prices. NSC’s coal franchise has been in secular decline for pretty much the entire “rail renaissance”, with pricing helping to offset the impact on revenue. NSC is not very popular on any side of the Street, as we see it. The vaguely hostile Q&A on this morning’s deal rejection call made that reasonably clear.

Upshot: We continue to think that NSC offers relative upside, and would look to initiate a position in the mid-70s to low 80s as presented in our Best Ideas Black Book call above. The rejection of CP’s low bid should come as little surprise, but the reply incorporated a list of hurdles that would need to be overcome in a new and higher bid. NSC’s rapidly improving performance metrics create the potential for a cost surprise while the Street fixates on volume pressures.