This note was originally published January 07, 2013 at 11:36 in Restaurants

The primary takeaway from this post is the most important macro indicators are continuing to confirm our bearish stance on casual dining.

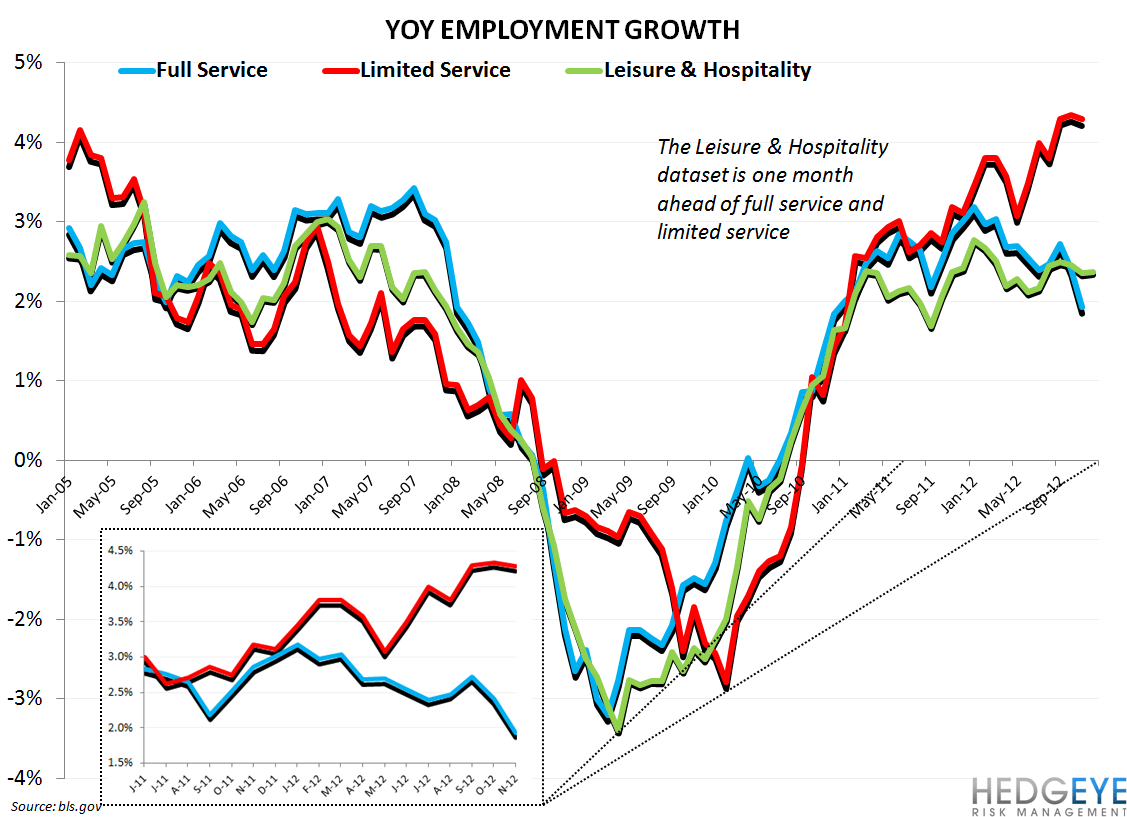

Employment trends within the industry suggest a possible sequential deceleration in same-restaurant casual dining sales. The deceleration of employment growth within casual dining versus quick service and the broader leisure and hospitality industry is worth noting.

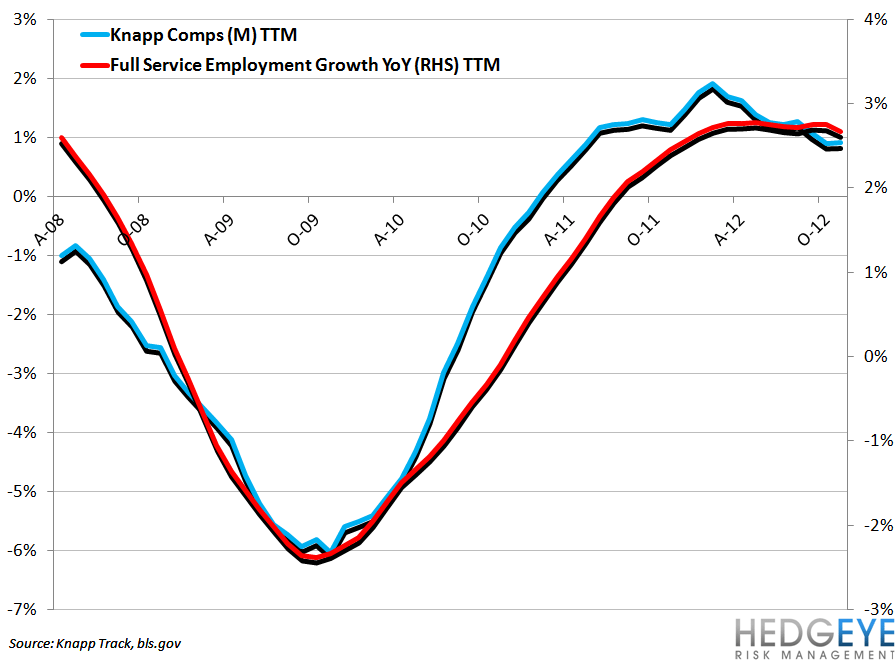

Knapp Track Casual Dining sales data track BLS employment growth data for the full-service and leisure and hospitality industries. Within casual dining, we are bearish on DRI, BWLD, and TXRH

Employment by Age

Employment growth by age cohort implies that quick service restaurants are benefitting from strong employment growth among core consumers while casual dining’s struggles are being caused, at least in part, by decelerating employment growth of one of the sector’s core demographics.

The chart below illustrates a strong end to the year for employment growth among the younger age cohorts. Job growth in the 20-24 years of age cohort remained in the 3% range while growth in the number of employed 23-34 year olds accelerated to 1.2% in December from 0.7% the month prior. This is positive data point for QSR.

Employment growth among 55-64 year olds remains robust, accelerating to 5.6% in December, but softer trends in the 45-54 years of age cohort is a concern for casual dining.

Industry Hiring

If we assume that hiring within the restaurant industry serves as a decent proxy for operator confidence, it seems that QSR operators have a very different outlook than casual dining operators.

The continuing sideways trajectory of Leisure & Hospitality employment growth suggests that employment growth in limited service restaurants could be overstretching at this point. However, with consumers trading down and quick service chains investing in enhancing the consumer’s experience at their restaurants, it is difficult to come to a firm conclusion.

Sequential Moves

- Leisure and Hospitality: Employment growth at 2.38% in December (+1.7 bps seq acceleration)

- Limited Service: Employment growth at 4.29% in November (-5.3 bps seq deceleration)

- Full Service: Employment growth at 1.93% in November (-47.8 bps seq deceleration)

Howard Penney

Managing Director

HPenney@hedgeye.com

646.455.0992

Rory Green

Senior Analyst

RGreen@hedgeye.com

646.455.0992